“All investment frenzies pass. The market is gloriously inefficient and wanders far from fair price but, eventually, after breaking your heart and your patience…it will go back to fair value. Your task is to survive until that happens.”

-JEREMY GRANTHAM, co-founder of GMO, one of America’s largest investment advisors.

Note: For a quick recap of some important questions facing investors in the stock market today, please see the final section of this week’s EVA titled “The two-minute drill.”

Buy-and-hold, the path to gold? Nearly 25 years ago, Jeremy Siegel’s book, “Stocks for the Long Run”, hit the market. It was an instant bestseller, at least by financial book standards. His timing was propitious, since it came out in the middle of the biggest bull market in history.

His basic premise—that stocks are sure winners over time—has certainly been borne out by the returns on the S&P 500 since his book was first published. To wit, the S&P has produced a total return of 9.7% annually from the 1994 publication date of “Stocks for the Long Run” through March 31st of this year. Case closed, right? Maybe not.

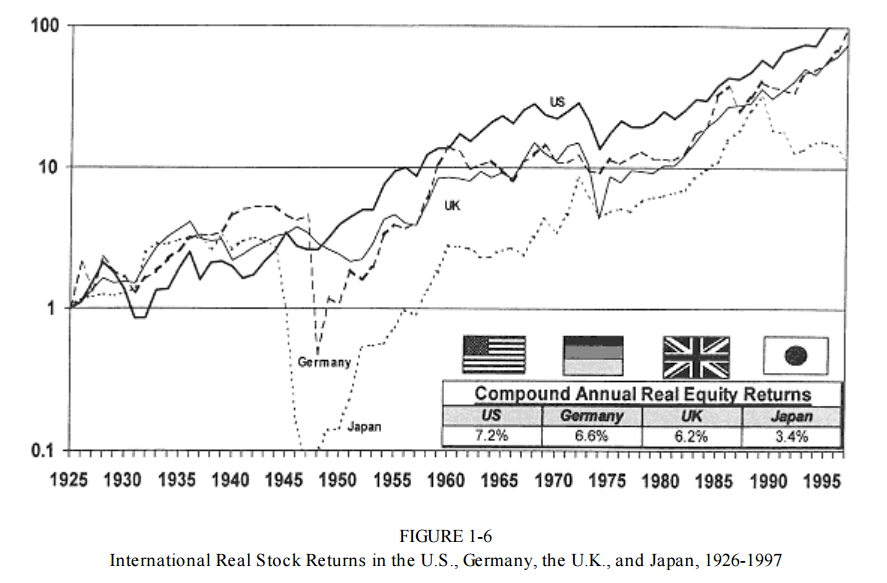

One of Professor Siegel’s critical points is that if you hold stocks long enough—like 20 years—it doesn’t matter how expensive the market was when you first invested. Even wars and total economic collapse, such as Japan and Germany endured, did not prevent positive returns from being achieved, at least looking back from the vantage of 1994.

Source: Jeremy J. Siegel, the Wharton School of the University of Pennsylvania

Yet, ironically, the performance of the Japanese market itself since then is a glaring exception. As most EVA readers are aware, Japan experienced dual bubbles in stocks and real estate in the 1980s, until they catastrophically burst in 1990. Now, some 27 years later, the total return on the Japanese index has been roughly minus 30%. So much for the infallibility of a long enough holding period! However, I guess, even nearly 30 years isn’t up to Warren Buffett’s preferred ownership timeframe—as in, forever.

Yet, for us Baby Boomers, who are increasingly the most numerous bag stockholders, “forever” is way too long to wait for acceptable returns. Even Professor Siegel’s “sure thing” length of 20 to 30 years doesn’t work very well for the “Me Generation.”

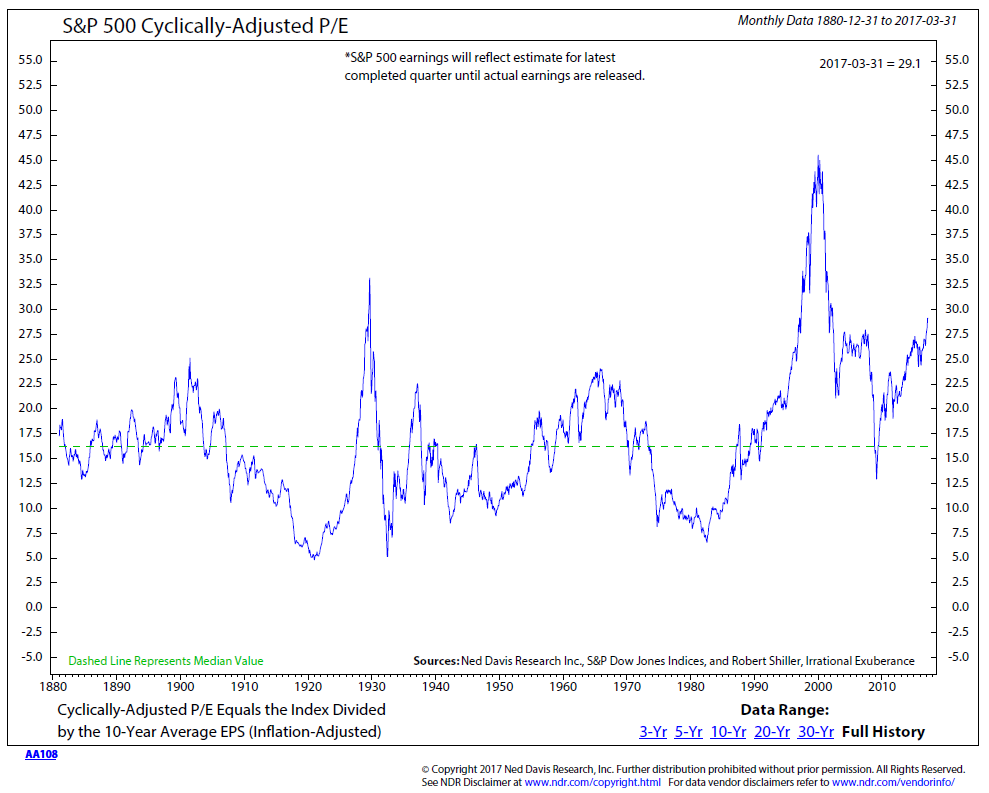

But let’s accept that Japan was a rarity caused by insane overvaluation. That could never happen in the good old US of A, right? Except that a mere five years after Professor Siegel wrote his book, the valuation on US stocks exceeded what was attained during what most Americans probably still feel was the zenith of the greatest domestic market mania of all-time—the infamous year of 1929.

Source: Ned Davis Research

Source: Ned Davis Research

As you can see above, by the end of 1999—almost 70 years after the ’29 crash—the US stock market was actually more expensive on a valuation basis than it was when buying stocks with just 10% down (i.e., 90% on margin) was commonplace. Optimists can point out that the market “only” de-rated by 49% during the 2000 to 2002 bear market but that understates the carnage. This is because during the late ‘90s most investors were intoxicated with the tech-heavy NASDAQ and the “NAZ” vaporized by nearly 80% over those grueling two and a half years. The difference compared to the 90% nuking stocks took from 1929 to 1932 was negligible. (By the way, even investors in a plain-vanilla S&P 500 index fund in those days were heavily tech-exposed; this is because nearly 50% of the S&P was in technology and telecom issues at the time.)

Now, 17 years after the peak of the late 1990s-stock bubble, the market would seem to have pretty much vindicated Professor Siegel’s views that time heals all stock wounds. The “pretty much” comment relates to the reality that stocks have returned a tough-to-live-on 4.7% since 12/31/99. Net of taxes and inflation, you’re talking maybe 2% a year.

But the bigger problem is yet to come…

When euphoria collides with a double-tightening. Anyone who doesn’t think a bear market is inevitable is clearly delusional. To (almost) quote the great financial guru, Forrest Gump, “Stuff Happens!” Let’s assume we dodge a serious shakeout for another year, stocks rise a further 10% from here, and then there is a garden-variety 30% bear market over the next 12 months. That would put the market around 1800—interestingly, around where it troughed in February of last year. At that point, the per-year return on the S&P 500 from 12/31/99 over a period of nearly 20 years would be a measly 3.1% per annum.

Should the decline be deeper, as is highly likely after so many years of artificially muted downside volatility (caused by central banks), the numbers will, of course, be even more dismal. Let’s make the same assumptions as in the forgoing paragraph but use a 50% vs a 30% decline. That would mean about 1300 on the S&P sometime in 2019—again, assuming a 10% additional increase prior to the plunge—below where it closed in 1999. If it falls this far (remember that the S&P plunged 49% from peak to trough in 2000 – 2002 and 57% from the 2007 apex to the early 2009 bottom), then the total return—i.e., including dividends—for almost twenty years from the main US stock index would be a paltry 1.4%. And that’s before subtracting inflation and taxes which would push the effective return into the red.

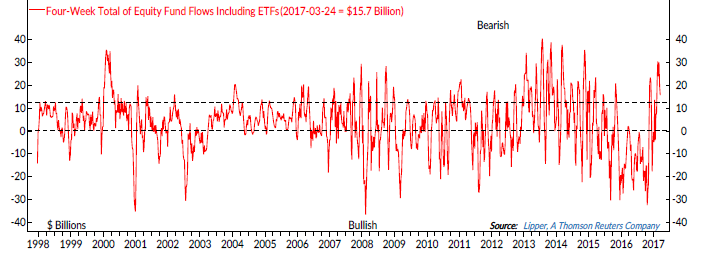

Under either one of these scenarios, it’s highly probable that the currently wildly popular and closely related notions of buy-and-hold-forever, as well as the supposed superiority of passive (i.e., index) investing, will begin losing adherents at the speed of a Tomahawk cruise missile. The behavior of the majority of investors over the last 17 years reveals scant willingness to buy into severe market declines. In fact, the polar opposite has been on display in each of the two aforementioned bear cycles. Massive outflows from equity funds occurred during both 2000–2002 and 2007–2009, despite the “50% off” sale that should have, rationally, attracted legions of bargain-hunters. (In fact, investors ran for the exits en masse even during the two mild pull-backs in the summer of 2015 and early 2016.)

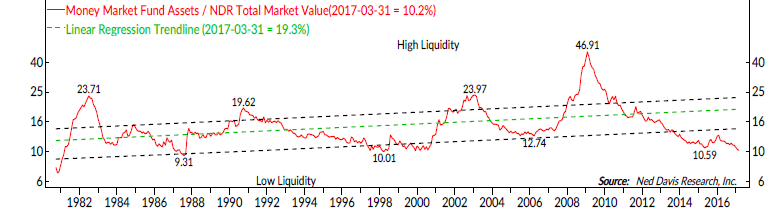

INFLOWS (ABOVE THE LINE) + OUTFLOWS (BELOW THE LINE)

FROM ALL EQUITY (STOCK) FUNDS FROM 1998-2017

Source: Ned Davis Research

Source: Ned Davis Research

This means that the millions of folks who are convinced about the lack of meaningful downside risk and the merits of “brain-free” investing are in for a most rude awakening. However, the odds are fairly high that such a reckoning is not right around the corner, even if it might be lurking in the neighborhood.

As expressed in various EVAs over the last few months, the stock market’s trend is clearly up. The various trend-following indicators used by our friends at Ned Davis Research have had an exemplary long-term track record and these remain definitively positive. (This does not preclude another correction, however.)

We’ve also noted in these pages that the stock market tends to continue to rise in the early-to-middle innings of a classic Fed rate-hiking campaign. We’ve been opining since the start of the year that this is exactly what we’re facing now, with the added kicker that it’s likely to be a “double-tightening”. The latter term means that not only are rates likely to be raised multiple times, but that also our central bank is finally telling the world it is preparing to put its Sumo wrestler-sized balance sheet on a diet. Practically speaking, later this year or early in 2018, once it has raised rates up to the 1 ½% to 2% range, it will then halt the reinvestment of its $4.5 trillion portfolio (all of which was purchased with money it created out of nothing but digital bits and bytes). This will amount to draining liquidity from the financial system. Additionally, this will theoretically happen at a time when the market has had five or more (we think more) rate increases thrown its way.

That isn’t a felicitous combination for a market millions of investors seem convinced can only go higher.

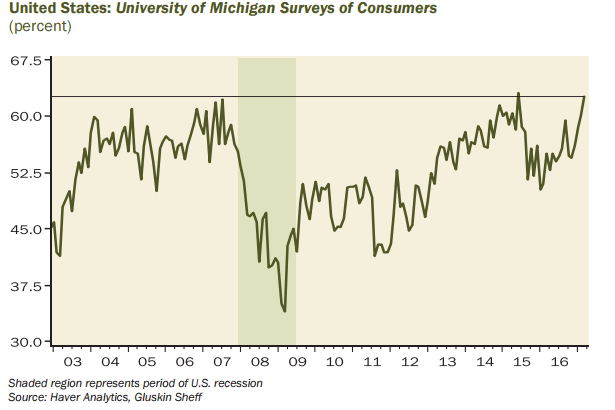

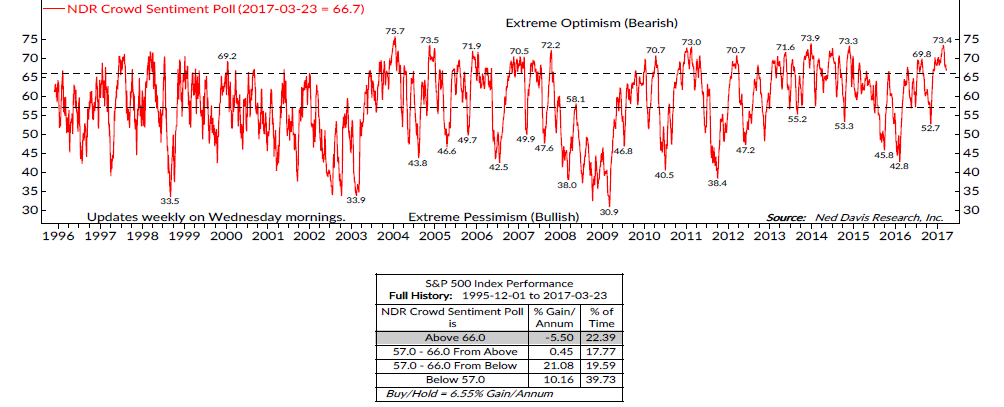

Extreme investing. To justify that last comment, a recent University of Michigan survey found that US consumers are as optimistic about the stock market as they were in 2007 and 2015.

PROBABILITY OF INCREASE IN STOCK MARKET NEXT YEAR

Source: Haver Analytics, Gluskin Sheff

Source: Haver Analytics, Gluskin Sheff

Obviously, the first instance was one of the worst times in history to be bullish on stocks. But even mid-2015 wasn’t ideal because of the aforementioned 12-15% corrections that followed shortly thereafter. This leads me both to a confession and also a discussion of the usefulness of extreme sentiment readings.

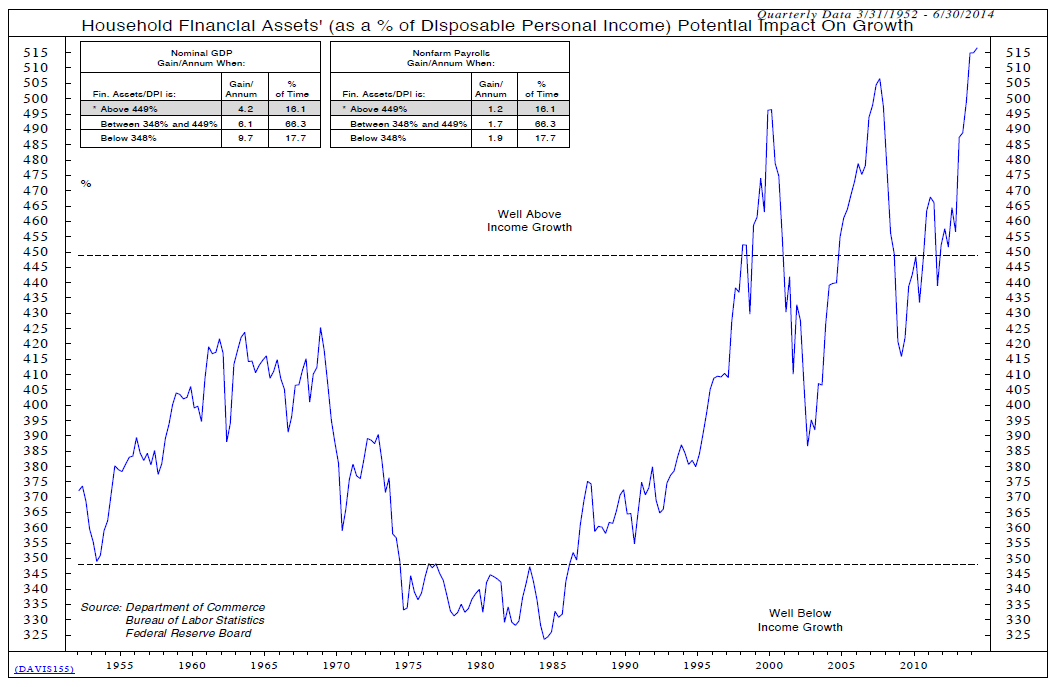

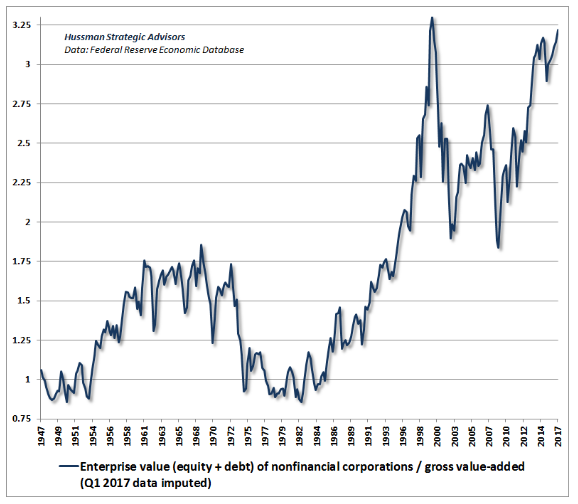

As I have admitted before, it’s been extraordinarily difficult to be a value-conscious investor (that would be Evergreen) over the past three or four years. Stocks have stayed beyond pricey for much longer than I’ve seen in my almost four decade-long career. To prove my point, consider the following chart, from the treasure trove of market data at Ned Davis Research.

Source: Ned Davis Research

Source: Ned Davis Research

As Ned, “da man” himself, wrote in the text that accompanied this graphic: “Never in history have household financial assets been higher relative to the disposable income that must support these assets and the humongous debts behind them. If the Fed has created a financial assets bubble, it makes it very tricky to unwind its stimulus.” As I’m sure will surprise nary a single EVA reader—at least one who has been subjecting herself or himself to our musings for very long—there is no doubt in my mind that the Fed has done precisely that. And, certainly, the chart Ned ran makes it LCD-clear that it’s the third monster asset inflation since the late ‘90s.

But look closely at the date in small print at the upper right part of the chart. Let me help all my fellow Boomers who struggle with small print: It reads from 3/31/1952 to 6/30/2014. In other words, this was almost three years ago! In case you were wondering, this condition is virtually unchanged since then.

Now, that’s a long time to be waiting for mean reversion! The fact that stocks have seemingly attained a permanently higher plateau (as Irving Fisher once famously—and disastrously—said in the late 1920s) has been very pleasing to perma-bulls like Jeremy Siegel. Conversely, it has been just as vexing to another Jeremy, this one by the last name of Grantham.

Super-astute EVA readers may remember that we ran a short piece several years ago, titled “The Two Jeremys”, based on a debate these two luminaries had back in 2007. As usual, Jeremy S. was bullish while Jeremy G. was bearish (the latter is not always so inclined; in fact, he recommended buying stocks circa early 2009 in a wonderfully named missive: “Investing While Terrified”). We certainly know whose view was vindicated as the next few years unfolded—and markets imploded.

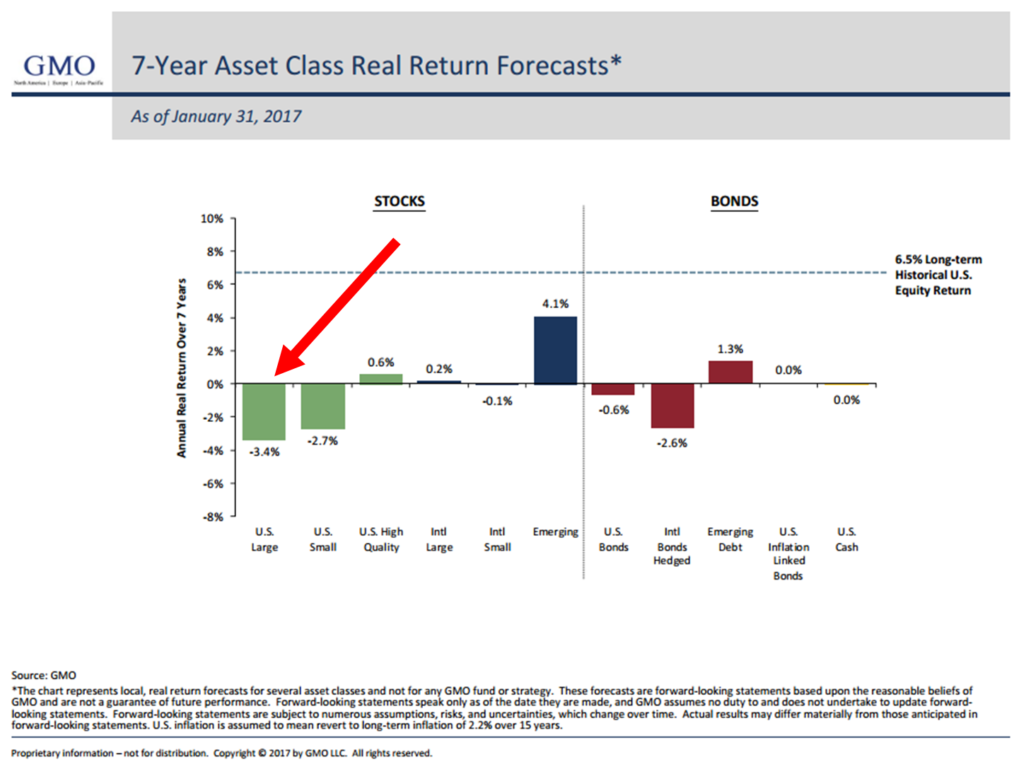

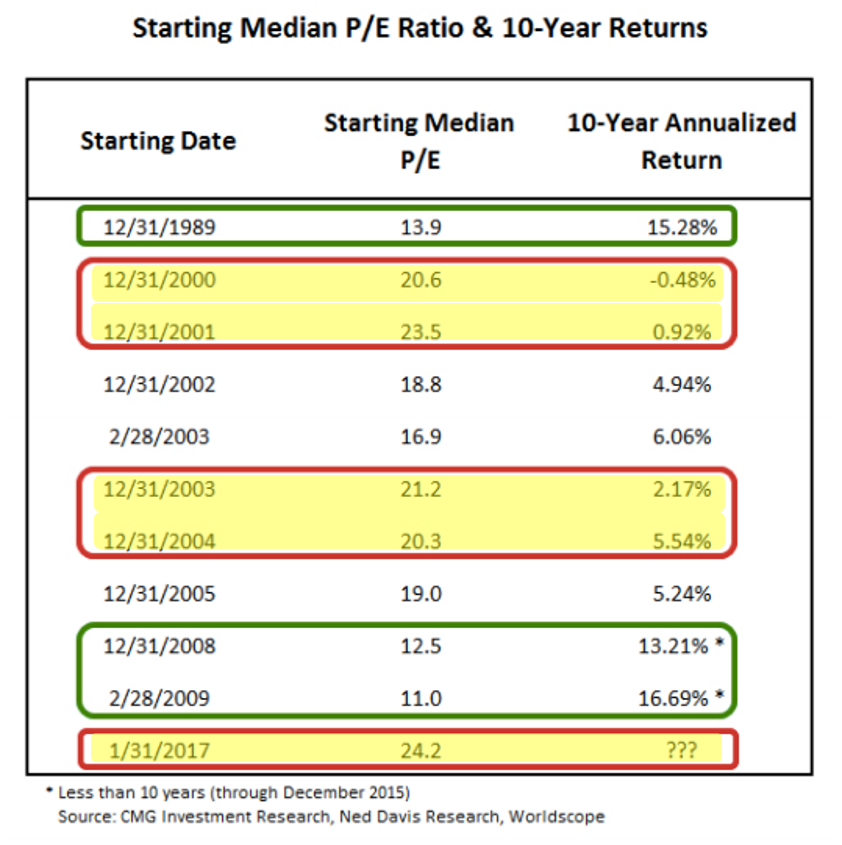

Fast forward to today… Once again Jeremy Grantham and his firm, GMO, have been battening down the hatches while Jeremy Siegel remains resolutely bullish. As a result, GMO has been bleeding assets (i.e., clients are defecting) as they did in the late ‘90s and also in 2007. Putting out a chart of projected future returns, such as the one below GMO recently published, isn’t great for either business development or client retention—certainly not in a relentless bull market, at any rate.

Source: CMG Capital Management Group

Source: CMG Capital Management Group

Numerous past EVAs have sung the praises of how well GMO’s long-term asset class return forecasts have turned out; but, I haven’t backed that assertion up as well as I could have—until now. A recent analysis by the highly respected Mark Yusko found that there has been a 97% correlation between what GMO has projected and how things like US stocks, emerging market debt, et al, have actually performed in the fullness of time. Ergo, investors should definitely pay heed to what GMO is saying presently, despite their recent “out-of-syncness”.

Yet, notwithstanding their exemplary forecasting record, they are almost always early, often painfully so, and this leads me back to the importance of extreme sentiment readings. By this, I mean that when retail investors, and/or those of a more speculative bent, are ragingly bullish or bearish, it almost always pays to position against that unanimity.

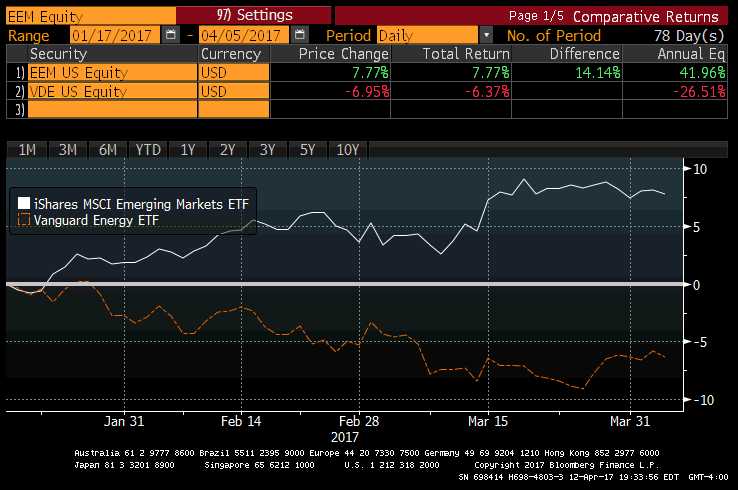

As a case in point, consider what occurred earlier this year between emerging markets (EM in the chart) and energy stocks. Per the below graphic, you can see that sentiment was negative on the former and euphoric on the latter back in January.

RELATIVE FMS POSITIONING: EM EQUITIES VS. ENERGY STOCKS

Source: BofA Merrill Lynch

Source: BofA Merrill Lynch

And here’s what happened since then: The VDE (Vanguard Energy ETF) pulled back by 6.4%, while the EEM (Emerging Market ETF) increased by nearly 8% for over a 14% divergence. That’s a meaningful deviation in a fairly short time.

Source: Bloomberg, Evergreen Gavekal

Source: Bloomberg, Evergreen Gavekal

This is by no means an isolated occurrence. It has happened repeatedly in the post-financial crisis era, possibly because there is so much trend-following, momentum-driven money coursing through financial markets these days. Consequently, prices get bid up very quickly. They are also driven down, it seems, even more expeditiously. Thus, extreme positioning appears to be happening more frequently, and to a greater degree, than in the past. This leads me to the confession part.

While, over the last year, Evergreen has been successfully using extreme sentiment readings to position against these (such as recently buying longer bonds when negativity was overwhelming), we should have done so sooner and more aggressively. For example, when small caps were pounded down by 27% from their peak in 2015 to their nadir in February of last year, and speculative short interest was Himalayan high, we should have covered most of—or even all of—our small cap short/hedge position.

The point is that even though valuations are extremely stretched by any measure that has worked well over time (fyi, the so-called Fed model of comparing P/Es to interest rates has not), there are still trading opportunities on which to capitalize. Admittedly, the best combination is when pessimism is so severe and persistent that it grinds valuations down to bargain levels, as happened with energy issues in 2015. (For more on this topic, I recently did a short audio interview with Aaron Chan from Real Vision that can be accessed here.)

Yet, this type of buying into deep pessimism and selling into frenzied optimism is the antithesis of buy-and-hold. But, it’s working and we believe it will continue to do so as long as trillions of dollars flow into no-think securities that feed the fads.

The two-minute drill. To close this EVA edition, I’m going to attempt the financial newsletter version of Chris Berman’s rapid-fire football highlights on ESPN. In this case, I will throw a flurry of pointed questions at you instead of game-breaking plays.

Source: The Credit Strategist

Source: The Credit Strategist

Source: Ned Davis Research

Source: Ned Davis Research

Source: Hussman Funds

Source: Hussman Funds

Source: Mauldin Economics

Source: Mauldin Economics

Source: Grant Williams

Source: Grant Williams

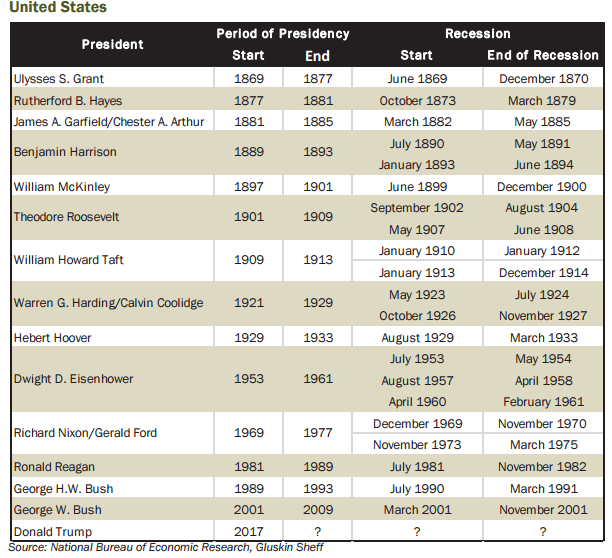

GOP PRESIDENTS AND RECESSIONS

Source: Haver Analytics, Gluskin Sheff

Source: Haver Analytics, Gluskin Sheff

Source: Ned Davis Research

Source: Ned Davis Research

As a result, those of a buy-and-hold nature need to be prepared for another long stretch—such as we’ve seen since January of 2000—of disappointing stock returns. Of course, if you are willing to focus on Jeremy Siegel’s 30-year time frame, you’ve got nothing to worry about…I hope.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.