"Here’s to the crazy ones, the misfits, the rebels, the troublemakers, the round pegs in the square holes... because the ones who are crazy enough to think that they can change the world, are the ones who do."

- Apple co-founder Steve Jobs

"The time is coming (when) global financial markets stop focusing on how much more medicine they will get (QEs) and instead focus on the fact that it does not work."

- Russell Napier, from the prestigious Asian research firm CLSA

POINTS TO PONDER

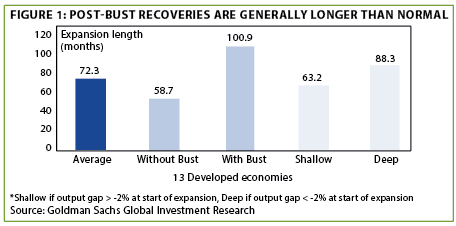

1. Prior EVAs have noted the upside of our underwhelming economic expansion: It may last longer than normal. Per the Goldman Sachs chart below, that appears to be a reasonable conclusion. Evergreen does worry, however, about how well the economy will hold up during the next financial market panic. (See Figure 1.)

2. Corporate America’s profit growth has been lackluster over the last three years, forcing "multiple expansion" (i.e., rising P/E ratios) to drive nearly all of the stock market’s considerable appreciation since 2011. In the third quarter, though, earnings look to have advanced a solid 6% on roughly a 4% revenue gain.

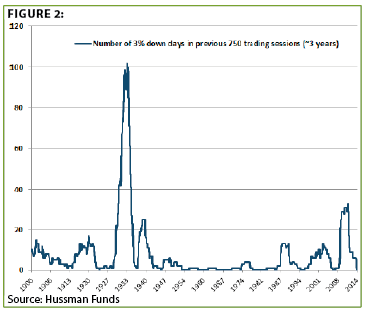

3. In another indication of how volatility has been suppressed, the stock market has not experienced a 3% down day in almost 3 years. Looking back at the last 25 years, such times of tranquility have been rare and tended to lead to eventual eruptions of these events. (See Figure 2.)

4. Zero-Hedge recently looked at the last 4 times stocks have rallied for 23 quarters, or nearly 6 years. As you can see, subsequent results have not been pretty. (See Figure 3.)

5. Global resource prices continue to be pummeled despite the latest desperate monetary blitz by the Bank of Japan, one of the world’s biggest central banks. One commodity that has been particularly nuked is uranium, which has melted down by over 70% since 2008. It has now fallen below production cost for many miners. This reality, combined with the restart of Japan’s nuclear fleet, portends better future price action for U-92.

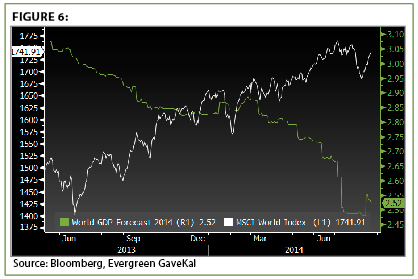

6. Since mid-October, stocks around the world have been on a tear. Those believing this is a function of an improved economic outlook may be basing their outlook on something other than tangible data. (See Figure 4.)

Special Message: In this week’s Evergreen Exchange, we are once again doing something a bit different—in this case, a real opinion exchange. It involves the world’s most valuable corporation, which also happens to be Evergreen’s largest equity holding (and has pretty much been in that role for many years).

Apple has had a tremendous run, and Jeff Eulberg deserves considerable kudos for getting us in it in 2007 and encouraging us to make some timely trims and buy-ups since then. Even though Jeff is our lead hi-tech analyst, the overall Evergeen investment team has certainly had some "spirited internal debate" as to whether or not Apple’s best days are behind the company. One of our bright research associates, Rob Dainard, believes that Apple’s days of dominance are quickly coming to an end, but Jeff and Tyler Hay (another strong Apple advocate over the years) believe the opposite is true.

Before we get into what I hope is an interesting pro/con—or, rather, bull/bear—debate on Apple’s future, I’d like to make a few brief comments on current market conditions (to free up some space for this addition, I’ve shortened this week’s Points to Ponder section).

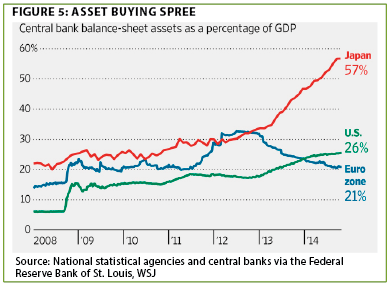

We believe markets were oversold in mid-October and due for a short-term bounce. In fact, Evergreen bought a number of positions, both of a growth and income nature, during the mini-correction. But the bounce has turned into a bound with the most recent impetus being the Bank of Japan’s (BOJ’s) latest iteration of extreme money creation. Additionally, another arm of the Japanese government, the Government Pension Investment Fund, has announced a $120 billion shopping spree on stocks and other "risk" assets. The goal is, as has been the case for the last two years, to crash the yen, raise inflation, elevate asset prices, and stoke economic vitality.

As you can see from the chart below, the BOJ’s money creation as a percentage of its economy makes the Fed look like a piker—no easy feat! Yet, so far, all they’ve been able to create is a weaker yen and rising stock prices. Inflation and growth are, despite the BOJ’s Herculean efforts, thus far, pretty much no-shows. (show WSJ chart from the 11/1 front page art by Jacob Schlesinger, art titled Japan’s Bold Stimulus Jolts Markets, chart titled Asset Buying Binge)

Predictably, the Japanese stock market went postal after this announcement (imagine how much more they would do so if Japan’s massive Postal Savings Fund joins the party!). As noted above, markets around the world also celebrated the news. But should they?

After all, this latest salvo is an embarrassing admission Abenomics, named for Japan’s charismatic prime minister, Shinzo Abe, has failed to deliver. You don’t have to dig too deep to found out why. As the Wall Street Journal pointed out, Mr. Abe’s vaunted "third arrow"—comprehensive and transformational changes to Japan’s paralyzing regulatory system—has never been launched. This is essentially the same situation seen in Europe, where regulatory reform has also been largely missing-in-action, and, frankly, in the US, as well. We believe the sad reality is that as long as central bankers are willing to continue administering monetary amphetamines, politicians are free to do what they do best: talk a lot and accomplish almost nothing.

Another reason investors should be less than elated about this latest "Shock and Abe" move is what it means for deflation. Commodity prices, already mostly in bear markets, fell even further on the announcement. This might seem odd given the additional monumental money multiplication. But there is a logic to it: The yen’s previous shocking shrinkage was a pronounced deflationary development, as noted in several earlier EVAs. This one promises to bring more of the same, particularly pressuring Europe given how directly it competes with Japan in so many industries. Eurozone companies must cut prices or lose customers, putting them in an extremely difficult position and further worsening the battle Europe is already losing with "lowflation" and even deflation.

Lower commodity and import prices are a boon to US consumers. But the plunge in crude might turn the US energy boom into a bust (major oil companies have already put $200 billion of global projects on hold). But the really whopper risk is that China feels compelled to devalue the renminbi to avoid falling even further behind in the currency wars raging across the planet.

If so, it would be a deflation shock that would rock the world. While Evergreen believes that is unlikely, at least for now, we have little doubt that a surprise is lurking out there somewhere that will prevent the two lines below from continuing to diverge.

In other words, caveat celebrator! The Great Disconnect shown above can last only so long.

![]()

IS APPLE TOO BIG TO GROW?

By Tyler Hay, Jeff Eulberg, and Robert Dainard

Question 1: Is Apple too big to grow?

Bull Case

[Jeff Eulberg] With a market capitalization of $634 billon, Apple is the most valuable publicly traded company in the world. Annually, Apple earns over $40 billion. I’ll admit it, on the surface, those numbers appear to be huge hurdles for meaningful future growth. However, unlike other large companies, which found the law of large numbers to be insurmountable, Apple competes in a growing market, has a loyal user base, and extends beyond its core product.

According to a recent study done by Ericsson, smartphone subscriptions are expected to grow from 1.9 billion subscribers in 2013 to over 5.1 billion in 2018. Of the current smartphone market, Apple has just a 12% market share, leaving plenty of room for growth.

Further, with Apple’s core focus placed on providing the highest user experience, it’s not surprising to see Apple’s industry-high retention rate of 76%. Currently, the annual smartphone upgrade cycle is about 25 months and trending shorter. Which, coupled with Apple’s high retention rate, provides a high level of predictably for earnings going forward.

I’ll go into more detail addressing an upcoming question, but the next phase of the smartphone cycle will be the evolution of the eco-system. In this stage, the phone is the essential component for the users’ computing experience. More devices will be connected and the phone will be used to monitor, record, and complete a multitude of daily tasks. As this phase evolves, Apple’s core user provides many new potential streams of income for the company, including, but not limited to, Apple Pay, app store sales, and wearables.

I’ve seen the diversified basket of companies that all equal Apple’s market cap, but to put that into prospective, over 75% of the companies in the S&P 500 have a market cap that is smaller than what Apple is expected to earn in 2015. I hear the concerns about the cost of Apple products, yet the company’s retention rate has remained the industry’s highest. And, at under 11x earnings (net of cash), Apple trades at a valuation that doesn’t require an investor to pay a premium for expected growth. The most incredible element of the Apple story is not the large numbers; it’s the predictability of the large numbers, and the potential for growth beyond those lofty figures.

Bear Case

[Robert Dainard] While Apple’s ecosystem of products and services continues to wow millions of consumers, something important has changed over the last seven years. The company went from having a balanced product mix to making the iPhone its star player, catapulting Apple into the largest company on earth.

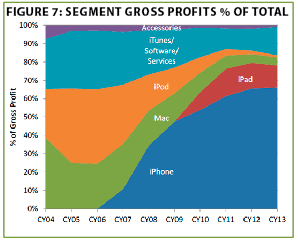

So what’s the problem? Well, the juggernauts profits have become substantially lopsided, as the iPhone now accounts for 63% of the company’s gross profits. We can see below, even the revolutionary iPad it barely makes a dent in profits given the sheer size of the iPhone.

If Apple was in the business of selling luxury shoes this might be less of a concern. Over the years, though, the phone I use to call Grandma has changed much more dramatically than the shoes Grandpa and I wore to our weddings. Because the iPhones profit margins are unlikely to be so fat for years to come (I go into why shortly), Tim Cook will need to find other sources to grow its eco-profit needle.

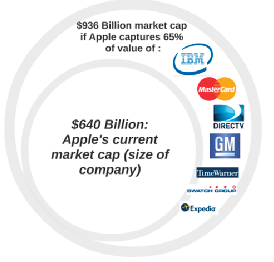

Given the company’s size, this seems like an impossible task but Tim Cook is up to the challenge. His goals for growth include building a stronger presence in enterprise, media, automobile, watches, travel and payments (what an underachiever!). To get a handle on what they’re dealing with, I looked at some of the industry leaders in the areas Apple seeks to dominate, including IBM, General Motors, Direct TV, Time Warner, Swatch, Master Card and Expedia. If we assume Apple executed beyond most expectations and the company captured 65% of the market value of all of these companies’ values today, where would this put them? It would add roughly 46% to the current size of Apple. This is where Apple’s size is a problem. Even if they somehow pulled off this titanic achievement, while maintaining the iPhone’s profit rate, the needle would hardly move.

QUESTION 2: IS APPLE JUST A HARDWARE COMPANY THAT WILL FADE AWAY LIKE SONY?

Bull Case

[Jeff Eulberg] An ecosystem is loosely defined as a complex network or interconnected systems. We may not realize it, but Apple, along with all of its partner developers, built a complex ecosystem that many of us use to better our lives every day.

As our computing transitions to the cloud, more devices will be connected to our smartphones. Our homes will be controlled by our smartphone, our cars will work seamlessly with our devices, and our vital information will be stored by the eco-system that we choose. As this evolution gains steam, the reliability of the hardware working properly with the software becomes increasingly paramount. Essentially, the phone becomes a control center for our life.

For my family and me, the iPhoto sharing capabilities all but guarantees we’ll be in the Apple eco-system for many years to come. This simple offering allows me to regularly see all of my family members as we share pictures easily amongst each other. Others will have different reasons for choosing their eco-system. Google will likely always have a large share of the market due to its lower cost. However, Apple users have consistently been willing to pay a premium price for a superior service, and as our lives become more connected through the IPhone, this willingness will only increase, in my opinion.

The iPhone may not always have the latest feature, but Apple users know if the missing feature provides a better user experience, it will eventually be added. Apple wants to provide me with the greatest user experience possible, and the hardware is merely the portal to their primary offering.

Bear Case

[Robert Dainard] Apple is much more than a hardware company, but the risk of their products becoming commoditized should not be dismissed. In the case of the iPhone, I think this threat is very real. Customers pay up for the hardware for better software, but looking at the iPhone’s current profit margins relative to the iPads (which is really just a big iPhone), margins are a full 100-110% higher. Why is this? Much of it comes down to phone subsidies, which have insulated consumers from the sticker shock of paying $650-$950. The other factor is that Apple has simply had a better product. But today, the competitive landscape looks very different. Over the last seven years Apple has gone from the reality of making a superior phone to the perception that they make a superior phone.

Today, $140 smart phones come in all shapes and sizes and are much stronger competition to a full-priced iPhone than the phones of seven years ago. Apple is worried about this, and we got a sneak peak when the internal company presentation was released thanks to the lawsuit with Samsung. One of the first slides was titled: "Consumers want what we don’t have."

The threats Apple identified were product, price, competitor’s improved ecosystems, and a lack of alignment with telecom partners. Apple isn’t Sony, but many of these risks are likely to get larger over time as technology improves.

QUESTION 3: DOES APPLE'S HIGHER PRICE POINT LEAVE THEM VULNERABLE TO LOWER PRICED COMPETITORS?

Bull Case

[Tyler Hay] A knee jerk response to this question would be to line up products made by Apple and compare their prices with those of their competitors. However, this simple exercise isn’t instructive [constructive?] enough, in my opinion. A Honda costs less than a Mercede: If price was all that mattered there would be fewer German cars on the road.

Instead of talking about price, I’m going to focus on value. Thirteen years ago, Apple launched a visually appealing, easy to use, metal box called the iPod. It didn’t do much besides play music. You still had to carry a cell phone for making calls, a laptop for reading emails or watching movies, a camera for taking pictures, and a wallet for making purchases. Today, they’ve consolidated all of that technology into one device with the launch of the iPhone 6. Other phone makers offer smart phones with cool features, but none have come up with anywhere near as comprehensive suite as Apple. The integration of the different ways Apple can connect your life deserves a monetary premium to other phone or tablet makers. For instance, Apple allows you to take photos on your Apple phone, store it in the Apple cloud, and view it through Apple TV. Piecemealing different technology from competitors can create a great product. No one has been able to do so as efficiently as the folks down in Cupertino.

Apple also provides two other differentiating service offerings that are often overlooked. First, the Apple store offers free technological support for all their devices. Go into any store and you will see a slew of geniuses, as they are called, dispensing free help. As someone who has often had to help my parents with technology, the value of sending them to the Apple store instead is priceless. I’d also point out that Apple gives away updates to the operating system that runs their phones, tablets, and computers. Historically, updates to Microsoft Windows have come at a cost.

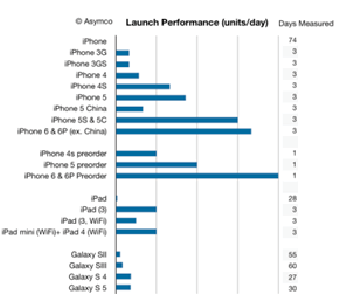

Apple has never been the cheapest product in their respective space. However, have done a fantastic job making their products more and more useful to end-users. Consumers voted with their wallets. The iPhone 6 has coming roaring out of the gates, as you can see.

The idea that Apple products are too expensive may lie ahead but, for now, consumers have no problem paying up.

Bear Case

[Robert Dainard] Many iPhone users will be forever loyal, but many users are not "Apple people." Instead, they just smartly bought into what happened to be both the superior and best option available at the time. But the best option today might not be the superior choice tomorrow.

In Herry Beckwith’s legendary book Selling the Invisible, Beckwith states: "People do not look to make the superior choice, they want to avoid making a bad choice. Experts on decision-making call this behavior "looking for good enough." Five years ago, Apple was so superior that good enough meant still going with Apple, because it stood head and shoulders above the competition. Today, the good enough category is growing rapidly. Reviewing Apple’s internal documents, it’s clear they’ve noticed consumer’s intense focus on price.

For years, the true cost of a phone has been hidden with subsidies. In the end, consumers pay for go unnoticed by many the same way that many consumers do not notice the 20% interest they change on their credit cards. But the landscape of who consumers pay for phones is starting to change (click here to read…. NEED LINK TO WSJ ARTICLE).

But the real reason Apple has continued to largely avoid the "good enough" threat is because they still are perceived as the safer choice. But perception, even with Apple, can change. A recent survey by Santa Clara-based Cheff (a leader in providing students with useful study services) of 1586 college students and 446 high school students found Apple is starting to lose its "cool factor." In fact, Amazon was rated as being "cool" by 72% of students; Google came in with 71%, and Apple at just 64%. (Click here for the survey.) It’s true that Apple is compared to luxury good companies, but what happens when the luxury good is no longer the coolest option? If a change in perception accelerates, the next big thing could be a slowdown in prices.

QUESTION 4: HAS APPLE REACHED A POINT OF MARKET SATURATION WITH CONSUMERS?

Bull Case

[Tyler Hay] There is no denying that Apple is an incredibly popular brand, pushing it to become the largest company in the world by market cap. Some people interpret this as Apple has limited room to grow. A quick look at some of market share metrics suggests that market saturation is more of an anecdotal worry than a factual one. There are two main avenues for Apple to continue their solid track record of growth. First, smartphone usage in the US has room to grow. Currently, 63% of US phone are smartphones, which is lower than adoption rates in China, Germany, UK, and Japan, just to name a few. This should be a tailwind in coming years. Additionally, Apple has barely scratched the surface internationally and currently have lower market share in countries abroad.

Despite being an emerging economy, the Chinese usage of smartphones ranks among the top with an adoption rate of 71%. US smartphone use has room to grow to reach the market penetration seen in China and other Asian countries. Further, expansion within the US is low hanging fruit for Apple as cautious American consumers migrate over from traditional cellular phones.

Globally speaking, the smartphone industry is rapidly growing and evolving. Since the iPhone was first introduced in 2007, global smartphone usage has exploded from 12% in 2008 to almost 40% in 2014. Total smartphone users are expected to increase from 1.4 billion users in 2013 to 2.7 billion users in 2018. In the US, Apple has roughly 40% market share in the smartphone space. Global market share for Apple is much lower at around 12%.

Finally, Apple computer and tablet sales will continue to increase as users migrate to the Apple "ecosystem." Prior to the introduction of the iPhone in 2007, Mac computers struggled to break above 5% of the total PC market share. Since the introduction of the iPhone, users have been attracted to Mac, likely due to the compatibility advantages between their phone, computer, and iPad. The numbers support this thesis. Despite selling their computers at a significantly higher price than competitors, they’ve doubled their PC market share in just seven years.

The market for Apple phones and computers is not saturated. iPhones are incredibly popular in the US but still have room to grow primarily internationally but also domestically. The continued iPhone success will mean Apple has a captive audience to sell other products. The massive following they’ve developed signals consumers’ strong desire for more things Apple.

Bear Case

[Robert Dainard] Apple has to sell both their hardware and software to dent in profits. Because they are a loved brand, it seems likely the company can continue to sell more products but it may not get their software into more hands. But, that does not mean that consumers will want more hardware focused products in the future. In five years time, people likely will want to do more things with less.

The Microsoft surface or a large iPhone replacing the need for an iPad mini are two examples. If is true Apple must begin getting their services into the hands of more consumers without meaningfully disrupting their hardware profits. A very difficult task! So instead of selling more products to the same group of people the company should be looking to expand it’s ecosystem to new groups.

One example of why this is important, if we looked to an American family of four as an example of why ecosystem growth story will be challenging. It seems very likely that most families will choose the "good enough" option for their children instead of paying an extra few thousand dollars every two years for high end Apple products. If the argument today is that the ecosystems of tomorrow will keep consumers anchored into what they already use, their seem little chance that youth will grow up to move towards Apple products as they will already be engrained in the ecosystems of Google and Microsoft. But would they switch to Apple? If the survey mentioned (Apple lost out to Google and Amazon) earlier is any indication of how the youth feel about Apple relative to others, it’s we would have to take the bet that perception that Apple is "cool" not only does not lose ground to others over the next 5-10 years but actually improves. This seems risky and too dependent on fickle consumers who are known to change opinion quickly and without notice.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.