“Money won’t create success. The freedom to make it will.”

-NELSON MANDELA

The Point of (Almost) No Return. Long, long ago, back when the earth was cooling and I began writing this newsletter, John Mauldin was my role model. His Thoughts From the Frontline weekly missive had already gone semi-viral and, shortly thereafter, the “semi” was no longer applicable as his recipient list surged into the millions.

Around that time, circa 2006, I also began attending his now acclaimed Strategic Investment Conference. As I’ve admitted several times in the past, it was at those events that I became convinced the then-prevailing housing boom was soon to go bust, a conclusion that saved Evergreen clients a considerable sum in subsequent years. Since those early days, I’ve gone from being a Mauldin acolyte to the honor of being a FOJ—Friend of John. In fact, at my partner Louis Gave’s 40th birthday party up at Whistler two years ago, John even graciously tolerated my American bulldog sampling some of the food he had left on his plate by Louis’ outdoor fire pit.

It’s been quite awhile since we’ve run one of John’s newsletters as a Guest EVA. But his recent piece, “The Age of No Returns”, focuses on several issues that Evergreen believes are of utmost importance. We plan to expand on these and several others in next week’s full-length EVA but, in the meantime, John provides a concise overview of some of the realities bullish investors might be overlooking currently.

First up is the growing discontent in Italy and the distinct possibility its populace effectively votes for an “Italxit” in a referendum this October (the vote is not technically an in or out initiative but it is being viewed that way in Europe). Very few Americans seem to be aware of this potentially explosive event. Yet, it has the potential to be far more destabilizing than Brexit.

Next is the extermination of interest rates that continues to evolve (devolve?) globally. The most extreme manifestation of this assault against savers is, of course, NIRP—the dreaded but increasingly common Negative Interest Rate Policy. Should you believe this is only an overseas curiosity, John contends the Fed is already setting the stage to bring it to our shores. Related to this, is the disturbing—at least for income-needy investors—implication that this interest-free (at best) environment may continue for many years to come.

Then there is his contention that the Fed’s radical monetary policies are in reality inhibiting, not enhancing, the US economy. Granted, as he points out, this has been the fourth longest expansion of the past 60 years but is also by far the weakest. Unfortunately, there doesn’t appear to be any durable acceleration on the horizon and we are getting very late in this business cycle.

To close, John highlights a graphic from a firm that has consistently produced one of the most accurate long-term return projections for various slices of the investment universe, GMO. You’ll see their updated chart on what they anticipate for US stocks, international equities, as well as domestic and overseas bonds, on an inflation-adjusted basis.

Fair warning: you may want to read this with a potent adult beverage in hand, despite the US market’s recent ebullience (which Evergreen believes can continue for awhile longer). Further, we remain convinced future market conditions will be extremely well-suited to contrarians willing to buy into sector-specific collapse such as we saw last year with energy and in 2013 in the gold space. In other words, don’t despair but be prepared to think and act unconventionally.

P.S. As a last minute bonus, we’ve added a relevant commentary, in this case from another friend, Simon Mikhailovich from the Tocqueville Bullion Reserve (by the way, this is an excellent vehicle to consider if you’d like to hold some gold offshore, in a completely transparent and legal manner).

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

By John Mauldin

“A bank is a place where they lend you an umbrella in fair weather and ask for it back when it begins to rain.”

– Robert Frost

The enemy is coming. Having absorbed Japan to the west and Europe to the east, negative interest rates now threaten North America from both directions. The vast oceans that protect us from invasions won’t help this time.

Someday I want to get someone to count the number of times I’ve mentioned central bank chiefs by name in this newsletter since I first began writing in 2000, and we should graph the mentions by month. I suspect we’ll find that the number spiked higher in 2007 and has remained at a high plateau ever since – if it has not climbed even higher.

That’s our problem in a nutshell. We shouldn’t have to talk about central banks and their leaders every time we discuss the economy. Monetary policy is but one factor in the grand economic equation and should certainly not be the most important one. Yet the Fed and its fellow central banks have been hogging center stage for nearly a decade now.

That might be okay if their policies made sense, but abundant evidence says they do not. Overreliance on low interest rates to stimulate growth led our central bankers to zero interest rates. Failure of zero rates led them to negative rates. Now negative rates aren’t working, so their ploy is to go even more negative and throw massive quantitative easing and deficit financing at the balky global economy. Paul Krugman is beating the drum for more radical Keynesianism as loudly as anyone. He has a legion of followers. Unfortunately, they are in control in the halls of monetary policy power.

Our central banks are one-trick ponies. They do their tricks well, but no one is applauding, except the adherents of central bank philosophy. Those of us who live in the real economy are growing increasingly restive.

Today we’ll look at a few of the big problems that the Fed and its ilk are creating. As you’ll see, I think we are close to the point in the US where a significant course change might help, because our fate is increasingly locked in. I believe Europe and Japan have passed the point of no return. That means we should shift our thinking toward defensive measures.

The Big Conundrum

The immediate Brexit shock is passing, for now, but Europe is still a minefield. The Italian bank situation threatens to blow up into another angry stand-off like Greece, with much larger amounts at stake. The European Central Bank’s (ECB) grand plans have not brought Southern Europe back from depression-like conditions. I cannot state this strongly enough: Italy is dramatically important, and it is on the brink of a radical break with European Union (EU) policy that will cascade into countries all over Europe and see them going their own way with regard to their banking systems. Italian politicians cannot allow Italian citizens to lose hundreds of billions, if not trillions, of euros to bank “bail-ins.” Such losses would be an utter disaster for Italy, resulting in a deflationary depression not unlike Greece’s. Of course, for the Italians to bail out their own banks, they will have to run their debt-to-GDP ratio up to levels that look like Greece’s. Will the ECB step in and buy Italy’s debt and keep their rates within reason? Before or after Italy violates ECB and EU policy?

The Brexit vote isn’t directly connected to the banking issue, but it is still relevant. It has emboldened populist movements in other countries and forced politicians to respond. The usual Brussels delay tactics are losing their effectiveness. The associated uncertainty is showing itself in ever-lower interest rates throughout the Continent.

That’s the situation to America’s east. On our western flank, Japan had national elections last weekend. Voters there do not share the anti-establishment fever that grips the rest of the developed world. They gave Prime Minister Shinzo Abe and his allies a solid parliamentary majority. Japanese are either happy with the Abenomics program or see no better alternative.

His expanded majority may give Abe the backing he needs to revise Japan’s constitution and its official pacifism policy. Doing so would be less a sign of nationalism than a new economic stimulus tool. Defense spending that more than doubles – as it is expected to do – will give a major boost to Japan’s shipyards, vehicle manufacturing, and electronics industries.

The Bank of Japan’s negative-rate policy and gargantuan bond-buying operation will now continue full force and may even grow. Whether the program works or not is almost beside the point. It shows the government is “doing something” and suppresses the immediate symptoms of economic malaise.

The Bank of Japan is the Japanese bond market. They are buying everything that comes available, and this year they will need to cough up an extra ¥40 trillion ($400 billion) just to make their purchase target, let alone increase their quantitative easing in the desperate attempt to drive up inflation. What is happening is that foreign speculators are becoming some of the largest holders of Japanese bonds, and many Japanese pension funds and other institutions are required to hold those bonds, so they aren’t selling. The irony is that the government is producing only about half the quantity of bonds the Bank of Japan (BOJ) wants to buy. Sometime this year the BOJ is going to have to do something differently. The question is, what?

Okay, for you conspiracy theorists, please note that “Helicopter Ben” Bernanke was just in Japan and had private meetings with both Prime Minister Abe and Kuroda, who heads the Bank of Japan.

Given the limited availability of bonds for the BOJ to buy, and that they’ve already bought a significant chunk of equities and other nontraditional holdings for a central bank, what are their other options?

Perhaps Japan could authorize the BOJ to issue very-low-interest perpetual bonds to take on a significant portion of the Japanese debt. That option has certainly been a topic of discussion. It’s not exactly clear how you get people to give up their current debt when they don’t want to, or maybe the BOJ just forces them to swap out their old bonds for the new perpetual bonds, which would be on the balance sheet of the Bank of Japan and not counted as government debt. That’s one way to get rid of your debt problem.

But that doesn’t give Abe and Kuroda the inflation they desperately want. Putting on my tinfoil hat (Zero Hedge should love this), the one country that could lead the way in actually experimenting with a big old helicopter drop of money into individual pockets is Japan. And Ben was just there… This bears watching. Okay, I am now removing my tinfoil hat.

Yellen Changes the NIRP Tune

I have been saying on the record for some time that I think it is really possible that the Fed will push rates below zero when the next recession arrives. I explained at length a few months ago in “The Fed Prepares to Dive.”

In that regard, something important happened recently that few people noticed. I’ll review a little history in order to explain. In Congressional testimony last February, a member of Congress asked Janet Yellen if the Fed had legal authority to use negative interest rates. Her answer was this:

In the spirit of prudent planning we always try to look at what options we would have available to us, either if we needed to tighten policy more rapidly than we expect or the opposite. So we would take a look at [negative rates]. The legal issues I’m not prepared to tell you have been thoroughly examined at this point. I am not aware of anything that would prevent [the Fed from taking interest rates into negative territory]. But I am saying we have not fully investigated the legal issues.

So as of then, Yellen had no firm answer either way.

A few weeks later she sent a letter to Rep. Brad Sherman (D-CA), who had asked what the Fed intended to do in the next recession and if it had authority to implement negative rates. She did not directly answer the legality question, but Bloomberg reported at the time (May 12) that Rep. Sherman took the response to mean that the Fed thought it had the authority. Yellen noted in the letter that negative rates elsewhere seemed to be having an effect. (I agree that they are having an effect; it’s just that I don’t think the effect is a good one.)

Fast-forward a few more weeks to Yellen’s June 21 congressional appearance. She took us further down the rabbit hole, stating flatly that the Fed does have legal authority to use negative rates, but denying any intent to do so. “We don’t think we are going to have to provide accommodation, and if we do, [negative rates] is not something on our list,” Yellen said.

That denial came two days before the Brexit vote, which we now know from FOMC (Federal Open Market Committee) minutes had been discussed at a meeting the week earlier. But I’m more concerned about the legal authority question. If we are to believe Yellen’s sworn testimony to Congress, we know three things:

When I wrote about this back in February, I said the Fed’s legal staff should all be disbarred if they hadn’t investigated these legal issues. Clearly they had. Bottom line: by putting the legal authority question to rest, the Fed is laying the groundwork for taking rates below zero. And I’m sure Yellen was telling the truth when she said last month that they had no such plan.

Plans can change. The Fed always tells us they are data-dependent. If the data says we are in recession, I think it is very possible the Fed will turn to negative rates to boost the economy. Except, in my opinion, it won’t work.

When Average Is Zero

Now, I am not suggesting the Fed will push rates negative this month or even this year – but they will do it eventually. I’ll be surprised if it doesn’t happen by the end of 2018.

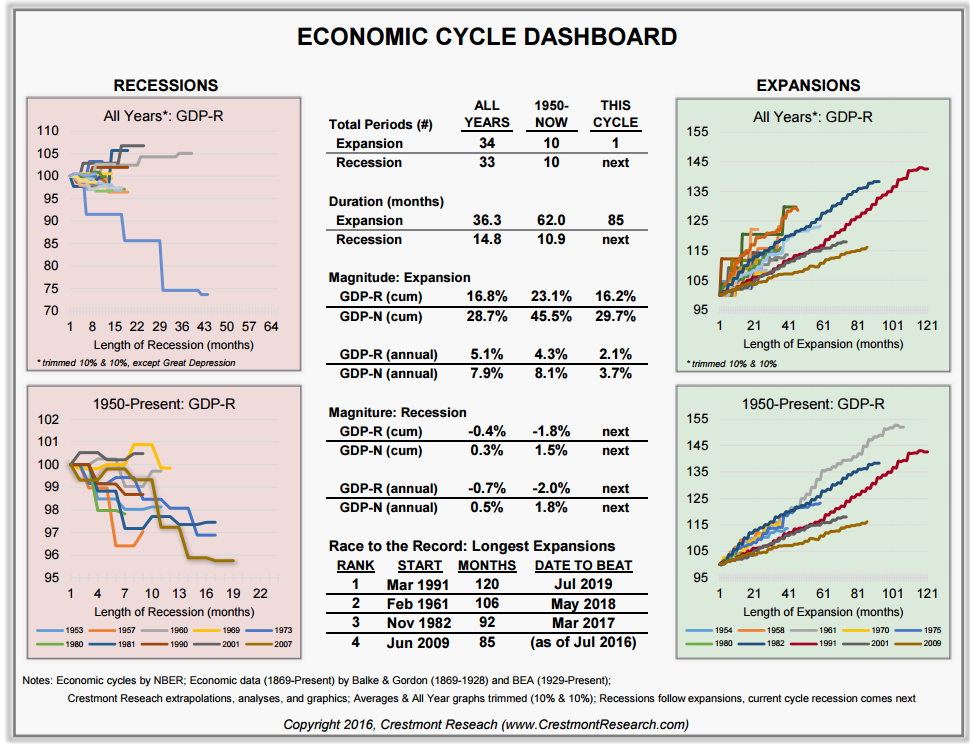

A prime reason the next recession will be severe is that we never truly recovered from the last one. My friend Ed Easterling of Crestmont Research just updated his Economic Cycle Dashboard and sent me a personal email with some of his thoughts. His chart is below.

The current expansion is the fourth-longest one since 1954 but also the weakest. Since 1950, average annual GDP growth in recovery periods has been 4.3%. This time around, average GDP growth has been only 2.1% for the seven years following the Great Recession. That means the economy has grown a mere 16% during this so-called “recovery” (a term Ed says he plans to avoid in the future).

If this were an average recovery, total GDP growth would have been 34% by now instead of 16%. So it’s no wonder that wage growth, job creation, household income, and all kinds of other stats look so meager. For reasons I have outlined elsewhere and will write more about in the future, I think the next recovery will be even weaker than the current one, which is already the weakest in the last 60 years – precisely because monetary policy is hindering growth.

Now combine a weak recovery with NIRP. If, in the long run, asset prices are a reflection of interest rates and economic growth, and both those are just slightly above or below zero, can we really expect stocks, commodities, and other assets to gain value?

The upshot is that whatever traditional investment strategy you believe in will probably stop working soon. Ask European pension and insurance companies that are forced to try to somehow materialize returns in a non-return world of negative interest rates.

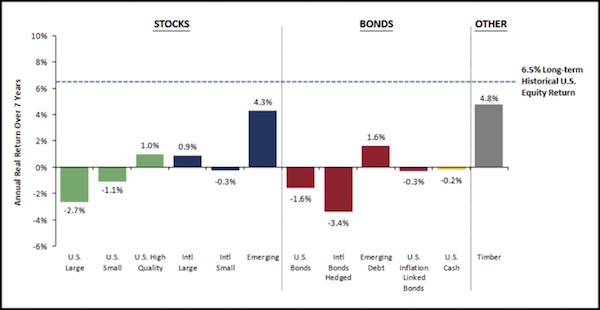

All bets may be off anyway if the latest long-term return forecasts are correct. Here’s GMO’s latest 7-year asset class forecast:

See that dotted line, the one that not a single asset class gets anywhere near? That’s the 6.5% long-term stock return that many supposedly wise investors tell us is reasonable to expect. GMO doesn’t think it’s reasonable at all, at least not for the next seven years.

If GMO is right – and they usually are – and you’re a devotee of any kind of passive or semi-passive asset allocation strategy, you can expect somewhere around 0% returns over the next seven years – if you’re lucky.

Note also that nearly invisible -0.2% yellow bar for “U.S. Cash.” Negative multi-year real (adjusted for inflation) returns from cash? You bet. Welcome to NIRP, American-style. Would you like that with fries?

The Fed’s fantasies notwithstanding, NIRP is not conducive to “normal” returns in any asset class. GMO says the best bets are emerging-market stocks and timber. Those also happen to be thin markets that everyone can’t hold at once. So, prepare to be stuck.

Your storytelling wannabe analyst,

John Mauldin

By Simon Mikhailovich

A committed landlubber until ten years ago, I took a few sailing lessons on a dare and unexpectedly discovered the joys of sailing. When a friend later asked if I would stand in for a crew member on his 18’ catboat during a Saturday race, I eagerly agreed, although his sturdy but slow boat didn’t look much like a racer. It turned out that being slow was not a problem in “one design” racing, just as it isn’t in today’s investment business. When one competes within the same class, it is through relative, rather than absolute, performance that one wins a trophy. It also turned out that much like investing, sailboat racing is as exciting as it is challenging. I got hooked and started racing my own sturdy and slow catboat, while learning as much about life, teamwork and investing as sailing.

This past Saturday, for example, we all drifted around the course hoping for a breeze. Indeed, the wind soon filled the sails, lifted spirits, and the boats started to move nicely... or so it seemed. After sailing briskly for about 15 minutes, we looked at the shore and realized we had been moving backwards! It happened because the prevailing tide was setting us back, even as our senses, the boat’s wake and its speedometer were all indicating forward movement. This episode was nature’s reminder that apparent progress should be never confused with making headway.

This is why for 5,000 years, a mariner needed a clear view of the skies to gauge his true position. Without the stars as fixed reference markers, there was no way to know one’s location. Similarly, for the past 5,000 years, market-set interest rates (the cost of scarce capital) and money anchored to tangible value have been financial stars that have guided capital allocation and served as a basis for setting asset values.

Today, reliance on the self-referencing economic models, epic debts, digital money printing and negligible to negative rates, have combined to blanket investors in the impenetrable fog from which no reference markers are visible. Having long forgotten how to navigate without models, investors and regulators are mesmerized by the virtual reality of computer-driven markets, where asset prices (including gold’s) are based on manipulated rates and measured on a USD (US Dollars) speedometer that conflates apparent, i.e. nominal, gains with the accretion of lasting purchasing power.

Recently, the U.S. Navy showed that it had a lot better sense than the U.S. financial regulators. Instead of waiting for a GPS cyber attack or malfunction to imperil its fleets, the Navy, after a 20 year hiatus, has reinstated mandatory celestial navigation training for all officer candidates. As Lt. Cmdr. R. Rogers of the U.S. Naval Academy explained: “We went away from celestial navigation because computers are great. The problem is, there’s no back up.”

As accurate as GPS is, economic and financial models keep proving to be anything but. Despite the Fed’s perennial forecasts of imminent recovery and higher rates, neither have materialized. Yields continue to decline and the debts continue to increase. Global debts are up 40% since 2007 to stand at $200T; there are still ~$660T in derivatives; and the utterly inane $13T (and growing) in negatively-yielding debts defy history and common sense. To top it all off, unable to lift rates without crashing the markets, all major central banks keep taking turns at the digital printing presses.

Despite the present and clear dangers, the markets and the global financial system continue to navigate by the rigged markers and operate without any back ups. As stocks and bonds and the USD keep hitting all time or near all time highs, complacency rules. Neither the regulators nor the investors want to question whether the profits are real or merely apparent. My own answer was unexpectedly reinforced last Saturday afternoon - apparent returns won’t fund your retirement any more than sailing against a faster current will get you where you want to go.

Until the monetary fog lifts and un-rigged navigational markers re-emerge, physical gold remains the only hard reference point capable of providing an essential back up plan for one’s nest egg. After all, just as the Navy took protective measures after realizing that no one can hack a sextant, investors should realize that no matter how many fiat dollars get printed, no one can print gold bars. The time to take protective measures is before they are needed. Now is that time.

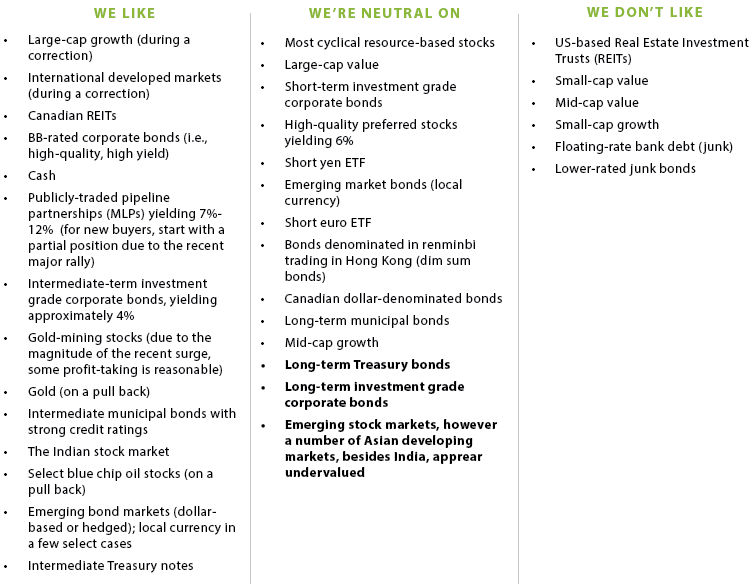

OUR CURRENT LIKES AND DISLIKES

Changes are in bold below.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.