“Revive the A shares, benefit the people; revive the A shares, benefit the people.”

- A required chant from last Sunday’s graduation ceremony at China’s prestigious Tsinghua University, referring to shares that trade on the Shanghai stock exchange.

Ka-put? To kick off this edition of our monthly Guest EVA, I thought I’d share some good news: This is not another nauseating essay about Greece! The more sobering message is that it is about the possible expiration of an extraordinarily market friendly device—the legendary “put”, which has undergirded financial markets in recent years.

Today’s Guest EVA highlights the work of two extremely savvy females on this topic, following up on my theme from last month that women often are more rational when it comes to investing than men. The first note is from our partner firm GaveKal’s Joyce Poon. Over the years, I’ve become a big fan of her consistently well-reasoned insights into Asian markets, particularly China. As you may have noticed, there has been some rather interesting market action in China recently.

Because Joyce’s overview is brief, we have space to include another recent article, one my friend Worth Wray alerted me to, written by Danielle DiMartino Booth. Coincidentally, I’d seen Danielle’s June 17th CNBC interview. It was one of those rare times when I heard a sound bite so intriguing that it caused me to stop what I was doing and turn up the volume. (For all of you who missed it, here is the link.)

Danielle worked for the Dallas Fed’s president Richard Fisher from September 2006 to June 2015. Like Mr. Fisher, she has been most uncomfortable with the Federal Open Market Committee’s constant effort to drive up financial asset prices without regard for the ultimate consequences—not to mention the questionable benefits to the real economy. As she points out, this policy was an extension of the so-called “Greenspan Put” that came into existence after the crash of 1987. Over the years, it morphed into the “Bernanke Put” and then the “Yellen Put”.

The idea of a put in this sense comes from the options market where a put contract provides downside protection for the buyer. The beauty of the Fed Put is that it doesn’t require an investor to spend any money to buy the protection. Who said there is no such thing as a free lunch? Well, in case you think Milton Friedman was wrong when he uttered that famous phrase, time has proven there is a most definite cost. Which leads me to China and Joyce’s aptly titled missive “The Xi Jinping Put”.

Xi Jinping is the General Secretary of the Chinese Communist Party (i.e., China’s head honcho), and he’s turning that country upside down and inside out. While he hasn’t resorted to executing political opponents with anti-aircraft cannons, as his beholden and deranged counterpart in North Korea has done, he definitely has an insatiable urge to purge.

He’s also proven quite the stock promoter, going out of his way to encourage his subjects fellow citizens to play the market, including on margin. As the more speculative markets of Shanghai and Shenzhen went postal, rising 150% and 200% respectively in less than a year, this surge served as a welcome off-set to the declining real estate market and the generally cooling economy. Thus, Mr. Xi has one-upped the Fed, the ECB, and the Bank of Japan in creating a “wealth effect”—until recently, that is.

At one point this week, the Shanghai market was down over 30% while the Shenzen index briefly touched minus 40%, compared to their highs hit in mid-June. This stunning fall from grace has caused media commentators to utter the dreaded “C” word—as in, crash. Remarkably, it has occurred despite the implementation of a long list of aggressive support measures, including a prohibition against insider stock sales. Yesterday, the Chinese government went so far as to order its citizens to buy stock. In other words, there’s little doubt this has been the most egregious government put in the history of the financial markets.

Whether it’s Greece, European bond yields, or Chinese stocks, there’s an unmistakable trend toward governments and their monetary lackeys, the central banks, losing control of the situation. Don’t expect them to give up without one whale of a fight, however.

While Joyce clearly has concerns about how effective the Xi Jinping’s put will be, she believes China’s bull market is wounded, but not mortally. In our view, the Hong Kong stock market, which was not caught up in the speculative mania and yet was slammed by 20% at one point this week, is a far safer way to play a continuation of China’s up-cycle. The Hong Kong market has trailed the S&P 500 by over 20% since the former bottomed in late 2008. And at less than 11 times earnings and a modest premium to book value, we don’t believe investors will be put out as severely if the Jinping put expires prematurely.

THE XI JINPING PUT

Joyce Poon

Over the weekend the Chinese government rushed out an unprecedented grab-bag of measures intended to support the free-falling A-share market, which by Friday’s close had tumbled 29% from its mid-June high. By deploying almost every weapon in their armory, the authorities managed to arrest the market’s slide, at least in the immediate short term. By the close of trading on Monday, the Shanghai market was up 2.4% from Friday’s close. But there is a deep contradiction inherent in Beijing’s efforts to prop up stock prices. In the near term, the government finds itself forced to manipulate the market in order to restore investors’ confidence. In the longer term, however, official operations to support share prices run counter to the idea that Beijing needs a robust and deep stock market to help resolve existing market distortions and to facilitate its broader policy of economic liberalization. This is a contradiction that Beijing may find hard to reconcile.

Reviewing the steps the authorities have taken in the last three weeks to bolster sentiment, there can be little doubt about the importance the central government attaches to putting a floor under the stock market. Following the central bank’s moves a week before to cut interest rates and inject liquidity into China’s financial system by reducing bank reserve requirement ratios, this weekend regulators and leading market participants announced a suite of administrative and price-keeping measures designed to halt the slide in prices.

-The State Council ordered an indefinite suspension of new share issues, which should halt further dilution and free investor funds that would otherwise have been locked up ahead of initial public offerings.

-The China Securities Regulatory Commission said that the capital of the China Securities Finance Company, a state body which extends margin financing to brokers, would be increased fourfold to RMB100bn, and pledged that the People’s Bank of China would inject liquidity into the lender in order to support the market.

-Central Huijin, a powerful state investment fund, said it was buying index-tracking ETFs.

-A score of China’s leading brokerage companies said they will set up a RMB120bn fund to buy stocks, also pledging they will not sell stocks on their own account while the Shanghai Composite index remains below the 4,500 level. At Monday’s close it was at 3,776.

-Nearly 100 fund management companies promised to buy stocks to support the market.

In addition, last week the authorities announced a crack-down on short sales and said the national pension fund would be permitted to buy equities.

Although similar measures have been employed at different times in the past, the simultaneous roll-out of such a broad range of initiatives emphasizes the political store China’s leaders set by a buoyant stock market. Indeed, rising equity prices are an important component of President Xi Jinping’s “China Dream” of turning his country into an acknowledged global economic super-power over the coming decades.

-A sustained bull market would cushion the adverse impact of China’s continuing downshift to a slower growth trajectory, potentially generating a wealth effect which would boost consumption.

-Rising stock prices would encourage private investment and make it easier for Chinese companies to raise equity capital, reducing China Inc’s reliance on bank lending and hopefully increasing the efficiency of capital allocation (see The Pros And Cons Of A Bull Market).

-By the same token, a robust stock market would ease the privatization of state assets, smoothing China’s transition to a more productive economy, governed more by market forces than official diktat (see [China] Chinese Equities And The Taiwan Syndrome).

Perhaps more to the point, having engineered the bull market of the last year by ensuring plentiful liquidity and encouraging the growth of margin finance, as well as through repeated exhortations to buy, the government is now anxious to preserve its own credibility among China’s millions of retail investors by averting a crash—hence the barrage of supportive measures launched over the last couple of weeks.

This places the authorities at a reform crossroads. By manipulating the market Beijing is offering investors a “Xi Jinping Put”, which is likely to lead to a major rebound in equity prices over the next six to nine months, of which China’s banks are likely to be the main beneficiaries (see A Bear Market, Or A Rotation?). If the authorities now react to the volatility of recent weeks as a wake-up call alerting them to the vulnerabilities built in to the current system, and accelerate their economic and financial liberalization program, the weekend’s intervention will go down in history as a smart move. Conversely, if they fail to take advantage of this window of opportunity, China’s leaders will have painted themselves into a corner in which they will remain dependent on continued micro-management of the stock market to shore up sentiment; a situation which would undermine their own aim of creating a liberalized financial system with robust—and largely independent—institutions, and an economy in which market forces play a more dominant role. Our belief is that the former remains the more likely course, in which case there are good reasons to expect that in five years time, China’s stock market will be considerably higher than today (see The New Way To Think About China and Chinese Equity Demand And The Acceleration Phenomenon).

In the shorter term, the Xi Jinping put should mean that the market risk is skewed towards the upside for the next six to 12 months. Beyond that, much depends on Beijing’s appetite for substantive reforms. The clock is ticking.

RATIONAL EXUBERANCE?

Danielle DiMartino Booth

“The mob will now and then see things in a right light.”

- Horace

If one dares make mention of overvaluation in the U.S. equity market, the derision incited takes one back in time to angry Roman mobs. Is it not plain, the masses shriek, based on a traditional price-to-earnings (P/E) ratio, that stocks are valued just a hair above their long-term average? Indeed, if you look back over the last 12 months of reported earnings, the current P/E of 20 is not alarmingly above its long-term average of 15. And that’s that.

But is that, that simple? At nearly 76 months, the current rally in stocks is surpassed in length by only two other stretches since 1932—the 86-month run that ended in 1956 and the extraordinary 113-month era that culminated with the bursting of the Nasdaq bubble. Shouldn’t the current stock market rally prompt a rational investor to at least ask what underlying factors are driving the persistent trend? There’s no post-war economic surge that promises to produce the next Baby Boomer generation. Nor has a technology emerged that begins to compete with the advent of the World Wide Web. The shale revolution aside, the current rally has not been catalyzed by anything that appears set to alter the course of history.

Of course, stocks could have been so undervalued in March 2009 that they were simply poised to rise after a brutal and prolonged slump. The problem with this line of thinking is that history suggests otherwise. Stan Nabi, now the Chief Strategist “Emeritus” at Silvercrest, once told a group of wet-behind-the-ears MBAs in training that there was one rule that never failed to deliver when it came to valuing stocks. Way back in 1996, when Greenspan was angsting about “irrational exuberance” and Nabi was still at Donaldson, Lufkin & Jenrette, Nabi said, “Stocks never emerge from a bear market until the Standard & Poor’s 500 is trading at a single-digit P/E multiple.”

There was little doubt in our minds as to Nabi’s credentials. He’d had the good fortune to study at Columbia University under the tutelage of Benjamin Graham, the father of value investing. It didn’t hurt that he’d attended Graham’s class with a young student named Warren Buffet. Suffice it to say, a long vigil began that day for one very impressionable market watcher for whom the wait has yet to end. The closest the market got to a single-digit P/E breach occurred in March 2009, when the S&P 500 troughed at the ominous level of 666, taking the P/E down to its most recent low of 13.3.

As for the true secular bottoms, ones that laid the groundwork for secular bull markets, the years 1921, 1931, 1942 and 1982 featured bear market troughs, when the P/E ratio did skid to a single digit. In some of these cases, P/Es languished below 10 for prolonged periods prompting investors to cry “Uncle!” and abandon the despised asset class once and for all.

While there’s no doubt stocks had put deep fears into investors’ hearts by early 2009, they were nevertheless not the screaming bargain history suggested they could be. Maybe it was good enough that there was a gaping distance between 13.3 and 1929’s 32.6 to say nothing of December 1999’s record high of 44. Maybe, but that reasoning just didn’t sit right with this market historian, especially from my perch within the halls of the Federal Reserve.

It’s undisputed that the financial crisis, sparked by the subprime mortgage conflagration, was the worst since the Great Depression. Why then, did stocks not react in kind, bleeding out until they too were trading at a single-digit P/E, as they were in 1931? Could it be that interest rates, which had been slammed down to the zero bound three months prior, had a hand in halting history in its steps?

Few Fed insiders would deny that extraordinary measures undertaken in the heat of the financial crisis put a floor under asset prices of all kinds, including stocks, though such aims could never be uttered publicly by policymakers. Except for the fact that they were, on October 20, 1987 in a statement released by Alan Greenspan’s tightly-run Fed: “The Federal Reserve, consistent with its responsibilities as the nation’s central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.”

The Fed intervened in the markets that very day, bringing the fed funds rate down by a half-percentage point to just under seven percent. The stock market responded in kind, rallying as if on cue. Throughout the course of the next few months, the Fed repeatedly took overnight interest rates lower. Sometimes, as an added bonus, the central bank would go so far as to give trading desks advance notice. How awesome was that, traders must have thought, the ability to position to profit before the fact?

Nobel Prize winner Robert Shiller has devised a twist of sorts on the traditional P/E ratio by comparing stock prices to the average inflation-adjusted earnings from the previous 10 years. The thinking behind this construct is corporate earnings can be affected by the bumps in the business cycle, which can render the traditional P/E ratio highly volatile. Smoothing out volatility to make any indicator less noisy and therefore more efficacious is intuitive enough. And yet, the Shiller ratio has become a target of stock market cheerleaders, many of whom have made a professional sport out of debunking his methodology. (Shiller’s measure suggests a higher current level of overvaluation than the more malleable, shorter-term P/E does, so what’s to like?)

To his credit, legendary investor Jeremy Grantham has not succumbed to attacking Shiller. Rather, he recently made an elegant observation with regard to the good professor’s full historic data set: The Shiller P/E averaged 14.0 times earnings from 1900 to July 1987; in the period that followed Greenspan’s taking the helm to present day, the Shiller P/E has averaged 24.4.

In other words, some element appears to have entered investors’ calculus that justifies paying prices that are markedly higher than they were before Black Monday, before Greenspan committed to provide liquidity to support the financial system. Years ago, investors even came up with a nickname to describe the effective floor placed under all risky asset prices since the Fed began making policy with an aim to mitigate losses: the “Greenspan Put.”

A put is a contract that allows the owner to profit if the price of an underlying security declines. If you own a put contract on the broad stock market, you make money as the stock market declines. To be sure, investors have changed with the times when it comes to the identity of the put’s benefactor. The current put is ever so originally called the “Yellen Put,” which replaced, of course, the “Bernanke Put.”

So which history should investors reference to judge the current value of the stock market -- the pre-Greenspan era or that which followed? The former casts the current Shiller P/E of 27 as frothy, if not rich; the latter suggests investors are perfectly rational in their exuberance. After all, stocks are not nearly as overvalued today as they were in 1999. And more to the point, policymakers remain loathe to end an era, regardless of the damage it has wrought on the notion of price discovery.

The catch is that a put, as is the case with any contract, is not designed to be in effect in perpetuity. Then the question becomes, what happens if history eventually catches up with stocks, ultimately pushing valuations into single-digit P/E territory? In that event, investors would rightly conclude that interventionist policymaking, while well-intentioned in name, was nevertheless destructive in the end.

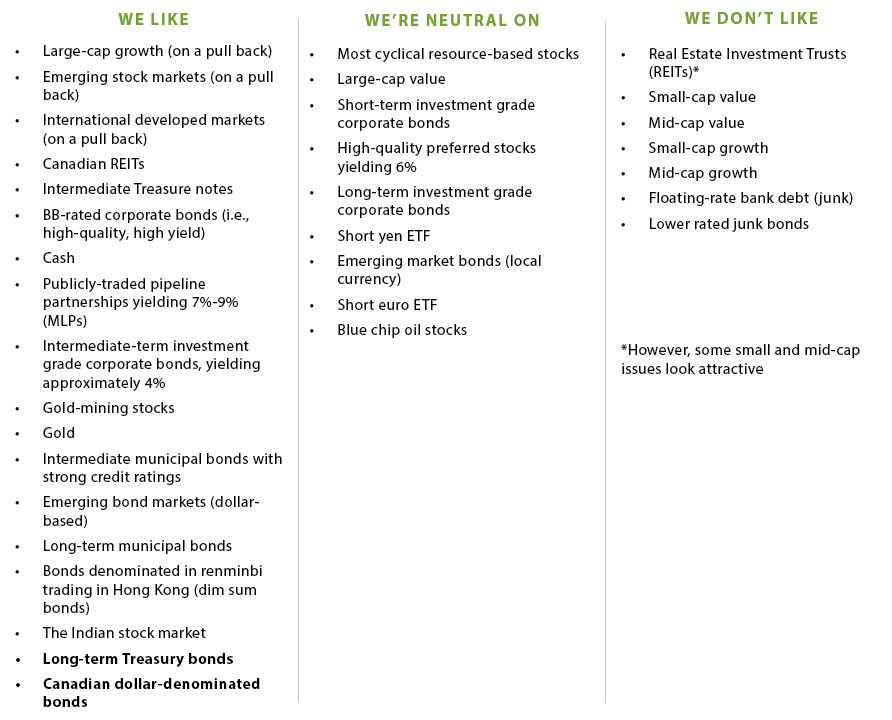

OUR CURRENT LIKES & DISLIKES

Changes are noted in bold.

DISCLOSURE: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.