"You can never say never, but I cannot imagine a convincing argument for further quantitative easing after this round, given what is developing now in the economy."

-Dallas Fed Chief RICHARD FISHER

POINTS TO PONDER

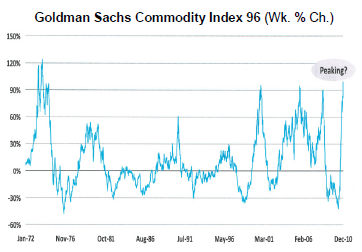

1. The battle against inflation in emerging markets continues to escalate, largely driven by soaring commodity costs. The combination of rising interest rates in developing nations and exceedingly extended commodity prices could lead to a plunge in the latter.

2. Increased tightening measures by central banks in emerging countries have caused spreading weakness in their stock markets. With the S&P 500 up another 5% this year, US share prices are now ahead 20% since the beginning of 2010 versus a rise of 16% for emerging markets.

3. Once the world’s leader in the production of TVs, stereos, cameras, and other related devices, Japan has just become a net importer of consumer electronics. As noted by the Financial Times, this has ominous implications for its balance of trade.

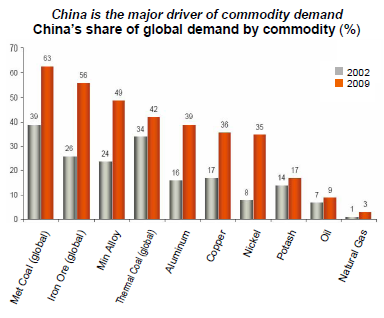

4. Rating agency Fitch has estimated that if Chinese economic growth were to decelerate from its current 10% to 5%, commodity prices could fall by 20%. Given China’s extreme influence on the demand for many key raw materials, this conclusion seems plausible.

5. Popular newsletter writer John Mauldin recently quoted a factoid from Newt Gingrich underscoring waste in government healthcare. Mr. Gingrich noted the contrast between fraud in American Express’ medical plan of just 0.3% versus 13% in Medicare’s, largely due to the AMEX system being far more automated.

6. Massachusetts’ experience with healthcare reform is a cautionary tale for the country as a whole. Prior to its passage, health insurance premiums in the state were rising 3.7% per year less the national average. Since it was signed into law, premiums have been increasing at an annual rate that is 5.8% above the average of the rest of the US.

7. Although US Treasury interest rates have been rising of late, the causes are likely tied to improving growth prospects and concerns over commodity-driven inflation rather than liquidation by foreign investors. The much feared rout of Treasuries once China halted its buying program has turned out to be a non-event.

8. Adm. Mike Mullen, chairman of the Joint Chiefs of Staff, has recently stated that exploding government debt is our number one security threat. His worries are understandable considering that our nation is 245 years old and our overall indebtedness has risen by one-third in just the last three years.

9. One of the more unusual aspects of last year’s 15% total return (appreciation plus dividends) for the S&P 500 was

that 94% of the gain occurred on the first trading day of each month.

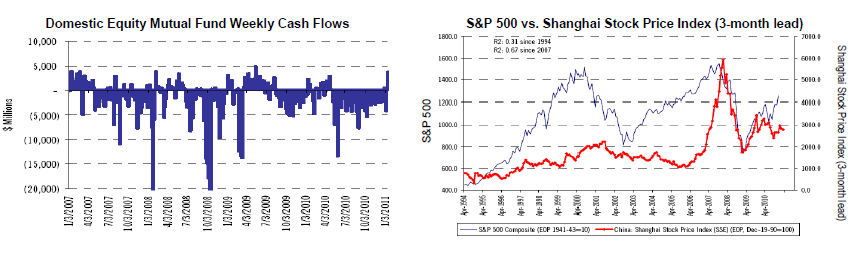

10. US mutual fund investors are finally beginning to feel better about domestic stocks. Their timing, however, could

be less than ideal due to the overbought status of the market as well as the correlation between Chinese and US share

prices. The Shanghai exchange has tended to lead by three months and lately has entered bear market status.

11. Bjorn Lomborg, acclaimed author of The Skeptical Environmentalist, pointed out in the January 22, 2011, issue of

the Wall Street Journal that London’s air quality is now better than it has been at any time since 1585.

11. Bjorn Lomborg, acclaimed author of The Skeptical Environmentalist, pointed out in the January 22, 2011, issue of

the Wall Street Journal that London’s air quality is now better than it has been at any time since 1585.

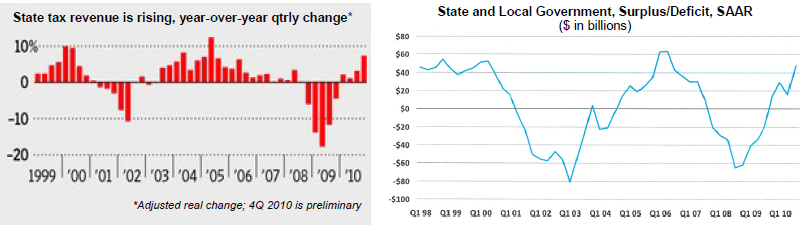

12. In the wake of Meredith Whitney’s ominous comments about the tax-free bond market, a growing chorus of experts has rallied to its defense. Yet municipalities are not helping their cause given that 40% of issuers were at least three years behind in filing financial statements as of 2009.

13. On the positive side for munis, tax revenues are definitely on the mend. Additionally, municipal budgets are increasingly

in surplus status despite gaping deficits among some of the largest states.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.