“GE is now finding it profitable to build manufacturing and service centers in the US rather than overseas, because it is more competitive to do so.”

- General Electric CEO, Jeff Immelt

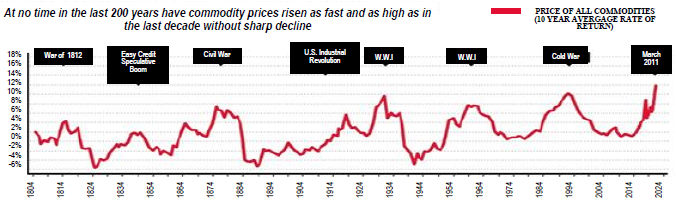

1. Oil prices north of $100 are estimated to be sucking $100 billion of purchasing power out of the US economy. The economic drag from this may undercut demand for other raw materials. Based on the fact that commodities are hitting a threshold where they have peaked multiple times in the last 200 years, a sharp decline is highly plausible.

2. New drilling techniques have caused a totally unanticipated glut of domestic natural gas. Now these same processes are being applied to oil exploration. One consequence is that the mature Permian Basin in west Texas is expected to produce 25% of total US oil output by 2013, up from 17% in 2002.

3. When factoring in undeclared income, China’s wealthiest decile earns 65 times the poorest 10%. Other rapidly developing countries have similar disparities. India, for example, has 6.9% of the world’s billionaires despite producing just 2.1% of global GDP.

4. Once again exposing the dark side of the Fed’s second round of quantitative easing (QE2), the boom in commodity prices caused by this ultra-easy policy is jacking up input prices for corporate America. This may lead to profit margin pressure on both blue chip and smaller firms.

5. Those who are convinced that the Fed’s accumulation of roughly $2 trillion of government securities using printed money is highly inflationary (beyond commodities) should consider Japan’s experience. The Bank of Japan’s balance sheet has ballooned to 24.5% of GDP, versus the Fed’s at 15.8%, yet the land of the rising sun continues to grapple with falling prices.

6. Perhaps indicating an irrational enthusiasm for real estate investment trusts (REITs), assets in dedicated REIT mutual funds and ETFs (exchanged-traded funds) are now at an all-time high. This is despite disappointing operating performance since the real estate bubble popped in 2007 and the widespread dividend cuts or omissions in 2009.

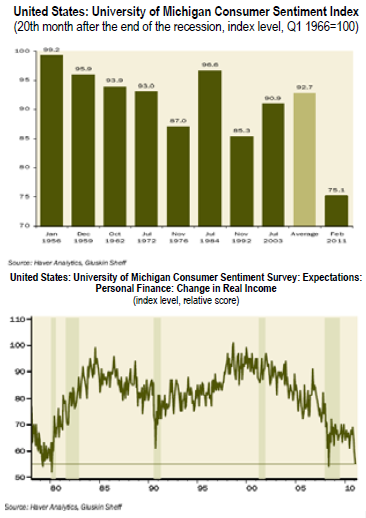

7. Even before oil prices broke above the confidence-busting $100 barrier, consumer sentiment was already disappointing.

8. Due to the earthquake in Japan and political turmoil in the Middle East, the near-term outlook for relief on the oil price front isn’t bright. However, acclaimed inventor and futurist Ray Kurzweil notes that solar power production has been doubling every two years and that at this rate it will provide all of the world’s energy needs by 2030.

9. Much has been made of the US losing its educational edge over China. However, the average person in China spends 6 years of his or her life in classrooms versus 12 in the US.

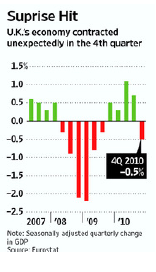

10. The UK continues to be at the vanguard of implementing radical deficit reduction. With Britain’s economy contracting slightly in the final quarter of 2010, those who have been warned of the dangers of this approach no doubt feel vindicated; however, severe weather may have been a major inhibiting factor.

11. One of America’s many underappreciated strengths—with courageous political leadership definitely not among them—is its low-cost railroad system. US rail freight rates are less than half of those in Europe, Japan and India.*

12. Many economists believe that improved productivity is the most important economic driver. Fortunately for the US, in 2010 productivity jumped 3.9%, its fastest rate of increase in eight years.

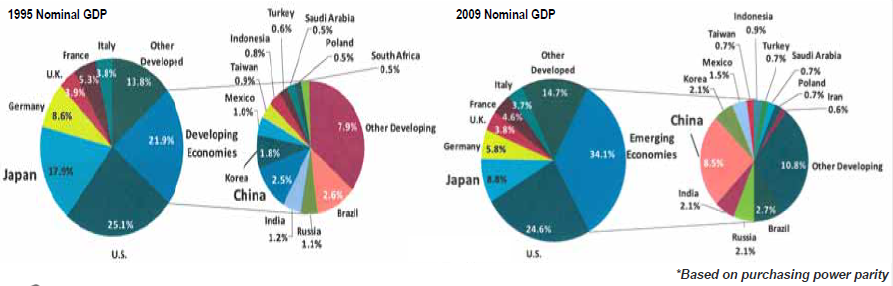

13. Unquestionably, emerging countries have greatly expanded their share of global GDP over the last 15 years. Interestingly, though, the US has roughly held its own over this time frame in contrast to sizable contractions by Japan and Germany. This may indicate that the US economic model is inherently more dynamic and adaptable.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.