“Value relative to growth has never been cheaper, globally.”

- Rob Arnott, chairman and co-founder of Research Affiliates with $170 billion under management and the creator of fundamental indexing.

_____________________________________________________________________________________________________

Last week’s EVA pointed out the considerable damage that has occurred below the placid surface of the US stock market. It also urged taking advantage of the stealth sell-off, particularly with regard to those market segments of a more cyclical nature. These had been especially punished by the Omicron-driven panic selling that began on Black Friday (the day after Thanksgiving) and largely continued through most of last week. At one point, the S&P 500 briefly retreated by 5.2% before the usual buy-the-dip response kicked in.

That EVA also conveyed a fair amount of expert opinion and up-beat news on Omicron. Fortunately, as this week has unfolded, that viewpoint has been mostly validated…for now. When it comes to the ever-mysterious Covid, and its various variants, one can never assume its nasty impacts are totally in the rear view mirror. Yet, thus far, there has been a healthy rebound in virus victim sectors such as energy, restaurants, hotels, airlines, as well as chemical and industrial metals producers, among other economically sensitive areas.

The overarching theme of last week’s EVA, though, was the shocking price declines of a long list of formerly hyper-performing growth stocks. To add another factoid to the story, a few days ago there were 615 issues with a market value of $1 billion or more that had tumbled at least 30% from their 52-week peaks. Most of these reside in the small- and mid-cap categories and many have tanked by 50% and even 70%. This is decidedly odd behavior in what must still be considered to be a full-blown bull market (heavily inflated, of course, by the Fed’s many fabricated trillions.)

This month’s Gavekal EVA, from our prestigious partner firm, is authored by its founder himself, Louis Gave. Because we’ve added quite a few new readers in recent months (thank you for subscribing!), I should provide a brief background on Louis. He co-founded Gavekal Research in the late 1990s in the wake of the Asian Crisis. That event created tremendous damage in asset prices throughout Asia, including a 70% plunge in Hong Kong home prices, the city in which he chose to base his new firm. Thus, it took considerable guts to start a firm focused on emerging investing opportunities in that region during a bear market of epic proportions. Of course, in hindsight, his timing was impeccable.

Starting from a tiny office with two other partners and his dog, Oshkosh, Louis has built an organization of truly global proportions. (The other two founding partners were his father, Charles Gave, and Anatole Kaletsky.) There are now branches around the world, staffed by individuals, and most major investment firms are clients of Gavekal. Louis has been extensively quoted in Barron’s and the Wall Street Journal, as well as numerous other leading financial publications. Further, he is one of the most in-demand speakers at investment conferences around the world. He is also one of my closest personal friends.

As you will soon see, Louis is highlighting the significant chasm that has opened up between the famous FAANGM type names and the formerly white-hot, now ice-cold, small cap growth stocks. Moreover, as senior Gavekal team member Will Denyer pointed out in a related note, the same is true with mid-cap growth stocks versus the mega-cap names such as Apple and Microsoft. This is further evidence of the extreme narrowing of leadership that is occurring in the US equity markets. As I discussed last week, this is a scarlet red flag about the overall market’s health…or lack thereof.

With that as an introduction, let’s see what Louis has to say about this very odd divergence of fortunes…

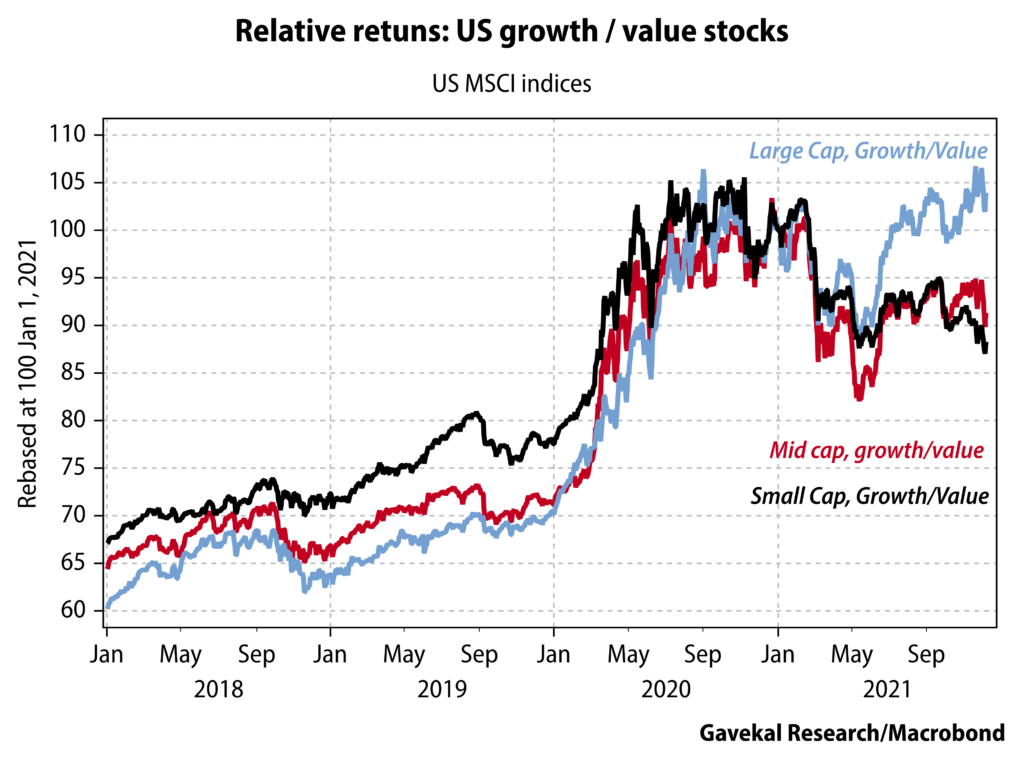

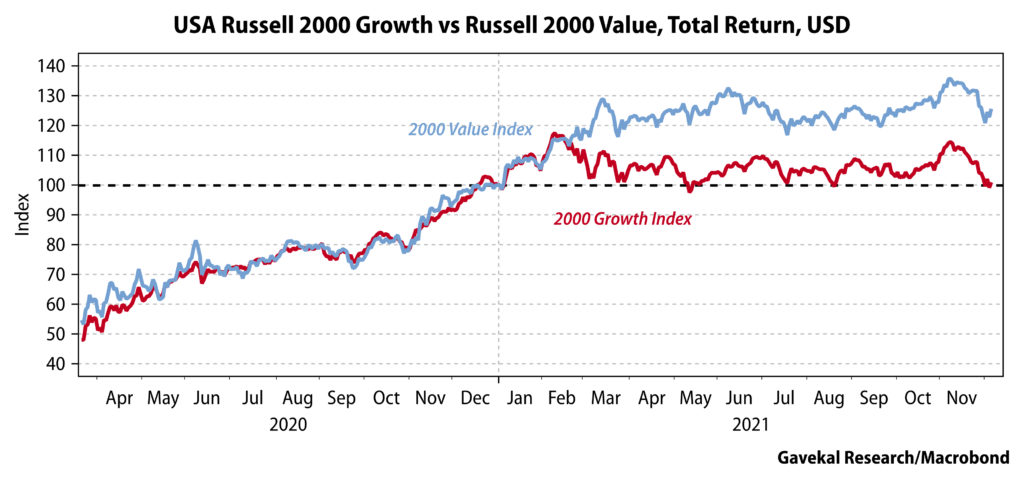

In a recent daily, we pondered the odd outperformance of US growth stocks at a time of upside inflationary surprises. A sharp-eyed client highlighted that the outperformance of growth was highly dependent on which parts of the market one was investing in. After all, our reader pointed out, the Russell 2000 growth index is roughly flat for the year… not much 2021 outperformance there, especially when one considers the +25% gain in the Russell 2000 value index:

Digging deeper, it is clear that while US large-cap growth stocks have done very well, thus grabbing headlines and the popular imagination, the US small cap growth space has had a tough time. In fact, the relative performance divergence between US large-cap growth stocks and US small-cap growth stocks is unprecedented (see middle pane in the chart below).

Zooming in further, it can be seen that after their recent pull-back, US small cap growth stocks have given back about a decade’s worth of outperformance (see lower pane in the chart). The conditions of the last decade—a strong US dollar, low energy prices, low inflation, low interest rates, record retail participation, record foreign inflows and record private equity activity—all favored small-cap US growth stocks. Yet they ended up delivering a similar result to the broader US equity market. These were still very good returns but in an almost “perfect” environment, one might have hoped that the usually high-beta small-cap growth stocks would have outperformed. Worse still, they now seem to be markedly underperforming.

In short, in the past 10 months, it seems that small-cap growth stocks have adapted to a US economy that was growing strongly with accelerating inflation by underperforming both US small-cap value stocks and the broader market. At the same time, US large-cap growth stocks have continued to surge. So what should we make of this parting of ways?

Figuring out which of these options is the right one will offer insights to risks faced by US growth stock investors. Back in 2000, rising short and long rates broke the back of the boom. Today, this does not look like an immediate threat and a bigger concern may be rising energy prices. After all, once they develop a certain momentum, equity bull markets tend to brush off most bad news until they are killed either by higher interest rates, rising energy prices, or a combination of both.

This brings me to a key divergence of opinion within Gavekal. Those, like Anatole, who think that energy prices will not exceed their recent highs conclude that inflation will prove temporary and the bull market will roll on. Those, like me, who think that years of underinvestment in energy has set the world up for a period of rapidly rising energy prices are, for the reasons listed above, more concerned about the viability of the bull market in US large-cap growth stocks. In short, energy bears should probably load up on small-cap US growth stocks, as those will bounce back and catch up with their large-cap brethren; and energy bulls should lighten up on large-cap growth plays.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.