"Given relative valuations, wouldn’t it be wiser to play the US consumer by buying European or Asian exporters than to overweight US equities today?"

- Louis Gave

Spicing things up. We all know the old saying that variety is the spice of life. Accordingly, in this week’s EVA, we are definitely doing a variation on our usual theme of a full length written issue by providing our readers with a spicy Asian video. No, not that kind! (This Fifty Shades of Grey stuff is getting way out of hand!!) I’m referring to a video interview with close friend and partner, Louis Gave, on the investment attraction of Asia.

Bloomberg has referred to Louis as one of the smartest men in Asia. Considering how many males there are in Asia that’s quite a compliment! After you listen to his thoughts on why Asian markets may finally begin to outperform the Energizer Bunny known as the S&P 500, I think you will agree Bloomberg was not waxing hyperbolic.

In full and fair disclosure, Louis is not just making a persuasive case for Asian markets in general but also for the GaveKal Evergreen Asian Opportunities fund which our two firms started in August of 2013. As Louis indicates, this new vehicle is structured in a highly similar fashion to GaveKal’s existing Asian fund for European investors (known as a “UCITS”) that incepted nearly 10 years ago. (Additional details can be furnished upon request via the fund’s prospectus.)

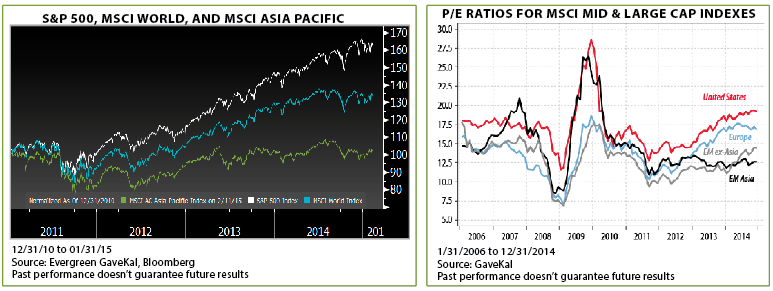

While I’ll let Louis make the case for the fund, I do want to make a few comments on Asian markets overall. As you can see from the chart below (left), they have lagged even the global indexes in recent years and those have, in turn, badly trailed the US market.

This is particularly ironic since Asian markets, especially the emerging variety, were widely assumed to have far better growth potential than the S&P 500 back in 2010 and 2011. Long-time readers may recall our skepticism of the conventional “wisdom” at the time. But, after years of underperformance, valuations are now among the cheapest in the world and far below that of the US.

Encouragingly, even with the US dollar on a rampage versus almost every other global monetary unit over the last six months, Asian currencies have held up considerably better in most cases. As Louis has recently written:

“Amid the turmoil, Asian currencies have been islands of relative stability. In the last three months the Philippine peso has risen by +1.3% against the US dollar. The Indian rupee and Thai baht are flat. The renminbi (China’s currency) and the Taiwan dollar are down -2.5%. Even the Japanese yen—every macro investor’s favorite short after the Bank of Japan’s October surprise—is down only -8%, and has basically been flat since mid-November.

The stability of Asia’s currencies makes the region all the more attractive both for domestic and foreign investors. Meanwhile, the greater currency volatility in Europe and other emerging markets massively increases the risk, and stress, for investors looking to deploy capital in either. At the margin, Asia’s currency stability should thus lead to a re-rating (i.e., improved valuation) of regional equities and bonds, relative to European and US equities. In fact, given the relative stability of Asian currencies and the region’s generally positive economic outlook, it makes little sense that Asian equities should currently be sporting the lowest P/E ratios in the world.”

In the interview, Louis also makes the crucial point that yields in Asia, particularly from dividends, are much higher than most of the rest of the world. Naturally, this is music to my ears as I continue to worry most investors are not grasping how deleterious it is that interest rates in the developed world have gone the way of the dodo bird. This is particularly a threat for all those needing cash flow on which to live. Given our rapidly aging society, this stunning yield extinction has the potential to escalate into an investment crisis of the first order. If you think I’m exaggerating, please realize that 16% of the world’s sovereign bond markets now have negative interest rates.)

Now, let’s listen to one of Asia’s keenest minds has to say…

Click here to watch the video.

DEFINITIONS AND DISCLOSURES

S&P 500: The S&P 500 is an index designed to gauge large cap U.S. equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. Investors cannot invest directly in an index.

P/E ratio: A company’s share price compared to its per-share earnings.

The GKE Asian Opportunities Fund is not suitable for all investors. Subject to investment risks, including possible loss of the principal amount invested. Emerging markets are often less stable politically and economically than developed markets such as the United States and investing in emerging markets involves different and greater risks. There may be less publicly available information about companies in emerging markets. The stock exchanges and brokerage industries of emerging markets do not have the level of government oversight as do those in the United States.

Securities markets of such countries are substantially smaller, less liquid and more volatile than securities markets in the United States.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. Click Here to obtain a prospectus which contains this and other information, or call 855.331.6240. Read the prospectus carefully before investing.

The GKE Asian Opportunities Fund is distributed by ALPS Distributors, Inc., 1290 Broadway, Ste. 1100, Denver, CO 80203.

The sources, opinions and forecasts expressed in this interview, which are subject to change, are as of 11/26/14 and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. The user of this information assumes the entire risk of any use made of the information provided herein.

Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of Evergreen GaveKal or any of its affiliates. Past performance is not indicative of future results. The opinions and forecasts expressed in this video by the speaker do not necessarily reflect those of Evergreen GaveKal or ALPS Distributors, Inc. and may not come to pass.