"There is a big difference between an inflation scare and an inflation cycle and most pundits are underestimating the degree of austerity that is on its way at all levels of government, which will outlast the commodity boomlet."

-DAVID ROSENBURG

POINTS TO PONDER

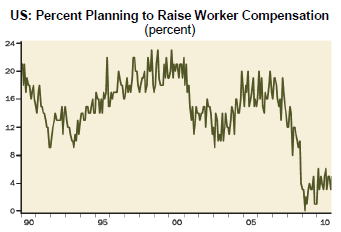

1. With inflation fears running rampant once again, it might be prudent to consider that consumer price increases in the US are primarily driven by labor costs. Based on the outlook for employee wage hikes, it’s difficult to see a lasting surge in the CPI.

2. Excessive slack in labor markets is not just a US phenomenon. According to UBS, global unemployment is at an all-time high, with approximately 27 million more individuals unemployed now than prior to the Great Recession.

3. Although solar continues to be a miniscule portion of overall energy production, global installation of photovoltaic power more than doubled in 2010 to 16 gigawatts. There is now more than 40 gigawatts of world solar capacity, enough to supply about 40 midsize cities.

4. After a stunning surge in both construction and capital spending, propelled by a torrent of liquidity, China’s numerous

tightening measures seem to be cooling investments in these areas. However, while the boom is unquestionably decelerating, the growth rate remains at historically high levels.

5. Germany continues to stand out in an economically challenged Europe. Its unemployment is down to 6.6%, making it one of just two large (G7) countries to have a lower jobless rate today versus 10 years ago.

6. The prestigious investment firm, GMO, has an exemplary track record when it comes to forecasting the future returns of various asset classes. It now sees smaller US companies losing an average of 1.4% annually over the next seven years, net of inflation.

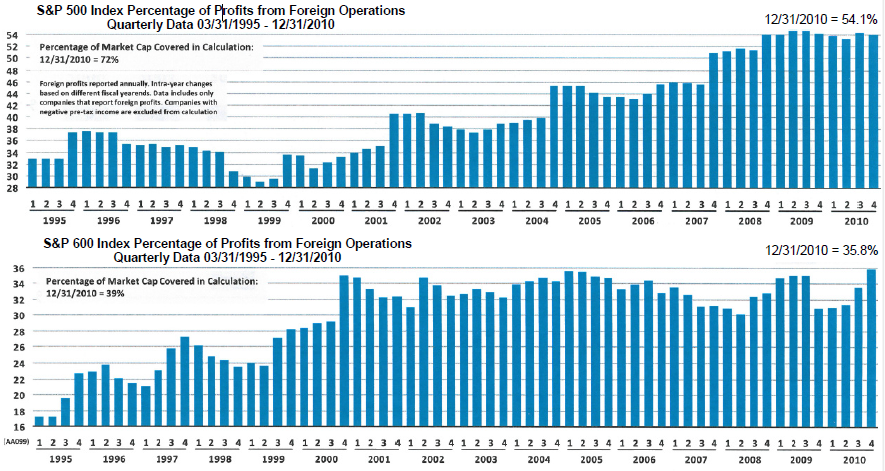

7. A prime reason larger companies, those represented by the S&P 500, might perform better in the years ahead than smaller firms (S&P 600) is the higher percentage of profits derived overseas (54% versus 36%). Moreover, blue chip growth companies, such as Apple, are collectively trading at a P/E ratio of just 14.6, 31% below the 20-year average.

8. In another endorsement of the efficacy of contrarian investing, according to Bloomberg, stocks most favored by Wall Street analysts have risen by 73% since the March 2009 bottom while those least liked by “the Street” have vaulted 165%.

9. Battles are raging in many state legislatures to rein in public-sector benefits. Some have suggested stiffing municipal investors instead; however, the combination of interest and principal payments averages a modest 3% to 7% of state budgets, consistent with historical levels.

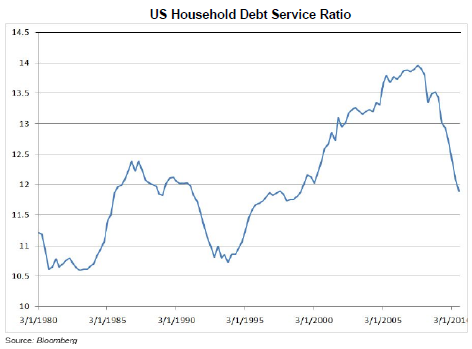

10. Prior EVAs have noted the dramatic improvement in US corporate balance sheets over the last decade. American consumers are moving in the same direction with households having significantly lowered their debt service costs since the housing bubble popped.

11. Brazil is one of the darlings of the emerging world, but it may have a serious credit issue on its hands. Unlike in the US, consumer balance sheets have been deteriorating with debt service costs rising to 24% of disposable income. Despite an inflation rate of roughly 6%, the typical interest rate on consumer loans in Brazil is over 30%.

12. Until emerging markets began to struggle recently, there seemed to be ubiquitous faith that they were no longer tied to the industrialized world. Yet, according to the IMF, linkages between industrial output in developed and developing economies consistently increased from 1979 to 2006 and have become even more correlated recently.

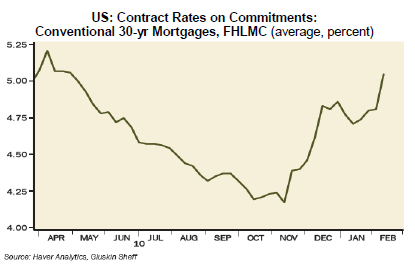

13. The Fed’s quantitative easing program that began last fall was supposed to lower interest rates. The unfortunate reality, however, is that it has caused exactly the opposite outcome for mortgage rates, further pressuring the beleaguered housing industry.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.