“The Fed is on the wrong side of the market.”

- Jim Grant

“Jerome Powell called low inflation...the pre-eminent economic challenge of our time. So the Fed bet on a new policy regime to get inflation higher. It worked. It’s not the first time a central bank wanted a little more inflation and got a lot more.”

- Former member of the Federal Reserve Board, Kevin Warsh, in a 12/13/21, Wall Street Journal Op-Ed

_____________________________________________________________________________________________________

It’s not an exaggeration to say that the raging debate about whether inflation is transitory or persistent is the most important “opinion exchange”, at least for market participants. Of course, this assumes China doesn’t invade Taiwan, and that Russia doesn’t attack the Ukraine, and Omicron remains highly transmissible but not very virulent.

As most EVA readers are aware, Fed-head Jay Powell has told the world that when it comes to inflation it’s time to retire the word he used so often, “transitory”. Ironically, though, as is validly pointed out by this week’s Guest EVA author, Gerard Minack, both the stock and bond market are already acting as if the inflation threat is indeed a fleeting one. To wit, would the 10-year Treasury note be trading at 1.4% if bond investors truly believed inflation was destined to stay in the 6% range? Of course, this ignores the Fed’s influence on keeping rates down through its multi-trillion buying spree, all financed with the magical pseudo-money it simply wills into existence. Despite that influence, current long-term yields appear way out of synch with the facts on the ground—and the prices in the supermarket.

It also overlooks the stock market’s sudden fragility. As this newsletter has been discussing over the prior two issues, there has been a truly shocking breakdown among a long list of equities, particularly of the high P/E small- and mid-cap growth variety. This erosion has continued into this week. Roughly 37% of the Nasdaq constituents are now down 50% or more from their 52-week peaks. 65% are down at least 20%. (The “Naz” is heavily populated with expensive growth issues, though they aren’t nearly as pricey as they were a month or two ago; please see our Positioning Recommendations section for more factoids on the intensifying rout.) To reiterate a point from recent weeks, this is behavior decidedly inconsistent with a true bull market—unless it is one that is in the process of entering a bear, or at least serious correction, phase.

A key cause of this performance and sentiment shift is the belief that the Fed is poised to move quickly away from unprecedented stimulation into aggressive tightening. Some respected commentators have even opined that it is on the verge of a deflationary policy mistake.

Like me, Gerard is taking issue with this notion. He believes the Fed and the other central banks are much more concerned about unemployment and wage growth than they are with inflation. (In the Fed’s case, you need to add in the desire to facilitate the green energy transition and bring about social justice.)

In another irony, the growing fears of a deflationary accident and, related to that, a stock market crash, or crashette, actually make the Fed’s job easier. Nothing would eliminate inflation angst faster than a panic in equities. The way things are trending at this minute, that’s not a big stretch. Interestingly, the impregnable FAANGM names, lead by Microsoft and Apple, are suddenly looking more than a tad pregnable.

Value stocks haven’t been exactly stellar performers lately, either (though they did spring to life yesterday). This is a function of Omicron, Fed tightening and also “fiscal cliff” worries. The latter means that the federal government’s unprecedented deficit spending (ex-WWII) is now moderating, leaving the economy to stand on its own feet. Gerard addresses these concerns very persuasively, in my view. As I’ve expressed before, I believe we are on the cusp of an economic surge comparable to what happened in America after WWII ended, when there was widespread trepidation about another depression.

Gerard also sees an economic reacceleration unfolding in 2022 with inflation running hotter than most market participants seem to believe. Again, I think he makes a strong argument for why the consensus, which expects the CPI to be back down around 2% by the end of 2022, is underestimating factors like rising wages and rents. To that I would add another likely spike in energy costs next year with crude oil breaking above $100 and natural gas making another run toward $5 or even higher.

If he and I are right, this is a compelling chance to take advantage of tax-loss selling and economic fears to overweight the beneficiaries of surprisingly robust growth next year. On that upbeat note, it’s time to pass the baton to Mr. Minack, one of the most talented economic and market commentators I follow. (For more information on his consistently insightful missives, please visit his Minack Advisors website to access his popular Downunder Daily.)

Pandemic permitting, expect 2022 to be a year of above-trend growth, rising underlying inflation, and slow policy tightening. This will not be a good setting for zero or low yield assets. I expect moderate equity returns. But the major investment thematic may be rotation from the beneficiaries of the low growth/low rate post-GFC world, to the beneficiaries of a stronger growth/rising rate environment. This note focuses on the macro outlook; the next note will focus on markets.

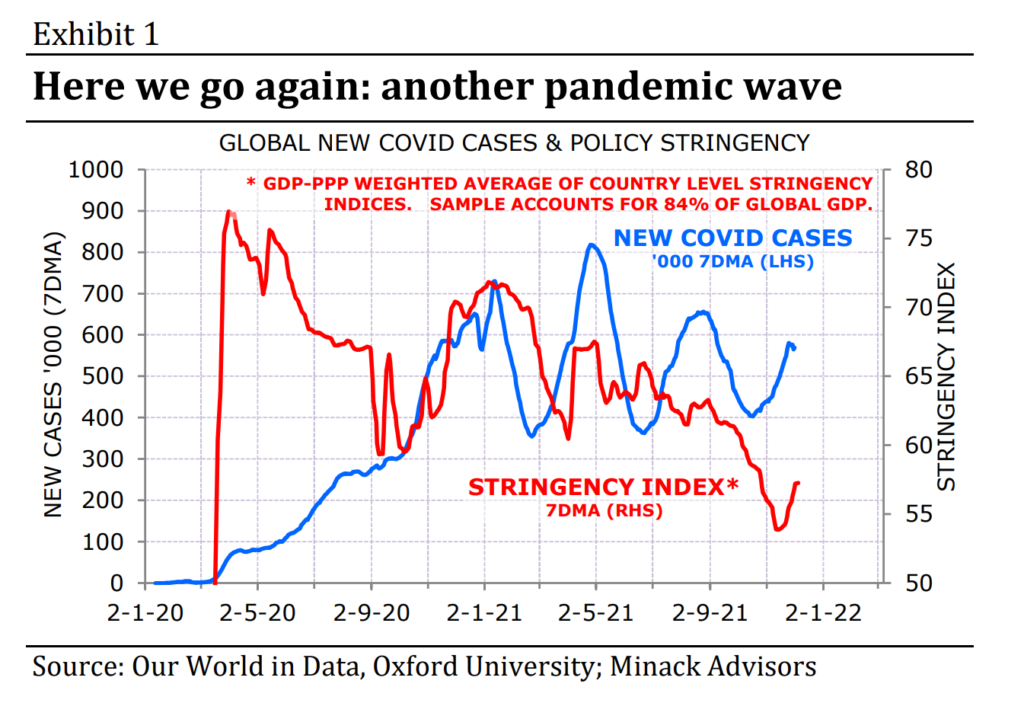

Covid-19 remains a wild card. The good news is that, so far, each new wave of infection has been met with less severe restrictions (Exhibit 1). Tentative early reports suggest Omicron is more contagious but less dangerous than Delta. If that’s confirmed, then it may create some macro bumps through the northern winter but won’t change the strong fundamentals for 2022. However, the risk of a more deadly variant emerging hangs over any macro or market forecast. As does geopolitics.

Assuming – and it is an assumption – that each Covid wave becomes less disruptive, expect above[1]trend growth through 2022, particularly in the developed economies. Policy settings remain extraordinarily easy, most household sectors are cashed up, there is likely to be catch-up spending on services, and there are cyclical and structural reasons to be upbeat on investment spending.

Expansions don’t end spontaneously. Expansions slow or end if economies are hit by external shocks, or if policy is tightened. I can’t rule out a pandemic shock, but policy is unlikely to be a material restraint on growth in 2022. Many disagree, pointing to a looming negative fiscal impulse (the change in the budget balance).

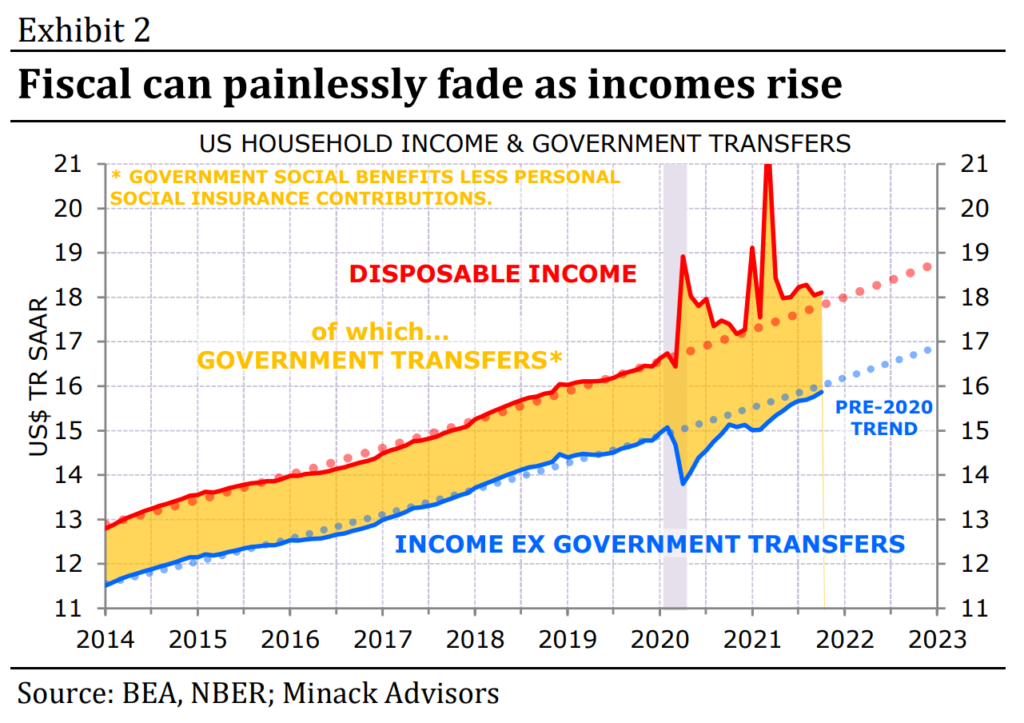

I think there are three reasons to ignore simple fiscal impulse measures. First, a large part of fiscal stimulus was transfer payments to households to compensate for income lost due to restrictions. It is not a policy tightening to reduce those transfer payments as reopening leads to a private income recovery. The handover from government transfers to private income is almost complete in the US: total income and income ex-government transfers are now both near their pre-Covid trend (Exhibit 2).

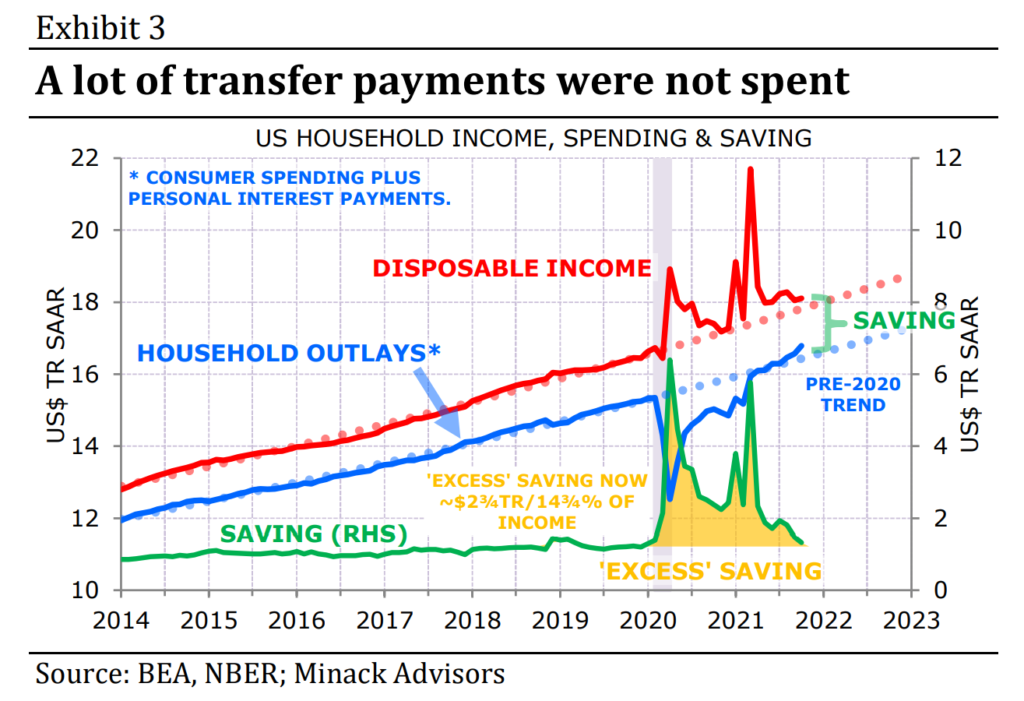

Second, simple fiscal impulse measures assume that all of the increase in public deficits were spent, so reducing the deficit is a GDP drag. That is not the case this time. In most developed economies households saved much of the transfer payments. Consequently, they are now sitting on cash reserves that could fund spending in future (Exhibit 3).

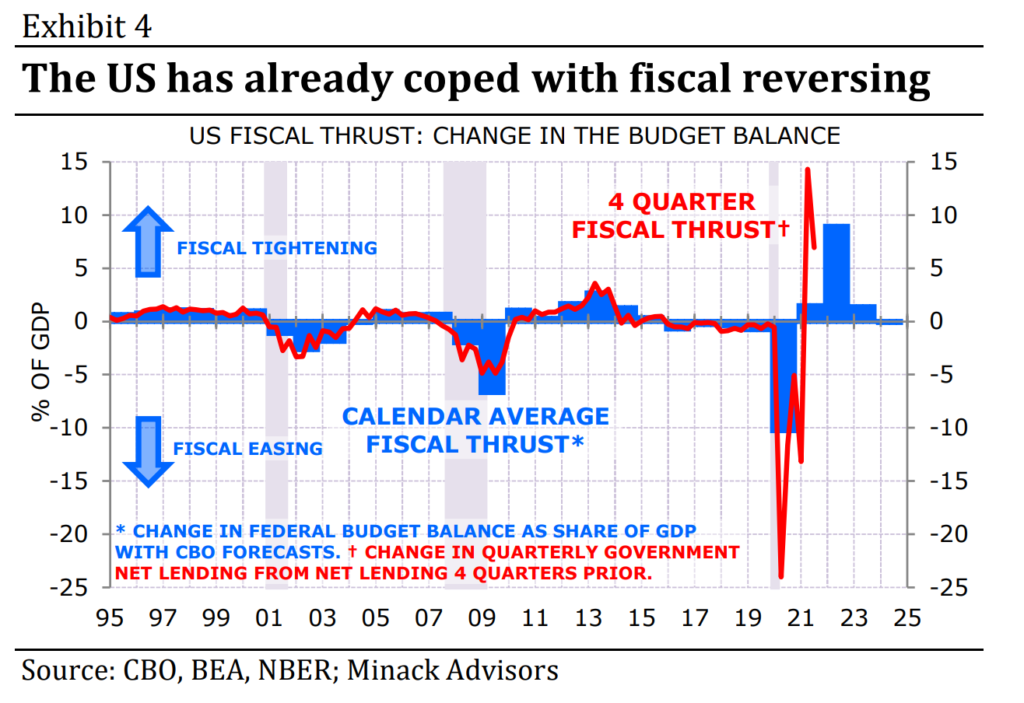

The third reason to not worry about the adverse fiscal impulse in the US is because it has already happened. Calendar year budget aggregates point to a large fiscal tightening in 2022. But the Federal government deficit has already fallen sharply. Net lending peaked at 28.9% of GDP in the June 2020 quarter. By September 2021 quarter it had fallen to 9.7% of GDP. Exhibit 4 shows the four-quarter fiscal impulse is now ostensibly very restrictive. Yet growth has been fine. In short, quarterly data suggest the worst of the fiscal shock has passed.

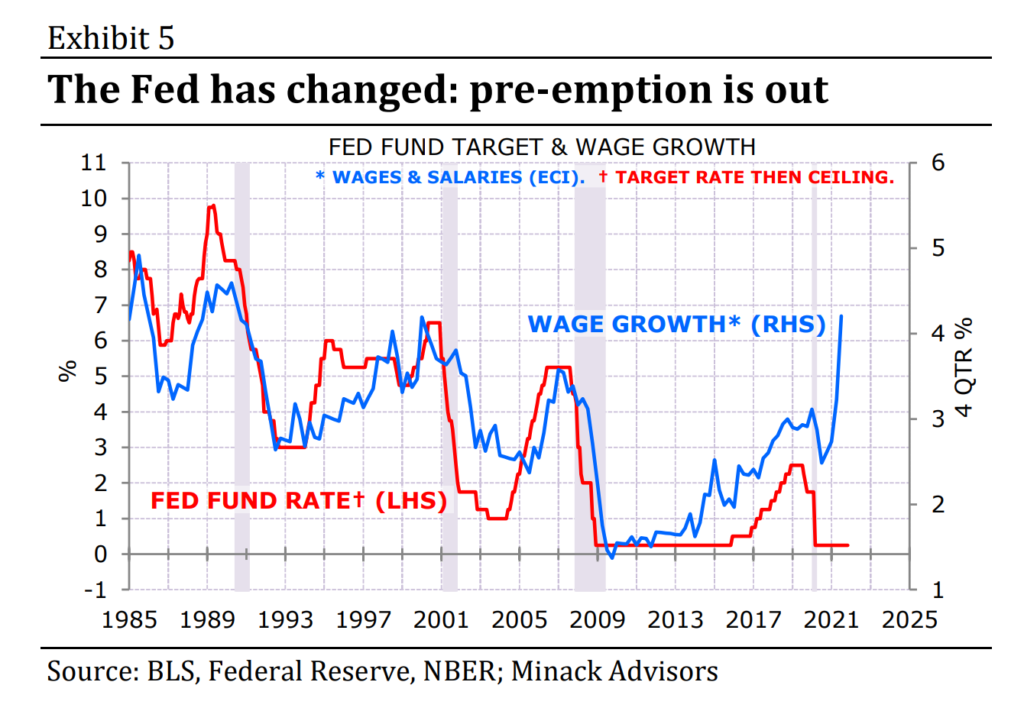

Ultimately what will slow growth is central bank tightening. So it’s crucial to note upfront that central banks have changed. For three decades central banks had a singular focus on inflation and aimed to set policy on a pre-emptive basis. That era is over. Central banks are now as focused on labour markets as inflation and are no longer pre-emptive. Exhibit 5 highlights how different the Fed is behaving in this cycle compared to history.

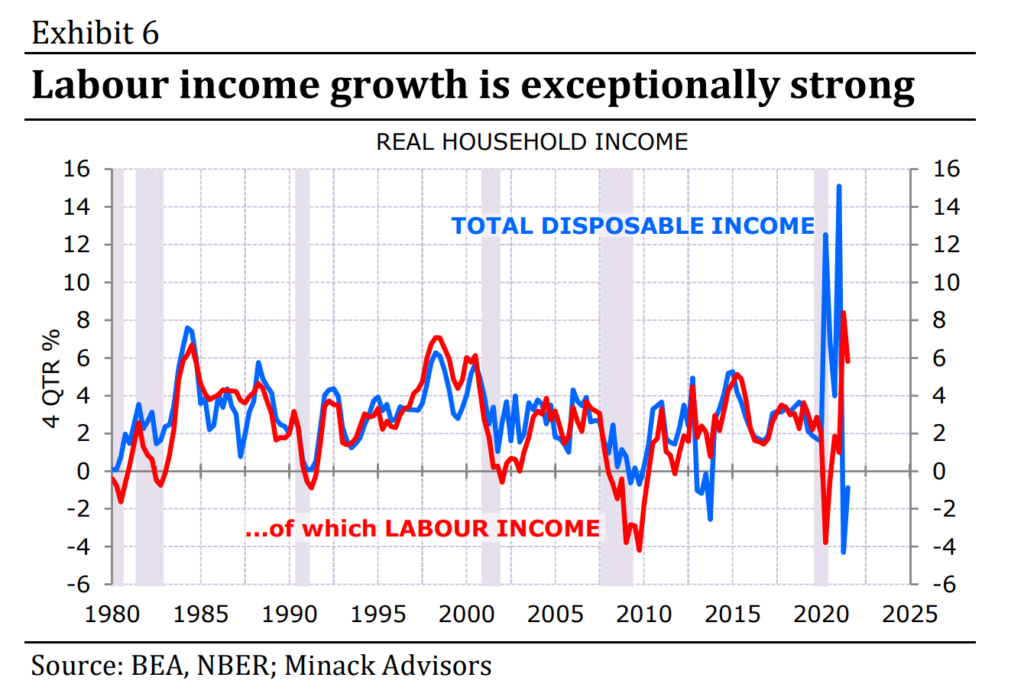

That in turn means that the economy will have more momentum – and more inflation – at the start of this tightening cycle than in any other cycle of the past four decades. In the US, for example, real labour income is now running over 6% above year earlier levels (Exhibit 6). To be fair, this is partly base effects, but the point is that wage and employment growth are both stronger now than at the start of any modern-day tightening cycle.

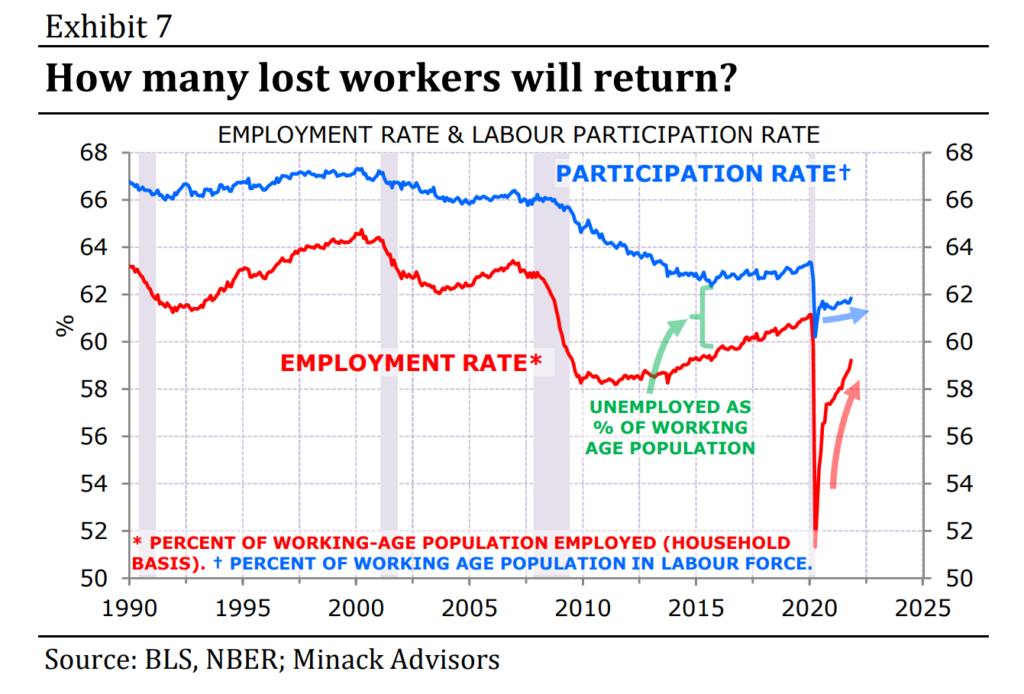

When the Fed starts lifting rates will likely depend on labour market conditions – specifically, the extent to which labour supply recovers (Exhibit 7). If the participation rate were to fully recover its pandemic losses – something looking increasingly unlikely – the Fed may be able to delay tightening until early 2023. On the other hand, if there’s no further increase then a mid-year hike would be on the cards. I am expecting 2-3 moves in the second half of next year, but I’ll change my view if there is a sharp change in labour participation trends.

There’s a faux debate about whether inflation is transitory. The fact is everyone is behaving on the assumption it is. It’s inconceivable that the Fed could maintain a zero fund rate target without believing that 4½% core inflation is transitory. Ditto bond investors buying 10 year Treasury notes on a yield of under 1½% – or equity investors holding stocks on current premium valuations.

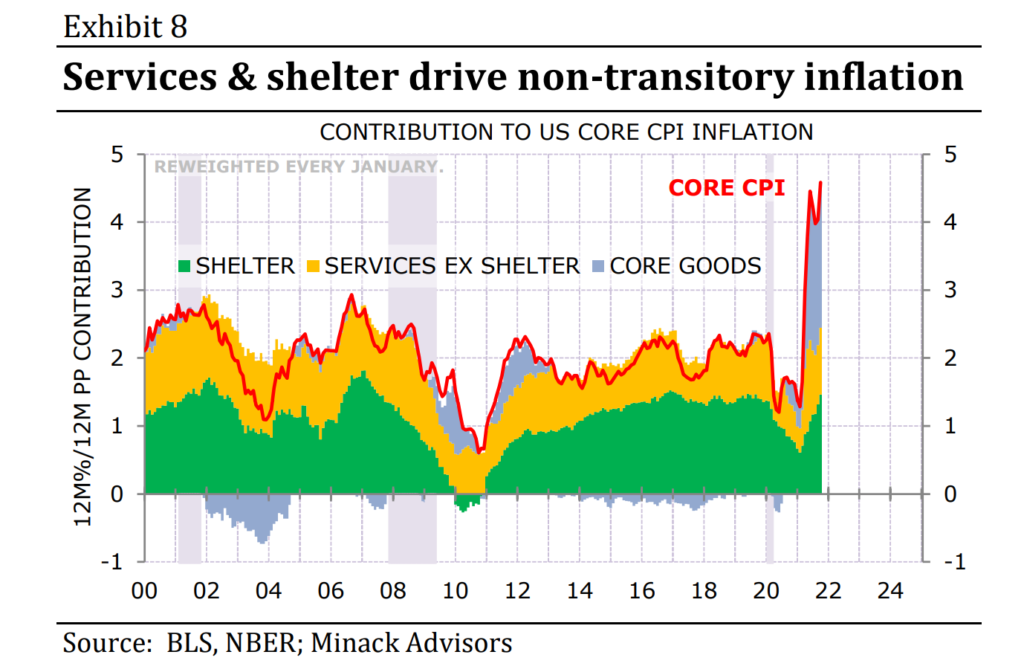

That is why I think the demonstration that inflation is not transitory will be an important influence on markets next year. The key will be an acceleration in shelter and service-sector inflation – both of which are strongly influenced by labour costs. Of course, it may be that the rise in shelter and service inflation will be partly offset by a decline in core goods prices. But just as investors are now dismissing the goods-led rise in core inflation as transitory, I think they would likewise look through any goods-led decline (Exhibit 8). In short, inflation concerns could increase next year even if there’s a (transitory) goods-led dip in the core rate.

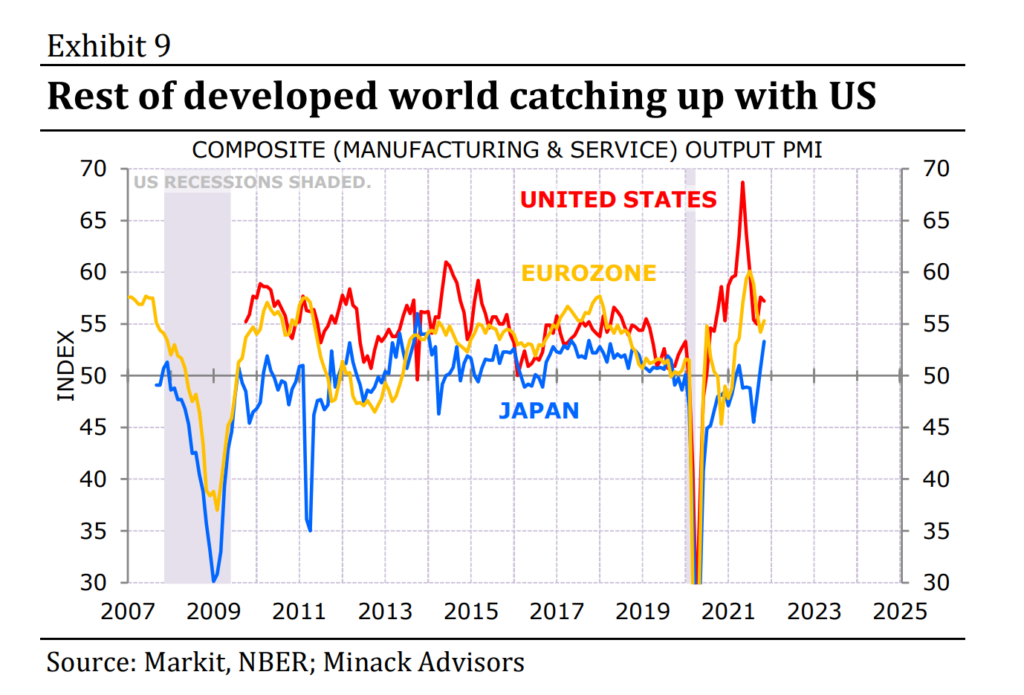

Most major developed economies lagged the US through 2021 (Exhibit 9, which shows composite PMIs). The gap should narrow next year as Europe and Japan have caught up (and overtaken) the US on vaccine roll outs and are undertaking follow-up fiscal stimulus. As in the US, all major developed economy central banks will be unusually slow to tighten in this cycle – improving the prospect of above-trend growth through 2022.

Emerging economies should benefit from the ongoing scramble of goods-producers to catch up with demand, a return of tourism travel, and an easing of domestic pandemic restrictions. I also expect that growth in China will stabilise in coming quarters. But I don’t think the broad picture of global strength would change even if Chinese growth took another step down.

In summary:

I’ll explain what this means for markets next week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.