This week’s edition of the Evergreen Virtual Advisor (EVA) is a return to one of our most popular formats, the Evergreen Exchange. This structure gives three members of our investment team the chance to agree, disagree, or simply comment on a topic of interest.

The theme of this issue revolves around common misconceptions in the market. First, Jeff Dicks outlines his view that the market is misguided by the prevailing sentiment that longer interest rates have nowhere to go but up. He makes a compelling case, highlighting key economic indicators to support his argument. Next, Jeff Eulberg argues that the “Trump Bump” has been buoyed by hope rather than concrete changes. He urges investors to keep a watchful eye on indicators of a market correction. Finally, Tyler Hay discusses the rise of robo-advisors in the financial services world, and whether or not they will be able to answer the call during the next bear market.

As we often do with our Exchange issue, we ask readers to select which case was made most persuasively. We would greatly appreciate it if you’d take the time to submit your vote here. Thank you!

One of the most common market misconceptions is that long-term interest rates have nowhere to go but up. Over the last six years, we have heard this touted by the media and some of the world’s most renowned bond investors. As the chart indicates below, we have yet to break a downtrend for interest rates that began in 1981.

Annotations A and B represent points in time where Bill Gross, once nicknamed the “King of Bonds” (dethroned by Jeff Gundlach), flipped bearish on bonds. The first instance (A) was in March of 2011, when Gross claimed rates were far too low and subsequently took a short treasury position in his Pimco total return fund. The second, (B), was during the 2013 “taper-tantrum,” when Gross pronounced an end to the secular bull market. In hindsight, both instances turned out to be exceptional buying opportunities. With the 10-year treasury yield recently crossing above a key resistance level of 2.60%, Gross (now CIO of Janus Capital) is again predicting the end of the nearly 40-year bull run for bonds.

10-Year Treasury Yield

Source: Bloomberg, Evergreen GaveKal

Annotation A – 3/11/2011: “Yields are too low. ‘Treasuries’ need to be ‘exorcised’ from model portfolios and replaced with more attractive alternatives both from a risk and a reward standpoint.” –Bill Gross

Annotation B – 5/10/2013: “The secular 30-year bull market in bonds likely ended 4/29/2013.” –Bill Gross

Annotation C – 1/10/2017: “The 10-Year at 2.6% will mark an end to the 30-year bull market in bonds.” –Bill Gross

As the Federal Reserve continues its current course of raising short-term interest rates, we have seen another notable spike in financial media ink calling for the end of the bond bull market. Thus, it seems like the opportune time to weigh in on whether this is truly the end of the nearly 40-year bull run for bonds, or if it’s merely another dip in bond prices that should be considered a buying opportunity.

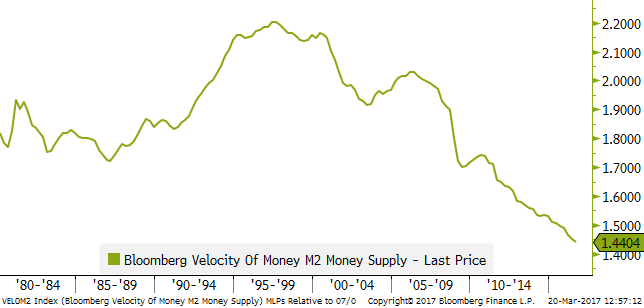

Follow the money. One key variable to monitor when forecasting interest rates is the velocity of money. Essentially, this metric measures how often a unit of currency changes hands during a given period. The quicker money changes hands, the more robust an economy tends to be. This leads to both higher inflation rates and higher interest rates. As shown below, there have been persistent declines in the velocity of money during this cycle, leading to the weakest recovery on record. Subdued inflation readings have, in turn, kept rates in check. If velocity continues to implode, it’s likely longer rates stay contained with no reason to expect a major reversal.

Velocity of M2 Money Supply

Source: Bloomberg, Evergreen GaveKal

Excessive global debt levels. Another factor inhibiting growth is total debt levels relative to GDP. The Hoisington Investment Management Company and their Executive Vice President, Lacy Hunt, do an exceptional job tracking this metric. Hunt has been one of the few bond managers to accurately predict lower interest rates during this cycle, maintaining his bullish stance on long-term treasuries. Hunt currently calculates total US debt at “more than $69 trillion, or 370%, of GDP.” Additionally, he calculates this total is “350% for China, 450% for the Eurozone, and over 600% for Japan.” In layman’s terms, the world simply has too much debt outstanding relative to economic production. Academic studies have found that when this metric eclipses 250-300%, new debt begins to slow economic growth, which causes the velocity of money to fall further and puts even more downward pressure on inflation and interest rates. As such, the developed world needs to drastically reduce overall leverage. The problem is that deleveraging inhibits growth as an economy must sacrifice current consumption levels in favor of paying down debt.

Look for extreme positioning. One of the best indicators of interest rates over the past eight years has been speculative positioning in the futures market. The lower pane in the chart below illustrates how traders are positioned ((total longs – total shorts)/total shorts). For instance, in mid-2012, the chart shows that positioning moved to more long-interest relative to short-interest. This contrarian indicator proved bearish for bond prices, pushing yields higher. Conversely, excessive pessimism, or much more short-interest relative to long-interest, is usually a bullish indicator for bond prices. The chart below shows an example of this during the “Taper Tantrum” of 2013. When positioning moved decisively bearish following a spike in interest rates, it turned out to be an excellent buying opportunity. Currently, there is a bearish reading on the futures market for treasuries. This has us projecting a near-term rally for bonds.

10-Year Treasury Yield and Open Interest

Source: Bloomberg, Evergreen GaveKal

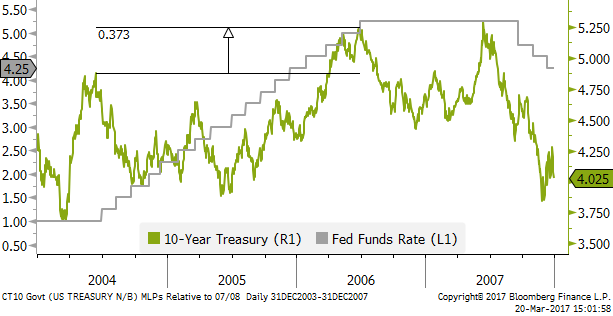

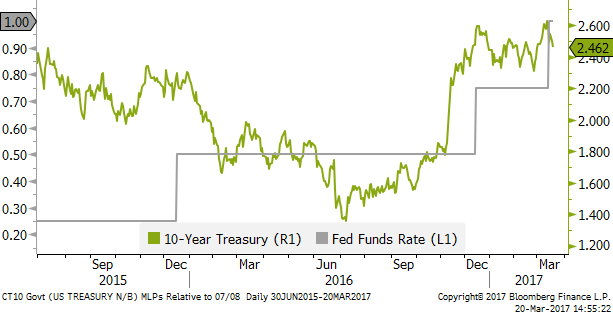

At this point, the Fed is your friend. The next idea is one our CIO, David Hay, has relayed in recent newsletters and is critical given the current environment—that most bond market damage tends to come early in tightening cycles. As shown in the lower left chart, the 10-year treasury yield moved up over 1.0% following two interest rate hikes during the 2004 tightening cycle. However, it was only 40 basis points (0.4%) from its ultimate peak with two full-years of future hikes still to come. Today, there has been a similar upward move in treasury yields after, again, only two hikes. If we are to compare past and present cycles, and project the same outcome, the 10-year should peak around 3.0%. At this point, we think it’s more likely the yield curve continues to flatten as the Fed hikes rates. Thus, just because the Fed is raising short-term rates doesn’t mean long-term rates will move up in lockstep.

10-Year US Treasury Yields and the Fed Fund Target Rate

Source: Bloomberg, Evergreen GaveKal

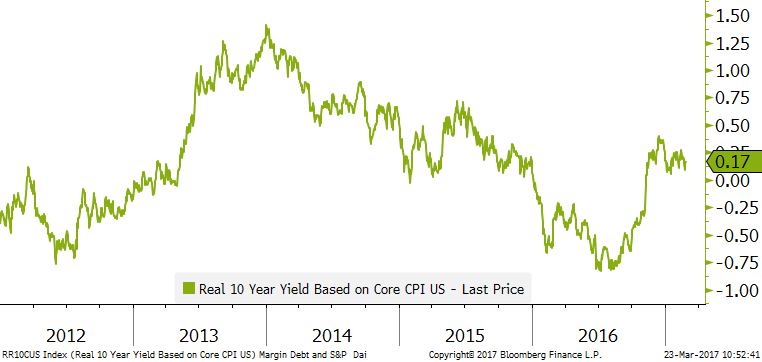

Real rates lower for longer. Conversely, real (after inflation) yields are stubbornly low. Subdued inflation and weak growth have contributed to this, but central bank policy has exacerbated the issue. Specifically, the Bank of Japan (BOJ) and the European Central Bank (ECB) are in full-fledged easing mode. The Fed, despite cutting off its QE program, is still reinvesting its $4.5 trillion balance sheet. These policies continue to suppress interest rates. The real rate on the 10-year U.S. Treasury averaged 2.5% from 1960-2011. Since then, the real rate on the 10-year has averaged a measly 0.4%. Currently at 0.17%, we are not advocating this is a solid long-term return proposition. However, if we continue to operate in an environment manipulated by central banks, U.S. Treasury yields look reasonably attractive compared to other developed markets. For instance, the real yield on the 10-year German Bund stands at -2.0%. Central bank policy is critical to watch moving forward, but despite historically low real yields, U.S. interest rates offer reasonable relative value. Moreover, during the next recession, inflation is likely to fall—perhaps meaningfully—raising real yields.

Real 10-Year Yield Based on Core CPI

Source: Bloomberg, Evergreen GaveKal

Conclusion: Be tactical, buy the selloffs, but fade the rallies. In summary, we do not believe we are entering a secular bear market for bonds. While we concede that global rates are unlikely to go much lower than their mid-2016 lows, one should consider buying into steep selloffs as the market enters a sideways trading range. But remain tactical. The economy carries far too much debt and higher interest rates will have a spillover effect on the real economy.

Additionally, as the Fed continues its path to normalize short-term interest rates, we believe growth will slow further. This will ultimately put downward pressure on long-term rates as investors seek safety, causing the yield curve to invert. Historically, this has been the best indicator of an oncoming recession, and the best asset class to own during a recession has been U.S. Treasuries.

Remember: at these low yield levels, U.S. Treasuries are assets you want to rent, not own. The long-term real return potential is barely positive, so holding these to maturity is not a solid long-term investment. That said, if we do enter an economic downturn, treasuries exhibit a negative correlation to most other asset classes which greatly reduces portfolio volatility and limits downside risk. Considering how late we are in the current cycle, it becomes even more critical to hold assets like this (particularly after a steep selloff when sentiment is extremely negative). Therefore, we think it’s wise to rely on the opinion of people like Lacy Hunt and, for now, to ignore the former Bond King who has once again cried wolf.

Jeff Dicks, CFA

Portfolio Director

To contact Jeff, email:

jdicks@evergreengavekal.com

As an ardent skeptic, I’ve yet to passionately fight for any political candidate. I’m not in perfect alignment with either major U.S. political party and I certainly see flaws in most candidates. I have issues that are important to me and I vote for those who I believe will champion them. Yet, ultimately, I believe that the power of any individual, including the President of the United States, is limited by the checks and balances of the Constitution.

Due to my general apathy for most Presidential candidates, I’m fascinated by the passionate reactions that inevitably follow most elections. Beyond the victory tours and rallies, markets typically experience some short-term volatility, but eventually refocus on other events. In fact, legendary investor and Democrat, Warren Buffett, has repeatedly advised against making investment decisions based on who’s in the White House. Therefore, as you can imagine, the 13% rally in the S&P 500, affectionately known as the “Trump Bump”, has my attention and full skepticism.

Throughout 2016, it was common to hear proclamations that Trump was the better candidate because he was a successful businessman who could surely revitalize an anemic U.S. economy. As markets stabilized and rallied post-election, the details of Trump’s market-friendly agenda and Wall Street-laden team continued to throw fuel on the markets’ fire. However, up until this past week, the 13% appreciation in the S&P 500 was primarily based on the hope of future action rather than concrete changes.

Accompanied by his self-professed skills at creating new jobs, Trump believes a 3% GDP growth rate is achievable if his policies are enacted. Post-election, industrial companies appreciated following the President’s promise to rebuild crumbling infrastructure in the United States. Financials rallied due to the belief that lower taxes and fewer regulations were coming. Surveys-based indexes, such as the Institute of Supply Management (ISM) and Consumer Confidence, echo the markets’ optimism for potential growth.

The Trump administration has generated its fair share of negative headline-worthy news, but thus far markets have remained unfazed. Now, as the administration completes its second month in the White House, we’re starting to get a clear picture of which agenda items are on top of the priority list. Along with immigration reform, repealing and replacing the Affordable Care Act is clearly a top priority. Markets view this favorably due to the belief that the bill has acted as a governor on economic growth for the past 7 years.

On March 6th, Wisconsin Congressman Paul Ryan released the first details of the House of Representatives’ new healthcare plan. In the two weeks following the announcement, many members of the Republican party voiced displeasure with the bill. Dissenting House Republicans believe the new plan remains too costly for the Federal Government. Conversely, several members of the more centrist Republican Senate have expressed displeasure with the bill, viewing the cuts as too harsh on poor and elderly communities. In what appeared to be an admission that repealing and replacing the ACA may be more time-consuming than originally thought, President Trump recently commented on the surprising complexity of our healthcare system. Until this week, the market appeared to have faith that Congress would ultimately agree to a replacement and move on to the next agenda item. However, Tuesday’s market decline was the first sign that faith in this administration’s ability to negotiate a bill through Congress is wavering.

For now, tax reform and infrastructure packages appear to be shelved until cost savings from a repealed Affordable Care Act are identified. Recently, Treasury Secretary Steve Mnuchin went as far to say that August might be the appropriate time to address tax reform. Subsequently, on Friday of last week, President Trump released his first budget proposal as President. While unlikely to be enacted by Congress, it does offer insight into the President’s desired path for the year ahead. Discretionary spending remained flat year-over-year and a surge in deficit spending appears to be of no interest to this administration. In fact, in her recent press conference, Federal Reserve Chairwoman Janet Yellen echoed my skepticism when she stated, “If we were to see a major shift in spending reflecting those expectations, that could very well affect the outlook. I’m not seeing it at this point.”

If Congress is unable to agree on a replacement for the Affordable Care Act, based on recent history in Washington, it’s easy to imagine gridlock eliminating any hope of tax reform and expansive infrastructure programs. Further, even if Congress can pass a new healthcare bill, the battle between austerity and deficit spending is likely to intensify.

Regardless of whether these market-friendly agenda items are addressed, other factors could ultimately side-swipe equity investors buying the “Trump Bump.” In fact, despite abnormally warm weather this winter (which normally supports consumer-spending trends), the Atlanta’s Federal Reserve forecast for first-quarter GDP has declined from over 3% at the start of the year to below 1% today. While lackluster growth is old-hat to the second longest bull market since the Great Depression, the Fed raising interest rates in consecutive quarters is certainly new. The Federal Reserve Board believes that it will raise interest rates twice more this year, putting pressure on the lofty valuations equities have enjoyed due to the lowest interest rates in US history. While we admit that equities can ignore this change early in a tightening process, it’s important to recognize the shifting environment that has supported this rally for the last 7 years.

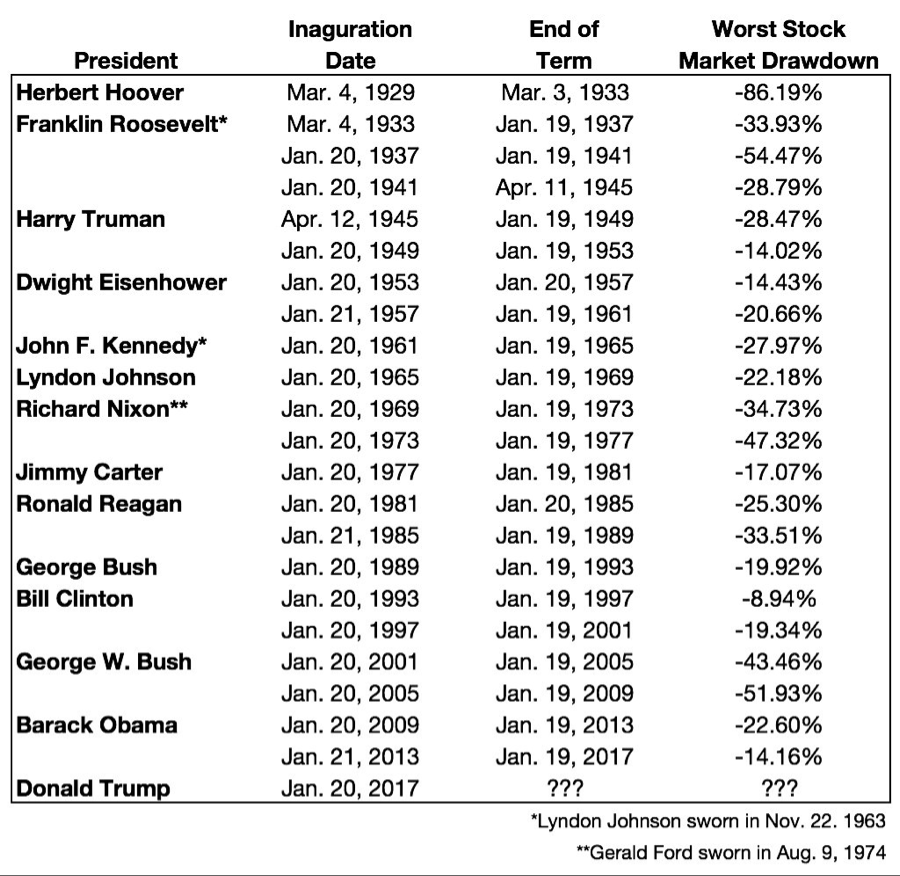

If you’re buying the “Trump Bump” today, hope needs to quickly turn into definitive policy change. Otherwise, the decline seen on Tuesday may just be the start of the "Trump Slump." As shown below, it’s not uncommon for a first-term President to experience a significant decline in the markets. If Trump disappoints as a legislator, and the markets shift focus to valuations and interest rates, I fear his market drawdown could be dramatic.

Jeff Eulberg, J.D., CFP®

Director of Wealth Management

To contact Jeff, email:

jeulberg@evergreengavekal.com

Recently, robo-advisors have exploded in popularity, emerging as one of the fastest-growing sources for financial advice. According to Investopedia, “A robo-advisor is an online wealth management service that provides automated, algorithm-based portfolio management advice without the use of human financial planners.” It seems like every week there’s a new article announcing another bank or firm that’s joined the party by launching a robo-advisor. Goldman Sachs, JPM, Charles Schwab—my inbox is bombarded with articles from industry publications warning me of the dangers they present to wealth managers. They have titles like “Are You Ready to Lose Your Job to an Algorithm?”, “How to Avoid Being Outsmarted by the Machines,” and “Wealth Management, Under Attack by Robots!” Given all the hype these new financial services are receiving, I thought I’d use this week’s “common misconception” theme to share my perspective on the matter.

In a strange way, the wealth management/financial services industry helped create the robo-advisor, though not directly through capital investments or creative innovation. In fact, it was quite the opposite. Many inefficiencies in the financial world created a vacuum for robos to fill. As technology continued to progress, it evolved and expanded the way investors chose to interact with their advisor. Five years ago, it wasn’t possible to open an account digitally. Today, it’s becoming increasingly commonplace. New investment vehicles, such as ETFs, have gained increased momentum, making investing seem both easier and safer. Additionally, markets themselves have played a key role. In particular, the lack of volatility has had an obscuring effect on all managers. As Warren Buffett says: “Only when the tide goes out do you discover who’s been swimming naked.”

Somewhere around 2010, robo-advisors truly began to gain traction. They burst onto the scene and offered enhancements that were long overdue. For starters, they eliminated something everyone hates: paperwork. Our industry is still behind the curve in this respect. Some firms have begun moving away from FedEx packages filled with paperwork and countless “sign here” stickers. Others (especially larger companies bogged down with corporate red tape), are slower to adapt. In the case of, emerging robo-advisors, they did something that’s considered heresy in the financial world—they simplified things.

Instead of using countless acronyms, big words, and confusing charts, robo-advisors made the experience for investors simple and intuitive. Another important differentiator they offered was a willingness to take on small accounts and charge low fees. On average, robos tend to charge around 0.30%, which is a sizeable discount from traditional advisors who typically offer management fees of 1% or more. Robos, which offer tech-savvy websites allowing small investors to easily access financial markets, are particularly popular with younger investors. Combine this with the pre-installed disdain millennials carry for Wall Street (or anyone wearing a suit) and it’s no wonder robos are “trending.”

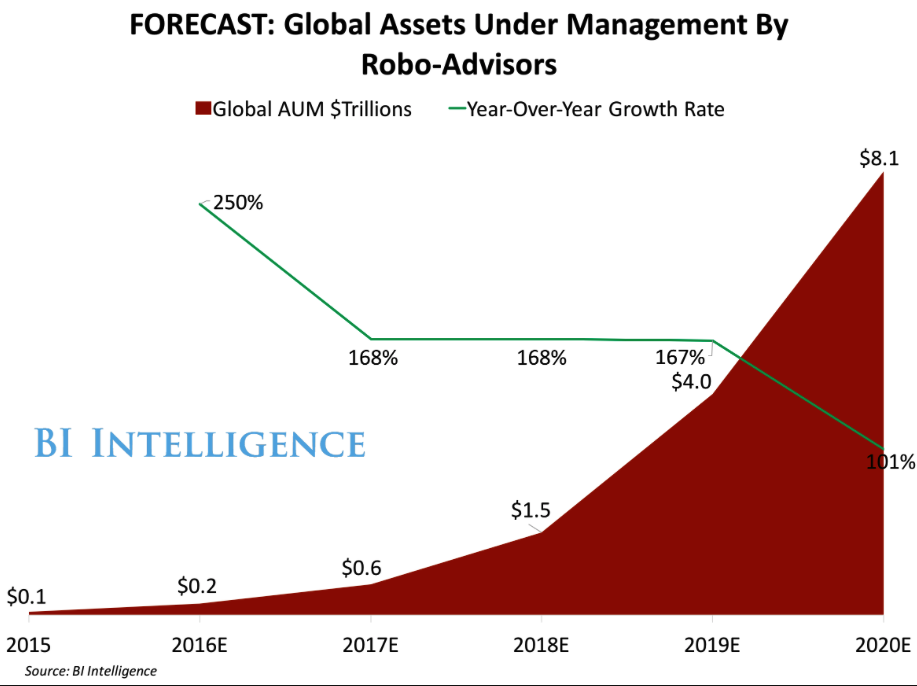

Source: BI Intelligence

As shown in the chart above, it’s estimated that robo-advisors will go from managing hundreds of billions of dollars today, to over $8 trillion in a span of four years. For perspective, total global Assets Under Management is currently $72 trillion. That means in four years robos are projected to soar from being a blip on the radar to capturing more than 10% of worldwide market share. The above prediction is far from an outlier, and if you’re not sold on BI Intelligence as a source, try this: Deloitte, a leading name in consulting, audit, tax, and advisory services, estimates that, by 2025, one quarter of all money invested in the U.S. financial markets will be done without a human advisor. To say that robo-advisors are taking the industry by storm is an understatement. If you believe what people are saying, it’s more of a foregone conclusion. Anecdotally, it’s easily the most talked about subject at every wealth management conference I attend. There’s a level of hysteria; “the robots are coming!” It reminds me of the quote that runs throughout the thrilling HBO series Game of Thrones: “Winter is coming.”

If conventional wisdom sees the rise of the robo-advisor as a foregone conclusion, I suppose it’s time to offer a rebuttal. I’ll try to avoid being ambiguous or elusive in my reaction to this accepted conventional wisdom: Bull! In fact, I’d like to point out that this is a firm-wide response to many widely-accepted consensus beliefs (hence the spirit of this week’s edition). We believe that this mindset is at the heart of what makes us sound investors.

Here’s my response to both the investor who thinks that the robo-advisor is their investing salvation and to the investment advisor who thinks their tombstone has already been carved. Using legendary ESPN college football broadcaster Lee Corso’s words: “Not so fast, my friend.”

As stated earlier, the inefficiencies and slow adaptation of the financial world made room for the birth of a new industry where finance and technology collide. Commonly referred to as FinTech, this is the overarching industry under which robos fall. The mission of a robo is to simplify and reduce the cost of investing. They’ve succeeded on that front. However, simplicity and low cost doesn’t translate into success for investors. The fact that they’ve made investing simple for the end investor says nothing about the rate of return for clients.

The beauty of technology is that it’s creatively disruptive. Innovators have already begun to defect to the archaic world of finance, helping modernize firms who want to keep pace. These entrepreneurs are taking all the great technology breakthroughs conceived in the robo world and making them available to firms willing to adapt. But, as technological breakthroughs made in the robo world bleed into the traditional financial space, the distinction between robo and traditional—from a client-experience perspective—will converge. Once this occurs, the differentiation will go back to actual investments themselves. If you have a choice between one car that’s sleek and stylish but is very slow and another that is fast but ugly and out of date, that could be a tough decision for some. If both cars are sleek and stylish, who would ever pick the slow car? To this point, robos have delivered far better user experiences than traditional wealth managers, but the pendulum is starting to swing back in the other direction.

Speaking of investments—what a world we are living in! If you’ve owned U.S. stocks for the past eight years, it’s been a wonderful ride—a smooth ascent with record low volatility. A monkey throwing darts at a wall of stocks would have done great over this period. Most, if not all, robo clients have never seen a real bear market. Sure, low fees and simple interfaces are appealing, but what happens when you want someone to talk to about what’s going wrong? Some robos have started hiring CFPs and developing human call centers. The idea that these folks sitting at the end of an 800 number can calm the fears of a frightened client during the next bear market, whom they’ve likely never met, seems a tad optimistic.

When it comes to portfolio management, most robos only offer the most basic techniques. One reason for this is they can keep costs low and simply rebalance an investor’s portfolio to its target weight on a predetermined schedule. There is no thought involved, which begs the question, why are they receiving a fee at all? In many cases, it should be called a rebalancing fee, not an investment management fee. Further, many robos do not account for tax considerations. Partially, it’s because their low-cost model doesn’t allow for more complicated tasks, but also because they don’t know the entirety of your financial picture. This is where simplicity can turn from a wonderful to a not-so-wonderful thing. The burden is on the client of a robo to know what to do when their financial picture changes. For example, if you sell your family business for a sizeable gain and happen to have losses in your investment portfolio (which you could use to offset your tax liability), how will a robo-advisor know to take this step?

In summary, while creative disruption is forcing uncomfortable change for many within the investment industry, it’s a huge win for investors. For wealth managers who are skilled investors but lacking on the technological front, this will require a commitment of time and money to remain competitive. Robo-advisors who are under-equipped from an investment standpoint must find more sophisticated ways to manage their client assets. Both are already happening. Today, wealth management and robo advisors aren’t competing, they are converging.

One question remains: When the next bear market arrives and investors start to panic, can robots answer the call?

Tyler Hay, MBA

Chief Executive Officer

To contact Tyler, email:

thay@evergreengavekal.com

Cast your vote for whomever makes the most compelling case.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.