"There are no atheists in foxholes or ideologues in financial crises."

-Fed Chairman BEN BERNANKE

1. The primary measure of stock market volatility, the VIX, recently hit 80, the highest level ever recorded. Even readings of 40 are considered extreme; thus, the current number is truly incredible.

2. The stock market collapse has been so intense that, according to the Wall Street Journal, 10% of all listed companies are trading below their cash holdings. This is comparable to what occurred during the Great Depression. Additionally, nearly 40% of all stocks tracked by Standard & Poor’s are trading at 8 times earnings or less.

3. Investment-grade corporate bonds have also been caught up in the selling frenzy, with some leading bond mutual funds having lost 25% or more year-to-date. Yield differentials (spreads) versus treasuries on junk bonds recently hit an unprecedented 15% and nearly 6% on high grade debt. This means their absolute yields reached 19% and 10%, respectively.

4. In one faint ray of hope for the credit markets, the prices of AAA-rated sub-prime collateralized debt obligations (CDOs) have risen from around 50 cents on the dollar to close to 60 cents. This may indicate that the government’s mortgage stabilization fund (TARP) might already be helping, even before it actually starts buying.

5. Retail gasoline prices have fallen from $4.11 in July to $3.03 recently (and are likely headed even lower). According to Merrill Lynch, each one cent decline in pump prices represents $1.3 billion in relief to consumers, amounting to roughly $140 billion overall.

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

Special note: If you’re like me, you’re fed up with standing idly by while chaos engulfs our financial system. Maybe I’m just doing this to feel better, and maybe I’m tilting against indifferent bureaucratic windmills, but this EVA is intended to address the frustration I feel and that I suspect many of you do as well.

The letter you’ll find in the second section is a slightly revised version of an article I recently wrote. This was picked up by a number of news services around the world, generating some interesting feedback, as I discuss below. The most critical aspect is that, if you agree with its content, I’m respectfully requesting you to forward it to your U.S. senators. If not, feel free to ignore it or email me with your objections.

We have attached links to Washington state US Senators Patty Murray and Maria Cantwell. We have also included a link for non-Washington residents to help you easily locate the e-mail address for the senators from your state. Additionally, we’ve included a link to the Federal Reserve site where they accept citizen commentary.

But before you decide to expend any effort, I should give you some background.

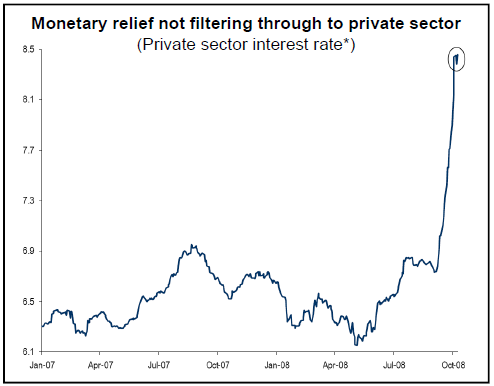

Watching in helpless dismay. As most of you know, more than two years ago I was writing about the impending disaster in the mortgage world. Even though I’m the first to admit that I never imagined it would turn out this horribly, it was still obvious to me that the regulators should have stopped the pandemic before it infected all of us. Then, for more than six months, I’ve expected the government to establish a stabilization fund to buy up depressed mortgages that have a high probability of eventually being worth much more—as opposed to letting their prices be forced down to senseless levels. Unfortunately, it took the Fed and the Treasury far too long to decide to do that; in fact, they still haven’t actually bought any mortgages (other than those issued by Fannie Mae and Freddie Mac). Meanwhile, in the wake of the collapse of Fannie and Freddie, and other major financial institutions, another grave threat for our markets and economy has rushed to center stage: The parabolic surge in yields high-grade corporate debt. Allow me to explain why that is such a big deal…

The spread’s the thing. It’s hard to overstate how crucial credit spreads are to both the real economy and the financial markets (credit spreads are the difference between what a corporation or a municipality has to pay over and above the yield on Treasury securities of a similar maturity). When these spreads widen in a major way, it’s a problem. When they rocket to the highest levels since the Great Depression, as they have done lately, it’s a catastrophe for several reasons. First, the cost of capital to corporate America rapidly rises, which is the last thing it needs right now. Second, financial entities that hold these items are often required to take losses related to their drop in value (as rates rise, the market value of a bond or mortgage declines). Third, leveraged holders such as many mutual funds and, particularly, hedge funds often become compelled to sell them, triggering a chain reaction of forced liquidation. Fourth, soaring credit spreads are almost always a very bad thing for the stock market and this time has proven to be no exception. Like so many other aspects of our current crisis, this cycle keeps feeding on itself until something stops it, which is the point of this EVA…

Crunch time. As I mentioned in the last issue, I’ve become convinced the Feds need to get very aggressive, very fast. The new bank support plan is an important step and you may have noticed it was modeled on the “kinder, gentler” European version. Fortunately, it is in stark contrast to the calamitous Paulson Doctrine of crushing common and preferred shareholders (and, in some cases, bondholders). In fact, if this approach had been used with Fannie and Freddie, as well as Lehman and AIG, there’s a pretty good chance we wouldn’t be experiencing this current market implosion. But it’s my strong conviction that providing additional capital to the banking system isn’t enough (and, despite the initial massive rally, recent market action confirms this). Collapsing asset prices are the ultimate problem. And it’s becoming painfully clear that only the government has the resources to prevent this vortex from sucking everything into its spinning funnel. Thus, as I alluded to in the preceding EVA, I believe that it is imperative for the Fed to become the bond buyer of last resort, as you will read in the attached letter. However, it seems that view struck a nerve with some modern day Ayn Rands out there.

My Andy Warhol moment. The aforementioned article managed to make it into both CNBC.com and Forbes.com before fading into oblivion, producing far less than 15 minutes of fame—maybe 15 seconds and even that’s probably an exaggeration. But before it disappeared into the slip stream of time, I received some feedback basically calling me (among other less than flattering things) a socialist, a heretic toward free market ideology, and a disbeliever in the efficient market theory (guilty as charged on that one!). Despite those responses, I am unwavering in my belief that the government should announce to the world that the garage sale in the corporate bond and preferred stock markets is over. From now on, there’s a new sheriff in town, he’s got an unlimited number of bullets, and he’s going to keep shooting until he’s got the town under control. Now, before your blood pressure skyrockets over the thought of more deficits, please read how this would actually be a profit generator to all of us taxpayers, far better even than buying depressed mortgage debt. So, if you will, please review the following letter and, if you concur, forward it on to the powers-that-be (or should be). Thousands of people now receive EVA, so maybe, just maybe, this idea might wind up in the right person’s in-box. Thank you very much for your consideration!

October 17, 2008

Dear Senator :

This letter is being sent to you due to the current crisis in the financial market which is now rapidly infecting the real economy.

While both the Federal Reserve and the U.S. Treasury department have recently initiated much needed actions to stabilize the banking system, it is clear that far more aggressive intervention is necessary, similar to what the Fed recently did in the commercial paper market. By directly acquiring commercial paper from corporations a complete and unimaginable liquidity crisis was averted; the Fed deserves great credit for this intelligent intervention.

However, the extreme stress in the corporate bond market, with yields on BBB-rated issues at levels not seen since the Great Depression, necessitates that the Fed moves beyond merely purchasing commercial paper—it needs to aggressively acquire longer term investment grade bonds as well as preferred stocks in the open market. And it needs to do so in whatever quantity is necessary to bring yields down to more normal levels.

This is in effect what the Treasury is preparing to do with the Troubled Asset Relief Program but would be much simpler and inherently safer for taxpayers. In fact, it would be virtually guaranteed to generate immediate and, eventually, significant profits for taxpayers.

The math is straightforward: the government can borrow in the short-term debt markets at rates around 2%. The average high-grade corporate bond is trading at 87 cents on the dollar and yields 8.5%, reflecting the extremely depressed state of the non-government fixed income markets. Just since Labor Day, high grade corporate bonds have declined an astounding 20%. According to The Wall Street Journal, investment grade corporate debt has not offered such high returns since the 1980s. Amazingly, this yield spike has occurred at a time of rapidly falling commodity prices and inflation, as well as during a time of collapsing risk-free interest rates. Thus, it’s unquestionable that both unbridled fear and forced liquidation are totally overwhelming fundamentals.

Prices are even more distressed in the market for preferred stocks; many investment grade issues trade at 60% of par value with yields approaching 12%. Consequently, Fed purchases of these securities would be even more lucrative for taxpayers.

Barring forceful intervention, further price declines are probable and could possibly accelerate. The implications of the credit markets collapsing are even more ominous than are those of the recent stock market plunge: as the cost of capital soars and buyers evaporate, even at exceedingly elevated yields, long-term financing for corporate America is essentially impossible. Just as destabilizing, financial institutions, including traditional insurance companies that did not participate in esoteric activities such as buying sub-prime CDOs and selling Credit Default Swaps, are now also under extreme pressure as their conservative portfolios plummet in value. This raises the specter of further rating downgrades and even more forced liquidation of bonds and preferred stocks.

Amplifying this disaster is the fact that myriad closed-end mutual funds own these securities with some degree of leverage. The breathtaking decline in the value of yield securities is endangering their debt coverage ratios, precipitating even more forced liquidation, effectively setting off a self-perpetuating cycle of margin calls. There is no doubt the situation is precarious in the extreme but it is definitely not hopeless.

This is one of those rare times when the Federal government can enjoy a high rate of return while at the same time producing an extraordinary societal benefit. Not only will it earn a fat spread between its cost of capital and lofty yields, the Fed and/or Treasury would be almost certain to realize substantial capital gains by investing large sums at irrationally depressed prices. Equally likely, once there is a bidder in the credit markets with unlimited resources preventing further absurd prices declines, and thereby driving prices back up, the astronomical sums of private money on the sidelines will be emboldened to join in the buying spree. Thus, an utter disaster can become, nearly overnight, a stunning victory.

By combining this effort with an equally aggressive plan to facilitate and ensure inter-bank lending, as the Fed is currently working hard to ensure, the overall financial system will receive a mammoth boost of confidence. We have unquestionably entered that stage of this credit cataclysm where fear, unless radically attacked and defeated, is now in the driver’s seat. Our government needs to commit all of its resources, and to do so at the points of maximum stress, in order to arrest this terrifying spiral of falling asset prices.

I respectfully request that you submit this proposal to the Senate Finance Committee at your earliest convenience.

Yours truly,

IMPORTANT DISCLOSURES: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.