“Each generation will reap what the former generation has sown.” -CHINESE PROVERB

“If everybody is thinking alike, then somebody isn’t thinking.” -GENERAL GEORGE PATTON

This month’s Gavekal-authored version of the Evergreen Virtual Advisor addresses what seems to be on everyone’s mind these days—you guessed it: The US presidential election. In fact, in my nearly 38 years in the investment business, I don’t think I’ve ever experienced such a singular focus on the part of investors (with the post-9/11/01 chaos a possible exception).

As you will read, this piece was written right before last week’s presidential debate, which most observers feel was a Hillary win. It includes a spirited opinion exchange with Gavekal’s three founders—Louis Gave, Charles Gave, and Anatole Kaletsky—joined by a fourth senior partner, Arthur Kroeber. As is the case with Evergreen, there is plenty of disagreement among the principals, particularly with regard to whether the US dollar and financial markets are likely to shrug off a Trump victory.

What jumped out at me as I read and re-read this piece, was Louis’ opening comment about complacency. In the September 23rd EVA, we ran a chart showing the unusually low volatility readings registered lately. This definitely reflects the relaxed attitude presently among the majority of investors (high volatility occurs during times of intense market fears while low volatility always occurs during periods when downside risks are ignored). Such insouciance strikes us as totally inappropriate relative to the increasingly hazardous global political, financial, and economic climate.

Actually, we may be in the early stages of a complacency reversal. In the opening days of October, we’ve seen some extreme weakness in the formerly red-hot equity income areas such as US REITs and utilities, the so-called bond proxies. (Fortunately, and knock on several cords of wood, energy infrastructure securities, such as MLPs, have mostly escaped the carnage.) The reasons for this shift are the Fed’s on-going chatter about raising rates in December combined with smoke signals from across the Atlantic that the European Central Bank (ECB) is having second thoughts about its money manufacturing/market manipulation scheme.

As noted for years in these pages, markets have become totally reliant on—and addicted to—the continual infusion of monetary amphetamines from the planet’s central bankers to maintain current price levels. Consequently, this twin threat to what we have called The Great Levitation is definitely causing a minor (so far) disruption in the prevailing market tranquility.

While it’s debatable which presidential candidate would be better (or less harmful) for the economy in the long run, there’s little doubt markets look at Donald Trump as a big wild card. Therefore, should the polls be wrong about his chances--as happened with Brexit, and, more recently, in Colombia (where the peace accord went down to a shocking defeat)—it would be another shot across the bow of the USS Complacency. Certainly, his China threats could cause Beijing to preemptively react, such as by allowing the renminbi to decline sharply should The Donald triumph in November. Recall that it was weakness in China’s currency in 2015, and earlier this year, that was among the prime factors causing two serious market corrections. And even though he’s looking and sounding more like Donald Grump these days, I wouldn’t count him out. He’s repeatedly shown a Teflon quality that would put Ronald Reagan to shame.

Speaking of shame, that’s certainly how I’m feeling about our country’s political state right now. But enough of my views…it’s Gavekal time!

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

By: Louis-Vincent Gave, Anatole Kaletsky, Arthur Kroeber, Charles Gave

As the world seriously tunes into the US presidential election, four Gavekal partners debate the outlook for the US dollar should Donald Trump emerge victorious and set about his promised remaking of the international security order and global trading system.

Louis: Investors’ complacency about a Trump win is huge for the following reasons: (i) most people think Trump can’t possibly win—that’s plain wrong, (ii) most people think that if Trump does win, he will be constrained by the “checks and balances” inherent to the US system—those checks work domestically, but in international affairs the US president has a largely free hand, and (iii) most people think that because Brexit was not a disaster for markets, democratic votes actually don’t matter and central banks “trump” everything—whatever else we at Gavekal disagree on, there is broad agreement that political risk associated with populist movements in the US and Europe being too easily dismissed.

Anatole: Your characterization of investor complacency is spot-on. I would add that the greatest immediate damage from a Trump win would be felt in emerging markets.

Louis: I’m not sure about EMs being first in the firing line. A Trump win will mean a weaker US dollar which is almost always good for EMs. Then you will likely see rising commodity prices due to heightened uncertainty. Both conditions are broadly good for EMs. Next, the political “discount” on EMs is likely to disappear as these countries will appear stable, while the OECD looks unstable. I can think of plenty of investors who will become sellers of US assets, but not many who will become buyers.

Anatole: I disagree with your starting premise, as a Trump win will likely lead to a stronger US dollar, potentially a much stronger dollar, as the fiscal spigots are opened up and inflation takes off in response to higher tariffs and labor shortages. At this point, the Federal Reserve will really start to tighten policy (before Yellen is fired in 2018). This is a variation of the strong-dollar scenario that Charles has been warning about.

Louis: When was the last time that high and sustained inflation led to a stronger currency? Inflation destroys the value of a currency! The likely collapse in global trade that would follow a Trump win points to a weaker US dollar, as does the inevitable foreign selling of US assets.

Anatole: Don’t forget that US CPI (ex-food and energy) accelerated from 3.2% in June 1983 to 5.3% in June 1984. The trade-weighted dollar surged by 25% in the same period, and a further 10% the following year as inflation stabilized at about 5%. Sterling also rose strongly in the early Thatcher period, even as inflation accelerated.

Louis: Yes, but that was driven by the bankruptcies in Latin America and the fact that every European bank had lent US dollars to the third world and was being forced to cover their naked shorts. Do you think we will have a repeat run with massive bankruptcies across EMs, triggering a US dollar short squeeze? I must say, I don’t.

Anatole: Why not, if Trump gets elected and tries to bankrupt every Asian and Latin American exporter?

Charles: I do not have a strong view on the US dollar right now. My only fear is that there remains a huge short position on the US currency. If, as Louis has suggested, some kind of secret deal was struck earlier this year between the big economies to maintain exchange rate stability, then a Hillary Clinton win is likely to result in stability. If, however, Trump is elected, then most shorts will seek to cover, and do so before the election. If there does remain a significant US dollar short position, then clear evidence of an impending Trump win will likely cause a fairly rapid appreciation of the dollar. Still, this is a low conviction call for me.

Louis: If, as I believe, a Trump presidency would mark the end of the US dollar as a reserve currency, this would be bullish for EMs, not bearish as one of the biggest constraints to their growth (access to dollars) would disappear. A Trump presidency is bearish for the US dollar as everyone and their dog are overweight US assets. Should Trump win, liquidation selling will occur first in US dollar assets, rather than in EMs where most people are underweight.

As I have argued all year, returns in emerging markets are being driven by US dollar and EM bond yield spreads. I think a Trump presidency possibly sees both fall. After all, Peron was not bullish for the Argentine peso, Chavez was not bullish for the Venezuelan bolivar, Brexit was not bullish for the pound and Le Pen would not be bullish for the euro. A Trump presidency means that foreigners are less likely to buy US assets and less likely to save in US dollars.

Anatole: Yet in times of geopolitical or financial panic, the US dollar is the ultimate safe haven currency, much more so than the Swiss franc or the yen. This has nothing to do with US military’s strength or foreign policy, but is simply because the US is the one major country that is completely impervious to foreign aggression and “will always be there”. Also, the US dollar is the numeraire and store of value for investors and businesses everywhere, especially in emerging markets. This could change over many years or (more likely) decades, but certainly not in just a few months.

Louis: I think this is a narrow view that equates a Trump victory to one of the recent shocks we have had. Meanwhile, a Trump win would be more akin to Richard Nixon breaking the Bretton Woods agreement. A few years ago, it was fashionable to say that we lived in “Bretton Woods II”. To me, a Trump victory would definitely be the end of that Bretton Woods II. Remember the end of Bretton Woods I saw a collapse in the demand for dollars and surging demand for gold.

Arthur: I’d also see the US dollar as a likely beneficiary of a Trump victory. The US dollar-as-safe-haven is a powerful force (remember in 2008 how a US-based financial crisis led to a jump in the dollar), although given Trump’s weirdness I’d expect the other safe haven default, the yen to also do well. I’m not sure that the pound sterling/Brexit analogy (or any of those Latam analogies) holds, since the US dollar is the global reserve currency and the pound is an optional holding for most.

To the extent that there is a consensus view on the economic consequences of a Trump presidency, it is that he would create a sharp recession. So equities could well sell off, but bonds would rally on this expectation as well as the safe haven effect (notwithstanding Trump’s assertion that repayment of treasuries is “negotiable”!). The problem with investors exiting the US dollar as the global reserve currency is that they would need something to exit into. And there are no plausible candidates.

I wonder, however, if there might be some second-order effects favorable to EMs. For example, China’s response to a rise in the US dollar may be to lay on stimulus in order to fend off a potential global recession. This could have a positive feed-through to commodity prices and EM financial asset performance, although it would bring the eventual crystallization of problems in China that much closer.

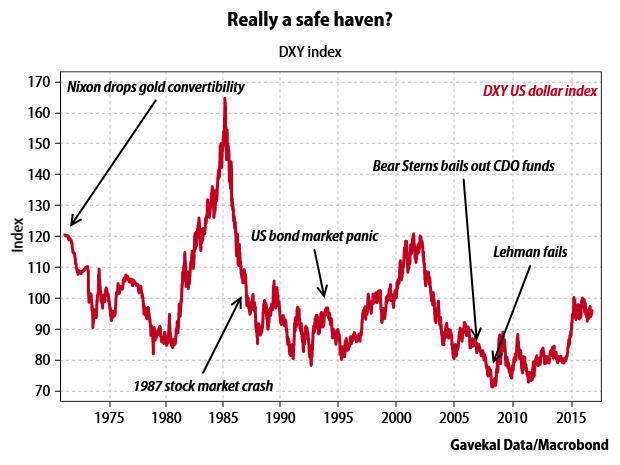

Louis: If the dollar is such a haven, why did it fall precipitously after Nixon’s de-pegging from gold, the 1987 stock market crash, the 1994 bond market panic and the initial rumblings of the 2007-08 crisis. After all, these events all reflected a financial panic. Or what about the panic that befell markets early this year when MSCI World rapidly lost -10% and the DXY index fell -2.5%. I just see no basis for the safe-haven argument.

Arthur: It’s one thing to say that a Trump victory in November would lead to a sell-off in the dollar. Frankly I think that is unlikely; there might be panic selling in the few days after the election but the longer-term impact would probably be for markets to ratchet up their expectation of a US recession, which in turn would take a Fed rate hike off the table and thereby increase the appetite for US bonds and hence the dollar. But I could well be wrong on this.

It is quite another thing, however, to forecast the end of the post-World War II order and most of the institutions that were put in place at the time. That order is very sticky and cannot be undone by the election of an eccentric, but ultimately vacuous, character to the White House. There’s no doubt that under Trump the US would become a more protectionist place, and cyclically this would be bad for the world economy. For the global order to fall apart, though, there needs to be some alternative set of arrangements for everyone to flee to. No such set of arrangements exists. There is no alternative to the US dollar as a global medium of exchange and store of value; there is no alternative to the US military as the guarantor of global security; and there is no alternative to US orchestrated geopolitical institutions as a safeguard against the law of the jungle. The US system could lose its primacy through severe mismanagement over many decades. It will not do so by virtue of four or even eight years of feckless incompetence by Donald Trump.

Louis: I will concede your point on an overnight demise of the dollar as the reserve currency, but it is interesting how quickly the Philippines, a former US colony and in the post-World War II period a loyal supporter in Asia, is pushing US troops out of Mindanao and moving its weapons purchases from the US to Russia and China. How long will it be until Rodrigo Duterte tells the central bank to move half of its reserves from (low yielding) treasuries into Chinese government bonds? If you take the view that a Trump presidency reflects a “bankruptcy” in the US—moral bankruptcy, intellectual bankruptcy, financial bankruptcy, and Lord knows The Donald knows about bankruptcies—how can this not be reflected in the value of the currency? As the French economist Jacques Rueff once said: “The currency is the price through which the distribution of unearned rights is paid.”

However, on the substantive point of the dollar’s key drivers in the coming period, we must not lose sight of the fact that the only consistent rule of markets is that pricing is made at the margin. Hence, the market’s direction will more often than not depend on positioning heading into a “problem” period.

Let me put it this way, why did the dollar soar after Lehman went bust? Was it that (i) investors everywhere thought “holy ****, trouble ahead. Quick, buy US assets” or, (ii) market players had borrowed heavily in US dollars in 2002-08 in the belief that the dollar could only go down (twin deficits and all that) and as Lehman Brothers went bust, banks cut credit lines forcing a massive margin call. The answer can be found from a quick look at spreads, price action and financial flows at the time. Simply put, people were only buying if they had no choice (i.e. puts being activated and accumulators being called in). It is clear that the dollar’s spike stemmed from credit lines being pulled.

Which brings us to today and two key questions we should ask ourselves, namely, (i) have we just gone through a 2002-08 period, when everyone thinks the US dollar can only go down, and (ii) are market players leveraged up in US dollars as they were in 2008, leaving them vulnerable to a withdrawal of credit lines? My answer to the first question is “no, quite the opposite”. The market as a whole is overweight the US dollar and dollar assets on the premise that the US is the best house on a bad street. My answer to the second question is a slightly less emphatic, “no”. Unlike Charles, I am skeptical that US leverage by non-US actors is that high. Since the 2013 “taper tantrum” and especially since last summer’s renminbi “devaluation shock”, it seems that people have busily paid back US dollar debt. Hence, I am not so sure that a Trump victory means that credit lines get pulled, as was the case right after Lehman.

A bull case for the US dollar rests on foreigners responding to a Trump win by buying more US dollar assets at a time when they are already massively long. In fact, the opposite will likely happen, and I speak here as a foreigner who owns US dollar assets! Absent Trump adopting rules that stop US banks from lending abroad, it is hard to see foreigners being caught in an epic short-squeeze of the sort that Anatole posits. Moreover, given that Trump’s whole trade agenda is focused on winning back manufacturing share for US firms, such a move would be hugely counterproductive.

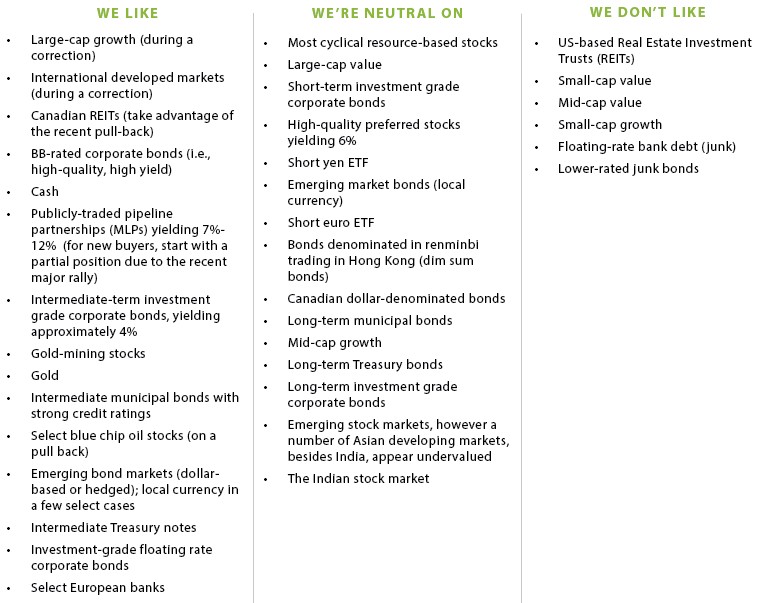

OUR CURRENT LIKES AND DISLIKES

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.