“We’re moving from a world that was constantly globalizing to one breaking up into three different empires, each with their own currency, reference bond market, supply chains. There are massive investment implications.”

–LOUIS GAVE from a recent feature article on him in Barron’s

As is often the case in the current news environment, the endless headlines surrounding the relations between the United States and China overshadow the substance of underlying policy and provide little added value to the public. While this may make for good political theatre, it leaves many struggling to grasp what has been developing not just over the past year, but quietly for the past decade. In this week's EVA, Evergreen Gavekal partner Louis Gave offers thought-provoking insights on the complex “trade war” being staged by the two countries. Louis—and the venerable Charles Gave, with his 50 years of investment experience—argue there are far bigger implications for the ongoing battle than just the balance of imports and exports. The following examines the events that have led us to this point, as well as the options that may be exhausted going forward.

Of perhaps even greater value to our loyal readers, they shed light on the consequences of the structural changes occurring in global trade and how that shapes portfolio management decisions. What was very recently a world dominated by the narrative of globalization, allowing for many investment opportunities—especially in technology—we have since seen that storyline experience massive decoupling. As Bob Dylan said, “the times, they are a-changin’”—yet the Gaves wonder why investors have failed to change their investments with the times. Whether it be due to a lack of awareness regarding the two nations’ agendas, or uncertainty of how these changes impact the broader economy, or simply a complacency born of a decade-long bull market, investors are at risk of getting caught flat-footed by a reversal of one of the main drivers of the global economy since the end of WWII.

The wisdom in this piece gives much-needed clarity to those looking beyond the noise of the daily news cycle, and who are instead seeking to comprehend the power struggle between the world’s two behemoths from a big-picture perspective. Do enjoy.

INVESTING FOR A NEW COLD WAR

By Louis-Vincent Gave

Over Christmas, Charles and I hunkered down to write our latest book Clash Of Empires: Currencies and Power in a Multipolar World. In recent months, we have both met with many clients and discussed its core thesis that globalization is ending and the world is breaking into three separate economic zones with their own (i) trade and reserve currency, (ii) bond market of reference and, perhaps most importantly, (iii) dedicated supply chains. In short, 15 years after we described a new era of globalization in Our Brave New World that period may be drawing to a close. As such, recent discussions with clients have typically gone something like this:

Charles/Louis: “Do you believe that globalization was one of the most important macro trends of the past couple of decades?”

Most clients: “Absolutely.”

Charles/Louis: “Do you believe that globalization is coming to an end?”

Most clients: “It sure looks that way.”

Charles/Louis: “What are you doing about this in your portfolio?”

Most clients: “So far, nothing.”

The aim of this paper is to tackle the quandary thus highlighted.

The New Cold War

Given the back-and-forth between China and the US over the past year (trade wars, Huawei, threats to Hong Kong’s special status) President Xi Jinping has likely concluded that “just because you’re paranoid it doesn’t mean they aren’t after you”. Even if Xi and President Donald Trump exit their G20 meetings singing Kumbaya, China is likely to keep planning for a long, drawn-out cold war with the US. Given the bipartisan, anti-China rhetoric emanating from Washington DC, Beijing has to conclude that its key relationship has changed. The Nixonian policy of “bringing in China from the Cold” has now run its course. From Beijing’s perspective, the US’s new China policy seems to be containment—technologically, economically and geographically.

Thus, even while hoping for the best, any forward-thinking Chinese leader must now plan for the worst. This means dealing with China’s most glaring weaknesses of which there are three; namely, its dependence on overseas supplies of (i) technology/semiconductors, (ii) energy and (iii) US dollars.

Technology/Semiconductor dependence

The first job of any empire is to control key axes of communications (all roads lead to Rome, and all that). In this regard, the US was as likely to yield a key part of the world’s critical telecom infrastructure to Chinese corporates as it was to give up control of the world’s sea-lanes. After all, the valuable “goods” of tomorrow are more likely to be digital information passing through telecom switches than actual goods being moved on a ship.

Thus, when Australia and New Zealand a year ago announced that they would ban Huawei from building their 5G networks, it was possible to find a positive take on the headline: as two key US allies in the Pacific reject Chinese technology, the US security establishment might relax about the unfolding Chinese telecom breakthroughs. Unfortunately, perfidious Albion’s decision to embrace Huawei changed the dynamic. It’s almost as if Britain announced: “we will use Huawei” and the US security establishment replied, in one voice, “The hell you will. We’re shutting it down.”

China’s vulnerability stems from semiconductors being its biggest import item (about US$260bn a year against energy’s US$170bn) and that US semiproducers hold most of the world’s important patents. This is a theme that colleagues Dan Wang and Matt Forney at Gavekal-Fathom China have spent the past couple of years writing about. And suffice to say that the US deciding to “weaponize” semiconductor exports leaves Chinese policymakers with the following choices.

This second choice brings us to a remark made by an old friend Ajay Kapur (strategist at BofAML) that only countries that spend lots of money on their defence sectors have a thriving tech sector. Of course, spending heavily on weapons does not automatically trigger technological progress (if so, Saudi Arabia would have its own Silicon Valley). But it does seem to be a necessary, although not sufficient, condition for breakthroughs.

All about the military

Back in the days when France and Britain had proper military budgets, France invented the Minitel, while Alcatel and Marconi were telecom giants. Today, most tech breakthroughs seem to come from the US (which spends more on defense than the next ten countries combined), Israel (a big military spender as a share of GDP), South Korea, and perhaps even Taiwan. Thus, the first consequence of the unfolding “tech war” may be that China cranks up its military budgets, including large sums going into military “research”.

This doesn’t mean that China will “crack the semi code”. But it will throw both money and people at the problem. Twenty years ago, China produced less than a million university graduates a year, with roughly half in the sciences. Today, the ratio remains the same, but this summer more than eight million university students will graduate in China. It now has more graduate students than it had undergrads a generation ago. Now, scientific breakthroughs are not a numbers’ game, but numbers do help!

For US tech firms, this looks like the worst of both worlds: on the one hand, the US government is telling them to kiss goodbye the fast-growing Chinese market. On the other hand, China’s government is likely to heavily support new competitors challenging the US producers. Such competitors do not have to worry about making money, or even achieving positive returns on invested capital as the reason for being is first and foremost national security.

Recent weeks have seen a number of US tech firms announce that their sales outlook is darkening. Unsurprisingly, it seems that uncertain CEOs are choosing to sit on their hands until visibility improves—a development that may put the impressive outperformance of tech stocks under pressure.

Looking past current tensions, US tech stocks are threatened by the US-China standoff becoming a full-scale cold war. First, this would devastate supply chains, with major consequences for productivity and profitability. The second, and more alarming prospect, is that the breakdown in relations worsens to an extent that China’s policymakers conclude they have no interest in respecting intellectual property rights. After all, if we move into a world where Chinese exports into the US, and other developed world countries, become constrained, China may decide to forgo those markets. It could instead focus on reverse-engineering Western products like jet engines and medical devices with a view to selling them into emerging markets.

Such a possibility brings me back to themes outlined in Our Brave New World. Back in 2005, we argued that in a “globalizing” world, intellectual property would become ever more valuable. But, of course, for such a construct to sustain value, governments would have to agree to protect it.

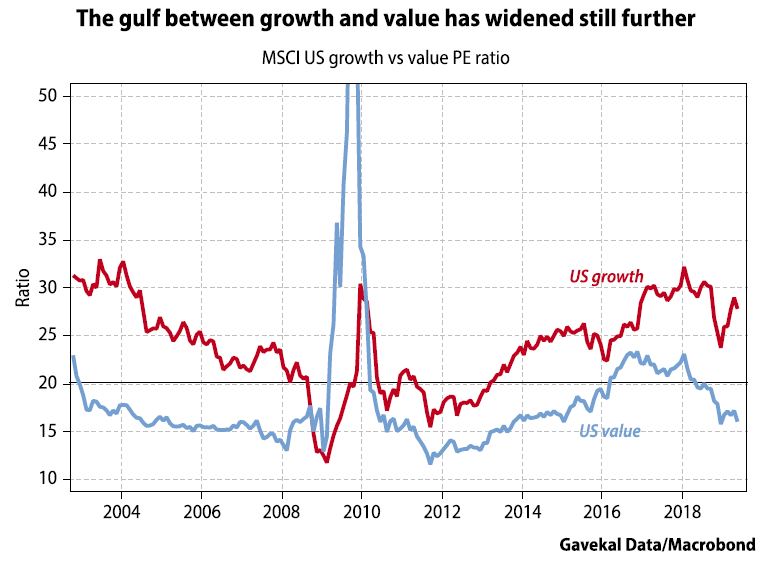

Over the past decade, financial markets have aggressively re-rated sectors like tech and healthcare which are rich in intellectual property just as “asset-heavy” sectors like energy and materials have underperformed (see chart overleaf). And just as the valuation gaps between the “IP heavy” MSCI Growth index, and the “asset heavy” MSCI Value index continues to widen, the US has decided to turn tech into the battlefield of the China-US cold war.

Charles’s family hails from Alsace, the French region that witnessed the 1870 Franco-Prussian war and epic battles in both WW1 and WW2. More than any region, Alsace was the battleground on which Franco-German rivalries played out for 75 years. And as anyone from Alsace will tell you, being the battleground is no prize. Once battles are over, one is left with ruins and, if lucky, one’s eyes to cry with. And this brings me to the US decision to make tech the battlefield on which the unfolding cold war will be fought.

This decision has been driven by the US holding a big comparative advantage in technology. But by picking this battlefield, could the US be replicating the French mistake at Dien Bien Phu? Back in 1954, the French were convinced they held superior troops, superior equipment and superior officers to the guerrilla-driven Vietminh (very unlike the French to feel superior). All they needed was to force the Vietminh into a proper, open battle and the Indochina war would come to an end. France picked its battlefield, the battle took place, and the war in Indochina did end—at least for the French, though not with the outcome the French general staff had expected.

Picking tech as a battlefield—a weaker dollar?

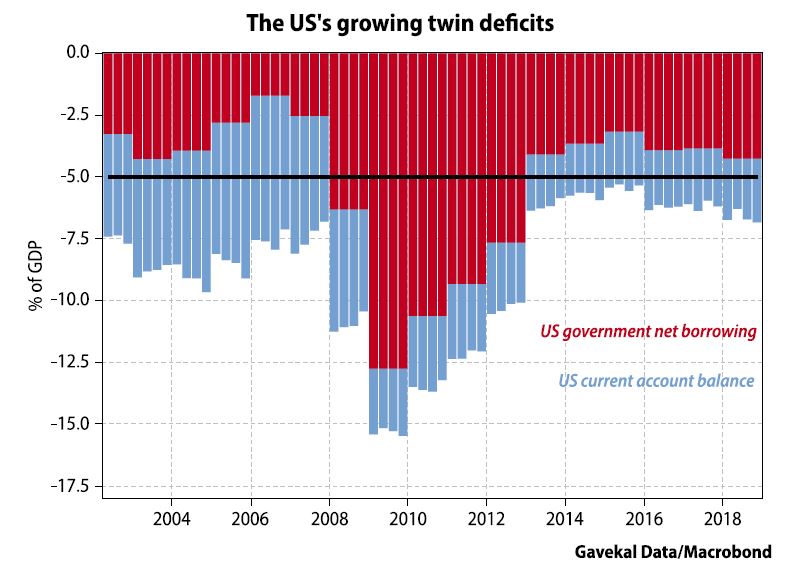

Amazingly for an economy in its 10th year of expansion, with record-low unemployment and record high asset prices, the US budget deficit rose by 39% in the first eight months of this fiscal year. It’s likely that for 2019, the deficit will be south of 5% of GDP. And despite the energy sector registering big productivity gains that have put the US on the cusp of being a net energy exporter, the US current account balance remains in the red. As a result, the US “twin deficits” remain south of 5% of GDP, a level which, for most countries usually means a weaker currency—unless one can attract foreign capital in a constant manner to plug those massive deficits.

Historically, the US has been good at attracting foreign capital. By promising to treat foreigners on a par with Americans, by maintaining an independent judiciary and defending property rights, it has been a safe-haven destination for at least a century. Indeed, it remains, the ultimate “risk-free” destination, unless you happen to be Iranian or Venezuelan.

The US’s haven status got a boost from European policymakers’ decision to impose the euro on a perfectly well functioning set of heterogeneous markets. It was also helped by so much wealth creation in recent decades coming from countries like China, Russia, Brazil and Mexico, where elites have sought to diversify their wealth away from domestic markets and currencies. In short, the US could run massive twin deficits and the dollar would remain the choice destination for asset allocators.

The changing rates environment

Having said that, there were probably still two factors which did help the US dollar stay strong in the face of large twin deficits: positive interest rate differentials, and the outperformance of tech.

The first is obvious enough. With Europe and Japan embracing negative interest rate policies, pension funds, insurance companies and even private savers have been forced to look abroad when seeking even a modicum of positive carry. Fortunately for them, such carry could still be found by investing in long-dated US government bonds and hedging the currency risk. In fact, up until recently, buying treasuries and hedging the US dollar risk typically delivered at least 100bp more in carry than the outright ownership of German bunds, French OATs or Japanese government bonds.

But as we write, this is no longer the case. As a result, European and Japanese yield-seeking institutions are left with a couple of obvious options:

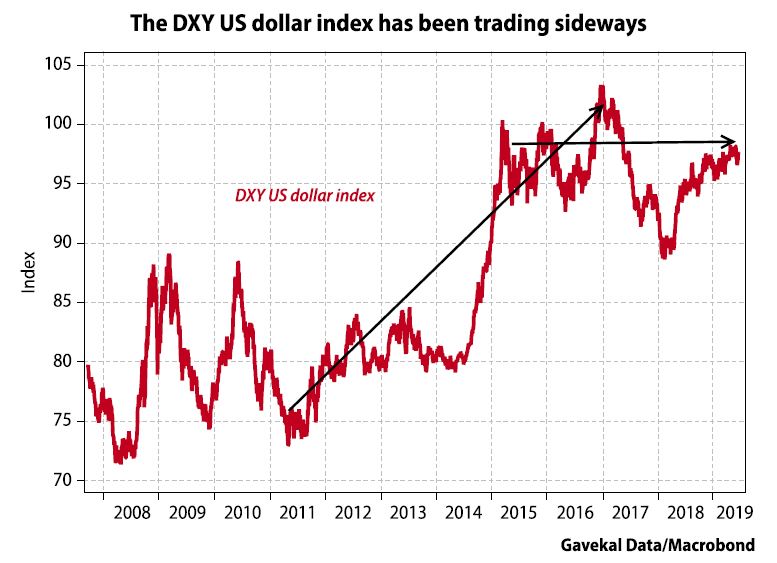

There is no more free lunch as European and Japanese institutions must now choose between greater signature risk or currency risk. Anecdotal evidence points to them going for the latter. After all, the general view has been that the US dollar could only rise, thanks in part to Fed hawkishness and the US’s strong economic growth. However, as US economic data starts to soften, as the Fed gets more dovish, and as the fiscal deficit shows no sign of abating, “long-US dollar” positions may become harder to justify. It should be noted that the DXY has not held new highs despite bad news-flow for the euro (Italian crisis, yellow vests, Deutsche Bank, the tariff threat to German autos), the pound sterling (Brexit), commodity currencies and even the yen.

Beyond interest rate differentials, the second main reason foreigners likely deployed capital in the US over recent years is that the US had a sector that almost everyone else lacked, namely, technology. After all, a European investor looking at Procter & Gamble could just as easily buy Unilever. Total or BP can compete for capital with Exxon or Chevron. BMW or Daimler with Ford or GM. But who in the developed world’s equity markets can compete with the lure of Google, Facebook, Apple, Microsoft or Amazon? Perhaps the utter domination of US tech has not only triggered the massive outperformance of US equity markets, but has also helped keep the dollar high in spite of the US’s sustained twin deficits.

It could be argued that as money keeps pouring into US funds running venture capital and private-equity strategies as well as exchange-traded funds, then there is good reason for the dollar to stay strong. Yet as investors adjust to the technology sector being the new battleground of the unfolding cold war, a possibility that will hurt tech valuations, will foreigners keep pouring money into US tech? Take Saudi Arabia’s Mohammad Bin Salman Al Saud as an example: having taken a bath on Uber and a cold shower on Tesla, will the Saudi crown prince now decide that art investing makes more sense?

The second Chinese weakness—oil

Looking through the list of China’s key imports, oil is the next item that follows semiconductors. And a few weeks ago, with John Bolton and Mike Pompeo advocating regime change in Venezuela and Iran, it must have looked—at least from China’s perspective—like the US was trying to engineer a spike in the oil price. After all, what better way to create a balance of payments problem in China? First, block Chinese exports to the US, thereby triggering a collapse in China’s dollar earnings. Second, cause a surge in China’s import costs through a higher oil price.

Until a few years ago, such a move would have been too costly for the US to contemplate. However, as it becomes self-sufficient in energy, a high oil price no longer means sending vast sums to Mexico, Venezuela, Canada or elsewhere. Instead, it means that money flows from the (blue States) North East and California down to (red states) Texas, Oklahoma, Louisiana, North Dakota and Alaska.

Fortunately, Trump remembered that he was not elected to see US soldiers bogged down in more foreign theaters and reined in Bolton, Pompeo and other hawks in his administration. But, as far as China is concerned, the energy threat remains real and will push China to seek better long term solutions. These will likely include:

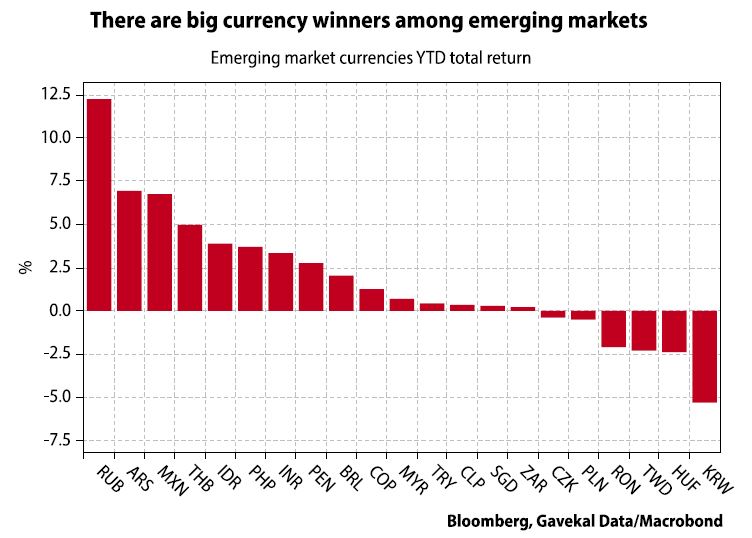

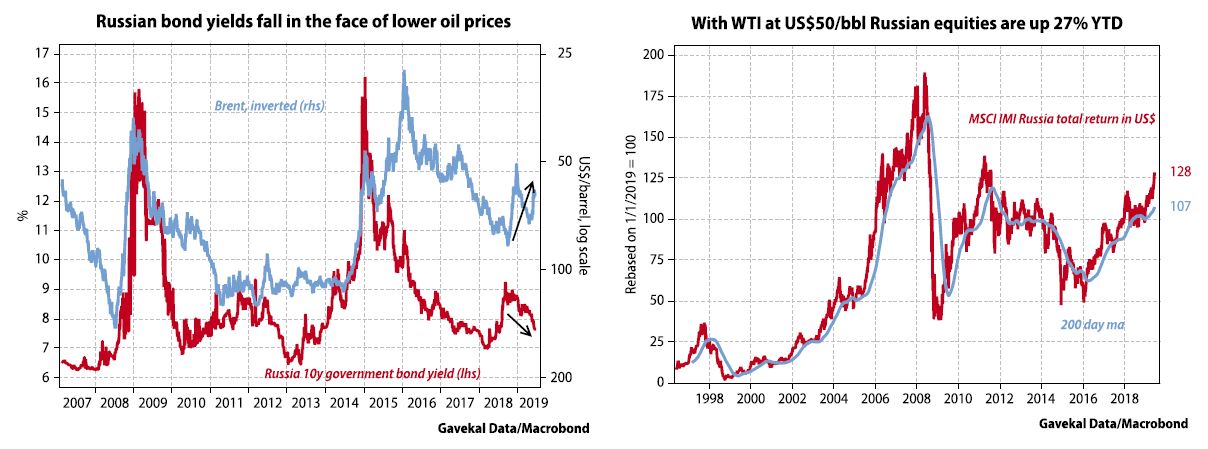

This brings us to the recent love-in between Presidents Vladimir Putin and Xi Jinping, the 13th official pow-pow between the two heads of state in the past six years. This saw Xi declare that Putin was his “best friend”. And as he did, you could almost see Putin thinking “I am very happy to be your best friend. Here is my friendship bill!”. In short, the more that US-China tensions rack up, the more important Russia becomes to China. This may help explain why, so far this year, the Russian ruble is the world’s best performing currency.

The Russian bond market is among the world’s best performing markets, with 10-year yields having dropped some 110bp (in spite of a lackluster oil price). At the same time, the Russian equity market has outperformed all others with a 27% year-to-date rise in US dollar terms.

The third Chinese weakness—US dollar dependency

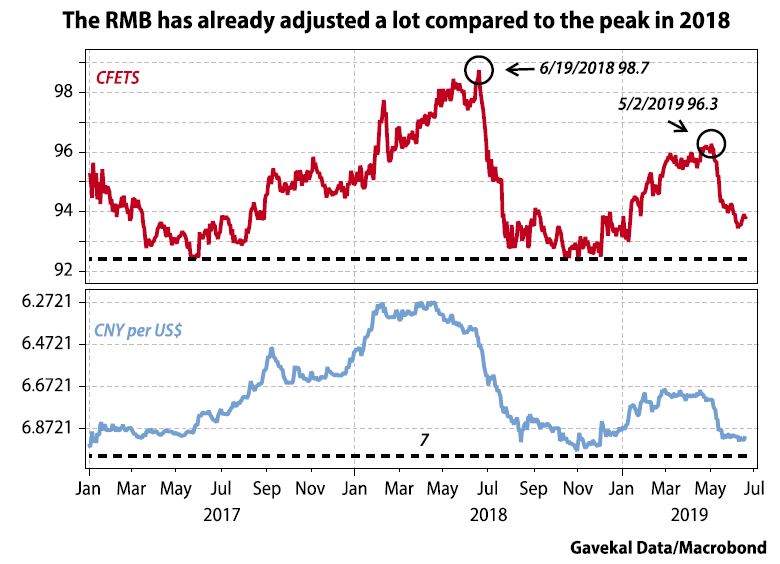

Following Trump’s May 5 tweet storm announcing that a trade pact with China was no longer an option, the renminbi promptly fell by -1.5%. Consensus opinion was that without a trade deal, Chinese growth would suffer. From there, Chinese policymakers would have little choice but to throw more stimulus into their economy, which would amount to adding more bad debt to an already large pile. Such an outcome would hardly be a positive development for the currency.

However, Chinese officials then came out and warned speculators that the renminbi would not be allowed to weaken much, if at all. This gave markets the sense that a line of sorts was being drawn, either at the RMB7 to the dollar level, or, at the very least, at the 92 level for the renminbi’s CEFTS basket.

These warnings were given more heft when Xi traveled to the site of the launch of the Long March and promised China some tough times ahead. It wasn’t quite a Churchillian promise of “blood, sweat and tears”, but nor did it give great comfort to those hoping for another wave of stimulus. Clearly, the Chinese equity market is more into gentle strolls then long marches!

This begs the question of why President Xi would make such a show of refusing the “easy path” of greater monetary stimulus, and possible currency devaluation. One obvious answer is that devaluing the renminbi could cause even more problems. First, it would anger Trump and likely make a compromise even harder to reach. Second, it may spur capital outflows. But perhaps most importantly, it would set back China’s long term goal of de-dollarizing Asian trade, and her own commodity imports.

Indeed, on the basis that China is run by control-freaks, why did it spend the past decade gradually liberalizing the country’s exchange rate and fixed income markets and so cede control of two most important prices in any economy? The answer is obvious enough: following the 2008 crisis, China’s leaders understood that depending on the US dollar for trade finance left it at the behest of American banks to keep providing the financing.

This was an uncomfortable situation back in 2009. But what is it like in 2019? Will the past year or so have re-enforced or lessened Xi’s desire to reduce China’s dependency on the US dollar? To ask the question is to answer it. And of course, to de-dollarize her trade, China needs to ensure that the renminbi remains a “strong currency”. Otherwise, the renminbi will be seen as an EM currency like any and China would remain an economic vassal of the US.

Conclusion

Assuming that the US-China standoff is not merely a trade war but the start of a new cold war then the shift in the US-China relationship will cast a long shadow over financial markets. As reviewed above, the new cold war could end up being:

In short, for a world that may be going through a dramatic shift, one wants to be long the assets that no-one today owns, like Chinese and Russian bonds, and underweight those that everyone and their dogs are overweight like the US dollar and US technology stocks.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.