"We learn from history that we do not learn from history."

- Georg Wilhelm Friedrich Hegel (courtesy of John Hussman from his June 14, 2014 Weekly Market Comment)

The next 20%? It’s not often when my colleague, Anatole Kaletsky, and fund managers Jeremy Grantham and Bill Miller all agree. But, lately, they each have come out with some remarkably similar commentary about the future of the stock market. The trio is an interesting combination because Anatole and Bill Miller are basically perma-bulls (the latter being famous for his 15-year streak of beating the S&P before incurring several disastrous years), while Jeremy Grantham is known for a much more jaded valuation eye.

As earlier EVAs have conveyed, Jeremy’s firm, GMO (the "G" standing for Grantham), manages over $110 billion in assets and has compiled one of the best forecasting records for long-term asset class returns. Unlike Bill Miller, and most other Wall Street grandees, Mr. "G" was resolutely—and correctly—bearish on housing and stocks in 2007. And, in glaring contrast to so many of the congenitally bearish persuasion, he switched over to the buy-side in early 2009, as memorialized by his exceptionally timely essay back then, Investing When Terrified.

Therefore, it occurred to me that this month’s "Guest" EVA edition should examine the unusual similarity in their outlooks, on both a short-term and long-term basis. As you will soon see, all three believe we may be on the verge of a 15 to 20% market surge. Anatole recently penned a piece, cleverly titled An Uber Bubble Awaits, playing on the issue (or, more accurately, issuance) of the highly popular car service’s impending IPO. In it, he asserts that the oft-quoted (including by me) axiom "Sell in May" should be "Buy in May" this year. He even brings up an aspect that I have in the past: The market could be setting up for a 1987 replay, with many months of "massive (and massively dangerous)" equity performance about to unfold.

Bill Miller is also suggesting that stocks may have another big jump ahead, as much as 20 to 30%. Yet, echoing Anatole, he further observes this would put the market "in a very vulnerable position."

As relayed in prior EVAs, Jeremy Grantham has been on record for months stating that stocks are likely poised for "a substantial and quite lengthy last hurrah." In GMO’s most current quarterly letter to investors, he outlines his logic on why he thinks we are likely heading to 2250 on the S&P 500, which would be up about 15% from here. This would also qualify as a "2 sigma" event, which is geek-speak for a full-blown stock bubble. (However, he does expect the months between now and October to include a correction that will set the stage for the final eruption.)

Accordingly, the two unifying themes from these three formidable gentlemen is a higher market near-term, with the caveat of a possible shakeout along the way conceded by Anatole and Jeremy Grantham, and then the moonshot. It’s that last part that is most meaningful in my mind, because all three admitted the market will eventually get to the point where the ingredients will be in place for the next disaster—Anatole’s "massively dangerous" phase.

Of course, we might not ever get there. In my view, this would actually be a much preferable outcome. As another brilliant market maven, Burton G. Malkiel, once observed: "The bigger the binge, the longer and more severe the hangover." (Why do so many of us forgot those wise words when the hooch is flowing freely?) On the topic of currently overcooked conditions, I’m also highlighting in this week’s "Guest EVA" a link to another star in the GMO constellation, Ed Chancellor. Ed, who is apparently departing that great firm, is of the opinion that there already is a bubble epidemic. Click here to read Ed’s pieace (it begins on page 12 of the GMO letter).

As evidence, he and Mr. Grantham, cite the example of the $58 million dog, shown to the right. By the way, this pup isn’t a one-of-a-kind and wasn’t even fashioned by the creating artist’s (Jeff Koons) own hand. Ironically, its name is Balloon Dog, which seems utterly fitting given all the monetary helium pumping up "collectibles" and other asset prices around the world.

Because it’s GMO’s policy not to let others run their Quarterly Letters, we are only able to attach a link to these essays on their website. However, I’d strongly urge all EVA readers to check them out (Mr. Grantham even

puts in a kind word for one of my favorite sources, John Hussman, whose former guru status has been in a vicious bear market, although I sense a major reputational rally looming). Click here to read Jeremy’s piece (it begins on page 2 of the GMO letter) .

Before I pass the baton to Anatole, unfolding—no, make that unraveling—events in the Middle East drive home one of the messages we have brought up recently: The dangers of the US foreign policy "taper" (please click here to read Tyler’s comments on this topic). Lost in the focus on the Ukraine and, now, Iraq, is that China is behaving most belligerently in Southeast Asia, especially toward Vietnam. When the world’s policeman goes on strike, the thugs tend to come out of the woodwork (in the case of Iraq, armed with alarming quantities of abandoned US military hardware).

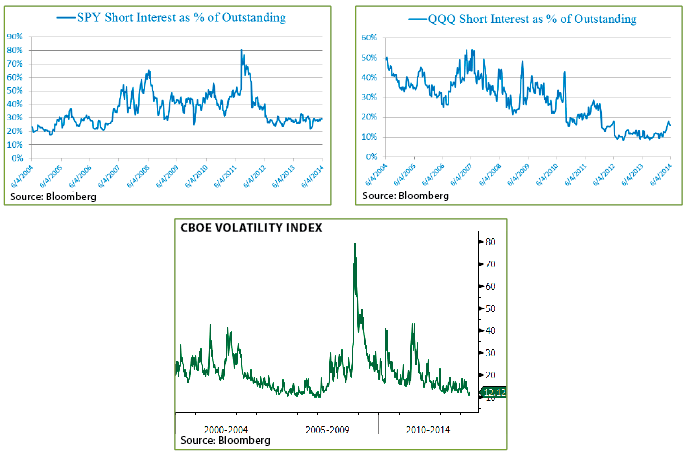

With margin debt at record highs, short-interest very subdued, asset bubbles all around, volatility measures on Valium, and the planet looking increasingly hazardous, it might not be smart to hold out for the last, possibly illusory, 20%. In fact, it might be time for prudent investors to act with all the courage of the Iraqi army in front of Mosul.

![]()

An Uber Bubble Awaits

Anatole Kaletsky

Last week was clearly an important one for financial markets and the world economy. Friday’s US payroll data confirmed that all the jobs lost since 2008 have been restored. The European Central Bank (ECB) overcame the opposition of the Bundesbank and joined the Federal Reserve, Bank of Japan and Bank of England in the ranks of growth-oriented central banks that are willing to whatever is necessary to pump up inflation and nominal GDP. And peace talks between Russia and Ukraine reinforced our view that Putin’s annexation of Crimea marked the end, not the beginning, of the most dangerous period of geopolitical tension in Eastern Europe.

Considering all this good news, it is hardly surprising that "sell in May" this year became "buy in May" as we suggested it might. The S&P 500 hit new records on four days of five days last week and closed at a high just below 1950, at the top of a remarkably orderly bullish trading channel. Yet it is possible that this week’s most important financial event was neither the US payrolls nor the ECB initiative, nor the rapprochement with Putin. It was the pricing of Uber, a taxi-dispatching business that many people had not heard of until a few months ago. Uber was valued by second-round equity investors at $17bn, which was some 60 times its rumoured revenues and presumably a much higher multiple of its profits (if any).

To understand the significance of Uber’s valuation, let us recall an observation we have often made in the past about asset pricing. The rise and fall of asset prices depends on three distinct factors. The obvious determinant is nominal economic growth (in the case of equity indices, bonds and other macro trades) or corporate cash-flow (in the case of individual equities or credits). The second factor, which attracts almost as much attention, is liquidity and monetary policy. But the third determinant, which is often overlooked by economists, is equally important: it is the valuation that investors decide to attach to any particular cash-flow. Given that asset prices are made at the margin and respond to events which are not expected, the main driver of bull or bear markets will usually be whichever of our three determinants is most uncertain.

Immediately after the 2008 crisis this was economic activity. After a few years of gradual economic recovery, the market’s attention shifted towards monetary policy, especially in the period of the euro crisis and the US taper tantrum. But what happens when both economic prospects and monetary policy become as clear and predictable as they have ever been, which seems a fair description of the situation in all the major economies, especially after last week’s US economic figures and ECB policy announcements? The answer is surely that investors will focus on the third aspect of the asset-pricing triangle: valuations.

Which brings us back to Uber and the other darlings of the mobile networking bubble. Two months ago, investors seemed to inaugurate the new valuation-driven phase of the equity bull market by shifting out of expensive growth stocks considered impervious to economic cycles into cheaper stocks which had been neglected in the phase of economic and monetary uncertainty. This rotation from growth to value contributed to the equity market weakness earlier this year, since the overvalued leaders retreated faster than the undervalued laggards could advance.

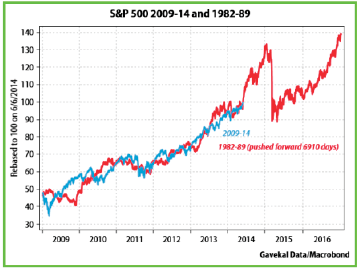

It seems, however, that this leadership rotation may now be over; investors are again falling in love with miracle and fantasy stocks. If this is true, then the bull market may now be entering a new phase that is both more exciting and more dangerous. As momentum-driven valuations keep rising, a severe correction of 20% or more will become inevitable. But the cause may not be weak growth, as bears have generally predicted; but simply a recognition that valuations have become excessive, perhaps underlined by a modest increase in long-term interest rates. In this respect, conditions today are becoming reminiscent of the period before the stock market crash of 1987.

Then, as now, equity prices had risen almost without interruption for five years, the start of a structural bull market that nobody at the time believed to be sustainable. Then, as now, a period of extreme economic pessimism was giving way to greater confidence about the stability of the world economy. Then, as now, valuations were rising from above-average to very expensive (the S&P 500 peaked at 22x reported earnings) especially in comparison with bond yields that were creeping up from 8.5% to 10%, alongside a strengthening economy.

Do all these echoes of 1987 imply that investors should bail out of equities now? Not at all. To trigger a valuation-driven bear market, Price-earnings ratios would have to rise well above their present levels since the S&P 500 presently trades at 19x reported earnings—and in the absence of a recession or sudden margin squeeze, that will only happen if equity prices keep rising, probably with sharply accelerating momentum. That is what happened in the nine months leading up to October 1987. Of course, history never repeats itself exactly, but chart to the right is worth a glance.

If we take the 1987 analogy literally, then nine to twelve months of massive (and massively dangerous) equity outperformance may be just starting. In that case, the best strategy will be to remain invested until equities become absurdly expensive, but buy lots of downside protection, especially while volatility remains absurdly cheap. And if you fail to get out at the top, as you almost surely will, don’t worry. After a bear market that is caused by over-valuation, rather than recession, equities will recover quickly and eventually rise to much higher peaks. That, at least, is the lesson from 1987.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.