Below are Evergreen Gavekal's Likes/Dislikes for December 31st, 2021.

Blasphemy, Revisited

There’s little doubt that my most controversial EVA of 2021 was my early year “Take Profits!” edition. When you consider how many feathers I ruffle on a regular basis, that’s really saying something. In fact, it was so polarizing--producing both an outpouring of positive and negative feedback--that I felt compelled to send out a clarification message the following week. This controversy was despite my suggestion was to raise cash and book some gains but not to exit stocks entirely, or even largely.

In hindsight, I should have been clearer in “Take Profits!” that most of my concern was focused on what I have long called the “COPS”, Crazy Over-Priced Stocks, an error I sought to correct in the January 8th, follow-on EVA. However, those were in fact the issues that I particularly took issue with in “Take Profits!”, particularly Quantumscape, Snowflake and Airbnb.

Subsequently, the first two did struggle, with Quantumscape plunging almost immediately after that EVA went out. In the case of Snowflake, it melted from $280 down to $200 before another explosive up-move to $340 about where it finished 2021. (Kudos to our growth strategy team for being more constructive on SNOW after it got hit.) Airbnb remained surprisingly non-volatile and finished up about 20% for the year but I continue to think its $100 billion market cap is hard to justify based on the challenges its business model faces, such as intense local opposition to short-term rentals. As far as my Quantumscape slam, it lost about two-thirds of its market value by mid-summer and has essentially flat-lined since.

As the year went on, I intensified my warnings against the multitude of other manifestations of speculative insanity which included the meme stocks, like Gamestop and AMC Entertainment, as well as the SPAC* craze. For the most part, these hit their crescendo in the first half, even first quarter, of the year and then embarked on a series of severe declines. As others have noted, it does appear that somewhere between February and June of last year, we achieved “Peak Insanity”, when it comes to the frenetic trading activity in these lottery-ticket type stocks. (Or should that be “stonks”, to use the Robinhood/Reddit crowd lingo?).

In this week’s main EVA section, Michael Johnston, Jr., adeptly conveys how overheated conditions also became in the Initial Public Offering (IPO) space. Michael has been working on this for the last few weeks and was waiting for calm conditions to run it; ironically, just yesterday the Wall Street Journal published this front-page story:

Michaels’s EVA is filled with fascinating factoids about the feverish IPO market, at least in terms of deal volume. But, as the Journal also pointed out, the performance for those “lucky” enough to get in at the offering price—which is exceedingly difficult to do (when was the last time you received one of those?)—the results have been less than impressive.

*SPAC stands for Special Purpose Acquisition Company. As noted in earlier EVAs, these are basically “blank check” entities and are typically publicly traded shell corporations. These facilitate the acquisition of private companies and effectively circumvent the need for the onerous disclosures required by traditional Initial Public Offerings.

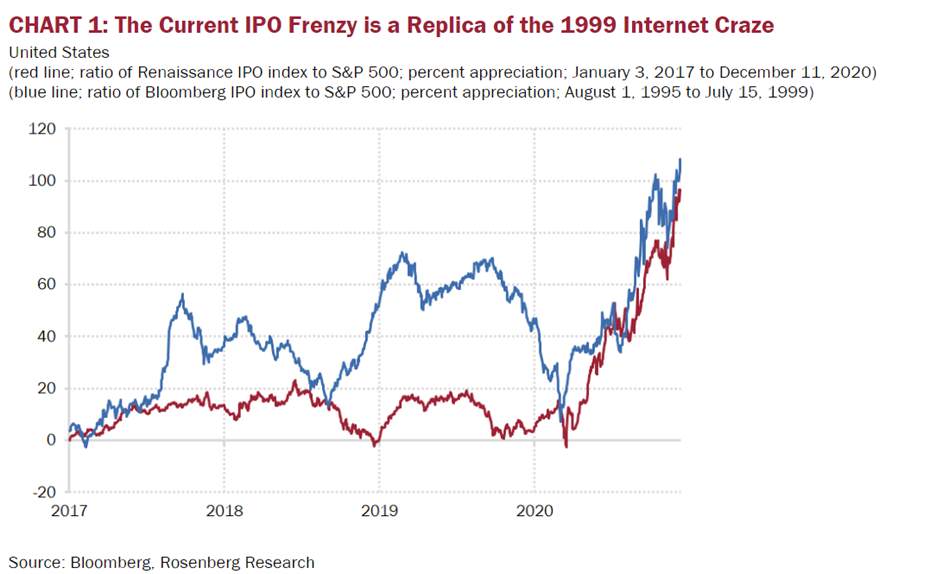

According to the Journal’s analysis, the average IPO was down 9% from its underwriting price. This undoubtedly reflects that there was far too much euphoria engulfing this market niche. To that point, here’s a chart I ran in “Take Profits!” that underscored the intensity of the IPO mania at the time:

Related to this, was one of Michael’s more intriguing tidbits, in case you missed it: “However, what’s fascinating is that while 2021 was a banner year for newly minted $10 billion+ companies, decacorns that hit public markets in 2021 fared worse than any other year on record.” Decacorns, as he explains, are those start-ups with $10 billion private market valuations. These were previously almost as rare as the mythic unicorns on which their name is a word play. Regardless, whether it is Decacorns or IPOs in general, it does appear the Wall Street underwriting machine is swamping the demand for these deals.

As various EVAs over the last two months have noted, there has been serious carnage over that timeframe in a wide range of aggressive growth stocks. Yet, there remains a multitude that continue to trade at heroic, if not absurd, valuations. In my view, most of these are poised to get crushed in 2022. Of course, I could be dead wrong and I would have said the same thing (and did) about Tesla many hundreds of billions of dollars of market cap ago.

Essentially, I believe Bubble 3.0 has only partially popped, with more “value restoration” up ahead. As I’ve also expressed in recent months, many of the far more reasonably priced stocks that are tied to the economy’s fortunes, or misfortunes, also were taken to the market’s woodshed. This validated some of the fears I expressed about them a year ago. Delta and Omicron have, of course, been the downside catalysts. Lately, though, these more cyclical issues have been perking up and I do believe they will be the stars of the first half of 2022. Related to this, I also feel the odds favor the US economy will surprise on the upside. On a less sanguine note, so will inflation, in my view.

On that topic, to wrap up this mini-overview of my calls coming into this year, I believe it’s fair to say that my overarching “anticipation” going into 2021, which I maintained through the year, was that inflation was a much bigger problem than the Fed wanted the world to believe. Here’s what I wrote last January:

“In fairness, one of the near-term risks I brought up, the GOP losing control of the Senate, turned out to be a non-event. My suspicion is that, had it hung onto one seat and maintained a majority, the market would have risen on that news, too. Personally, I believe the Democratic victory increases the odds of an inflation problem later this year due to the likelihood of another trillion or so of near-term deficit spending, with potentially trillions more later this year and next, funded by the Fed’s magical money machine.” Of course, I have total recall when it comes to my good calls! Hey, I’m only human!!

On that note, I would like to wish all of our clients and readers, a most prosperous and, especially, healthy, New Year!

Positioning Recommendations

(Note: there are once again very few changes this week.)

LIKE

- Large-cap growth. (Some of the Teflon mega-cap issues have begun to crack of late. The better risk/reward ratios, however, can be found in large-cap names that aren’t in the mega category.)

- Certain international developed markets, especially Japan (Use the recent pull-back for adding to or initiating position in ETFs like EWJ. The Japanese market should be a beneficiary of overseas investors pulling capital out of China.)

- Publicly traded pipeline partnerships, i.e., MLPs and other mid-stream energy securities. (Buy on weakness! They look poised for their usual late December, January rally; this appears to be underway.)

- Gold-mining stocks (Ditto!)

- Gold (The miners appear far more undervalued at this point.)

- Silver (It has more snap-back potential than gold currently.)

- Select international blue chip oil stocks (Again, it’s time to be a buyer for long-term, contrarian investors.)

- Short-term investment grade corporate bonds (1-4 year maturities; favor shorter maturities due to rising inflation risks because of the likelihood that the Fed and the Treasury are over-stimulating the US economy.)

- Emerging market (EM) bonds in local currency (focusing on stronger countries, particularly in Asia)

- Large-cap value (Use Omicron-driven weakness to accelerate accumulation especially in more cyclical companies.)

- High-dividend equities with safe distributions (These, too, have been hit; thus, add selectively though they lack the rebound potential of more aggressive issues, outside of economically-sensitive areas.)

- Most cyclical resource-based stocks (Buy more aggressively.)

- BB-rated corporate bonds (Buy more selectively after a spectacular rally and favor shorter maturities.)

- Canadian REITs (Avoid office issues for now.)

- South Korean Equities (S. Korea remains one of my favorite markets.)

- Certain “Virus Victim” equities such as refiners, homebuilders, and select retail stocks (Certain retailers look extremely attractive right now, especially one that is based in Seattle with a famously generous return policy.)

- Investment-grade floating rate corporate bonds (Despite a vigorous rally this year, there remains decent long-term value in this bond market niche.)

- The higher quality mortgage REITs (Previously, we had recommended profit-taking; use recent weakness for re-accumulation.)

- Floating rate bank loans (Although GDP growth this quarter came in much slower than Q2, this should be a pause not a reversal. Thus, the still healthy US economy reduces default risks and the floating-rate structure of bank loans mitigates inflation risks.)

- Copper producers. (The largest US copper producer has declined about 7% from its summer peak though it has rallied nearly 35% since its fall low. It continues to have long-term appeal due to copper’s critical role in EVs and their batteries.)

- A relatively new sector recommendation is healthcare stocks. Many have corrected and are trading at alluringly attractive valuations, often with lush dividend yields. (Use the recent weakness in some pharma names to accumulate; however, be selective as some have experienced strong rallies recently.)

- For those looking to for downside hedges, one of my personal favorite shorts is the Indian stock market. Its valuation looks indefensibly inflated.

NEUTRAL

- Uranium and uranium producers (There are better opportunities elsewhere for now.)

- Renewable Yield Cos (Based on the hefty rally that has occurred with this group in recent months, justifying our buy rating on them earlier this year, we are downgrading them to neutral; some profit-taking is reasonable despite bright long-term prospects.)

- A wide range of high-income securities, including preferred stocks (Preferred stocks look less attractive with prices up, yields down, and inflation risks on the rise. As with bonds, we prefer the floating-rate variety.)

- Intermediate-term investment-grade corporate bonds, yielding approximately 2.25% (Now rated neutral due to our increasing inflation concerns and the paucity of attractive yields; they have been under pressure lately due to rising rates overseas and escalating inflation concerns.)

- Mid-cap value

- Emerging stock markets; however, a number of Asian developing markets look undervalued (Caveat investor: These are much less bargain-rich than they were a year ago. China is an exception; its market has been crushed creating interesting value plays for brave investors. However, it’s continuing war on its best companies is a large and legitimate concern. Further, I would note key Chinese equities are breaking multi-year support.)

- US-based Real Estate Investment Trusts (REITs) (It is critical to be highly selective with this sector; however, the reopening of the US economy, despite recent challenges, should relieve pressure on some of the most impaired sub-sectors of the REIT universe—unless they are exposed to cities and/or states that are seeing significant population and business outflows.)

- Cash

- Canadian dollar-denominated short-term bonds (The recent yield spike makes these even more interesting—literally.)

- One- to two-year Treasury notes

- Traditionally “safe” sectors such as Staples and Utilities (There has been a mild pull-back in some utilities; thus, they are somewhat attractive at this point. However, rising inflation is typically a negative for this interest rate sensitive sector. Certain Staples stocks have been hard hit of late and offer decent upside, especially relative to their low risk.)

- Virus Victors (I.E, those companies that have benefitted from global lockdowns and now sport premium valuations. Many have retreated significantly of late; Clorox, for example, remains down materially from its peak.)

- Small-cap value (This style has corrected 4.9% of late; however, it has held up considerably better than its growth-oriented peer—see below.)

- European banks (Shifting these back to neutral due to improving vaccination prospects on the Continent. Still-prevailing negative interest rates in Europe are very hard on bank profitability.)

DISLIKE

- Intermediate-term Treasury bonds (These have been weakening a bit lately, possibly due to a lack of liquidity at year-end.)

- Small-cap growth (Since late-February, around the time of our negative call on this style, it is now down 9.8%; in fact, it has swooned by that amount in just the past month (down almost 10% since 11/8).

- Removing the short recommendation on small cap due to its recent correction. Small cap growth, however, continues to look vulnerable, especially should there be an oversold rally soon (which has happened to a degree a recently).

- Long-term treasury bonds (We have been negative on long bonds all year due to our inflation fears which have been realized; although some are celebrating their recent price bounce, long-treasuries remain down -2.2% on a total return basis this year. After inflation, the long treasury has lost approximately -8%.; we find this far short of celebration-worthy.)

- Long-term investment grade corporate bonds (These are viewed negatively because of the narrow yield gap, or spread, between corporate debt and treasuries combined with our escalating inflation fears. However, there are a smattering of long-term issues that still offer attractive yields. Long-term corporate bonds have had a negative total return of -6.0% for the year.)

- Most municipal bonds (Munis have bounced a bit lately but we remain negatively disposed to longer issues.)

- US dollar (The dollar has rallied recently, pushing it up roughly 6.9% for the year. This is despite the fact that the US is running a trillion-dollar trade deficit and the Fed continues to fabricate money at over a $1 trillion annualized rate. Thus, the dollar’s long-term outlook appears very challenging and it remains overvalued versus many currencies, especially those in Asia.)

- Many semiconductor tech stocks (Semis have held up comparatively well during the shakeout; many of these names look extremely pricey and hence vulnerable.)

- Mid-cap growth

- Lower-rated junk bonds (For the first time ever, junk bonds “provide”, on average, a yield below inflation; thus, their other moniker, high yield, no longer applies. In my view, the lowest rated junk bonds offer the worst/risk reward.)

- Green energy stocks (Note, this refers to equities not the Renewable Yield Cos; most of the former had explosive up-moves in 2020 and into this year; lately, though, many green energy plays have been hit hard, especially the dodgiest issues like Lordstown Motors and Nikola. The recently public new EV truck maker Rivian looks ludicrously overvalued; justifying that negativity, it has lost about 39.4% from its recent peak, down another 10% this week.)

- SPACs (Special Purpose Acquisition Companies, which are structured to greatly favor insiders and disadvantage retail investors. The SPAC ETF has fallen 38.4% from its February highs, justifying our negative stance on this highly speculative slice of the market.)

- Most new issues (Earlier this year, the IPO market was as frothy as I’ve seen it other than the giddiest days of the dot.com era; there are also signs the new-issue craze is fading, per this week’s main EVA. A number of IPOs are trading below their offering prices.)

- Despite a disastrous February, most of the popular Reddit/WallStreetBets stocks still have material downside. (As noted above, my repeated bearish views on these lottery tickets have been vindicated, at least for now.)

DISCLOSURE: This material has been distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, are subject to change, and reflect the personal opinions of David Hay (an employee of Evergreen Gavekal) as of the date of this publication. This publication does not necessarily reflect the views of Evergreen's Investment Committee as a whole. All investment decisions for Evergreen clients are made by the Evergreen Investment Committee. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed, and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this letter have been selected to illustrate the author's investment approach and/or market outlook and are not intended to represent Evergreen's performance or be an indicator for how Evergreen or its clients have performed or may perform in the future. Each security discussed in this letter has been selected solely for this purpose and has not been selected on the basis of performance or any performance-related criteria. The securities discussed herein do not represent an entire portfolio and, in the aggregate, may only represent a small percentage of a Evergreen's client holdings. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Before making an investment decision, the reader should do their own research and/or consult with their financial advisor. Past performance is no guarantee of future results. All investments involve risk, including the loss of principal.