“We cannot solve problems by using the same kind of thinking we used when we created them.”

- Albert Einstein

And now for something (almost) completely different. Those EVA readers out there who keep precise track of our publishing sequence—all six of you—realize this is that time of the month when we produce our "full-length" edition.

But this month, we thought we would create a more visual and less text-based version of our longer issue, somewhat along the lines of the Quarterly Chartbook from our partner firm, GaveKal Dragonomics. (For those of you who receive that, don’t worry—ours is not going to be 60 pages!)

We’ve decided to break this EVA up into two sections, one written by Evergreen’s quantitative whiz, Jeff Dicks, and the other by Yours Truly (aka, Ye Olde Worry Wart). Unsurprisingly, there’s going to be some overlap with our past coverage of these topics, but we still feel there is value in revisiting them, especially based on recent market instability.

Long ago, I heard that the great filmmakers essentially make the same movie over and over—they just switch the characters, locations, and storylines around enough viewers don’t realize the redundancy. On that note, in my section, I’m going to attempt to communicate what feel is a vital message—one that, like an old Hollywood director, I’ve told repeatedly: Despite the recent mini-correction, the US stock market remains extremely pricey. To illustrate this (literally), I will be using visuals that I haven’t used before, unless otherwise noted.

Okay, roll ‘em!!

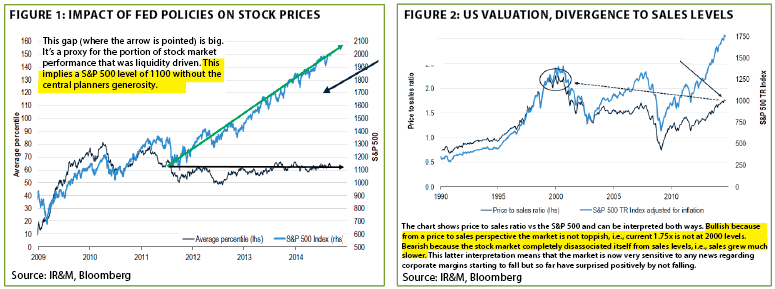

Is that gravity I feel? Courtesy of John Mauldin’s uber-prolific newsletter services, I periodically see the work of Ineichen Research and Management. I’ve viewed enough of their output to realize they are one of many firms that feel investors should stick with the US stock market’s rising trend, until it changes (as one of my ultimate heroes, Charles Gave, consistently notes, this is a classic case of "the prisoner’s dilemma").

So, when I see charts like the two below, which scream caution in my mind, I definitely pay special attention since it is contrary to their official outlook.

Admittedly, past EVAs have included a plethora of price-to-sales (P/S) charts, since the P/S ratio is our favorite valuation measure, but what is different about Figure 2 is that it overlays the stock market’s total return. Also, in their comments Ineichen takes the rosy view that since the P/S ratio isn’t as extended as it was in 2000, the market is not "toppish" (note, their version is based on market capitalization; on page four I will show the same metric on a median basis, which is far more alarming). On the other hand, they note that since the soaring stock market has totally disconnected from the sluggish pace of sales growth, this could be viewed bearishly (ya think?). Their upbeat comment also gives me the chance to repeat how imprudent I believe it is to make comparisons with America’s greatest stock market bubble ever, and conclude that there’s upside back to those insane valuations.

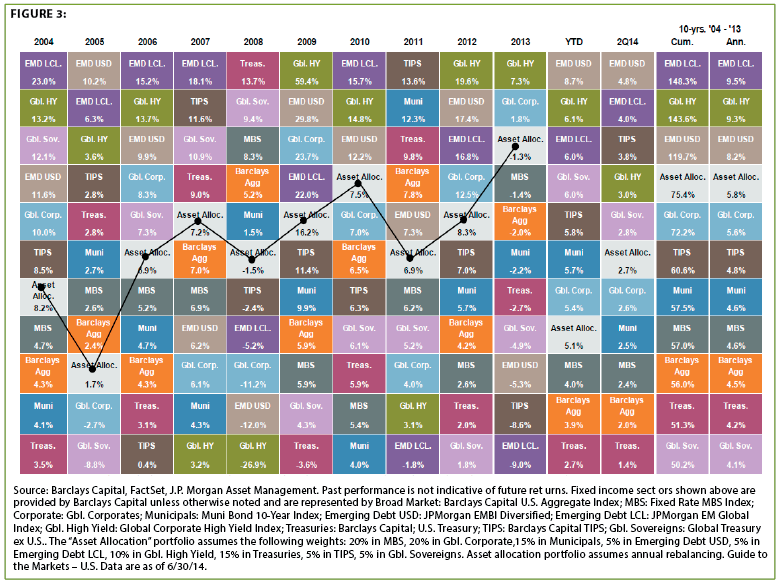

The Investment Team at Evergreen believes, above all else, that asset classes (such as the US stock market and commodities) revert to the mean over time. As you can see from the table below, the S&P 500 has been in the upper half of major asset class returns since 2009, with nary a down year. Previously, the S&P was in the bottom half four out of the five years prior to 2008. This is surprising considering that all of those—save for the cataclysmic year of 2008 itself—were of the bull market variety. Thus, it’s fair to say that the first part of our recent up-cycle was upward mean-reversion to offset the earlier underperformance. However, based on the previous charts, and several more to come, we believe it is safe to say that US shares are now due for some reversion the other direction (hint: the opposite of up).

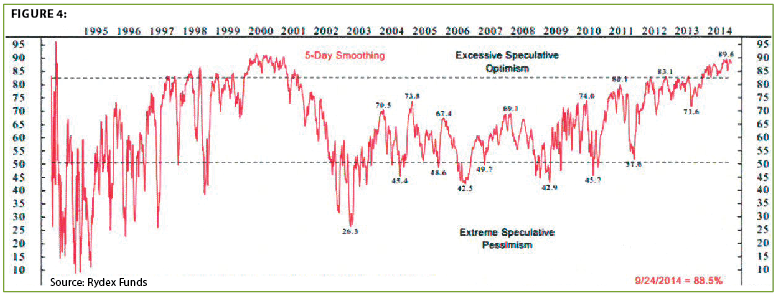

We’ve recently become subscribers to Ned Davis Research (NDR) and I can’t say enough for the quality of their work (listen up, all you investment pros out there—you may want to subscribe as well!). They are equally as prolific at chart production as is the team at GaveKal Dragonmics, and they run some of the best market-related graphics I’ve ever seen. A case in point is the following chart that illustrates something I haven’t seen elsewhere: smoothing sentiment readings using a 5-day moving average. The advantage of this is that you don’t get the typical rapid, extreme, and irritating, swings from bullish to bearish that is typical of most sentiment charts. Accordingly, it provides a much better sense of the long-term trend. As you can see, we are really in nose-bleed territory in that regard, essentially at early 2000 levels. Can you say "Wow!"? (See Figure 4)

To prove my point about the quality of NDR charts, we’re going to stay with them for awhile. These will continue to impress upon you what rarefied market territory we’ve been in lately. Again, the idea is to express this with some visuals that I don’t believe you’ve seen (at least I haven’t).

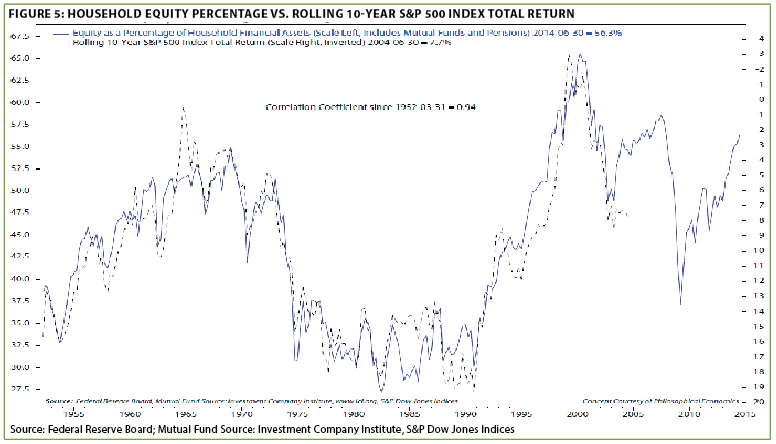

Next up is their analysis of US household stock ownership as a percentage of financial assets. As many EVA readers know, I have taken strong issue with the idea that we are in the midst of a "hated-on" bull market (maybe distrusted, for good reason, but certainly not hated). What’s different about this graphic is that NDR goes back to the early 1950s and looks at 10-year forward market returns relative to the level of stock ownership. As you can, see low stock allocations foreshadow high future returns and, as is the case today, elevated equity holdings lead to sub-par long-term gains. (Note, the return scale on the right is inverted.)

The correlation has been remarkable, as Ned Davis himself pointed out in the accompanying text with this chart. It totally makes sense but it’s another of those historically-proven measures that almost every market strategist has ignored, usually on the basis that the trend is still up (a view even NDR has espoused).

Another unique visual that tells the same story is the below NDR chart on the percentage of stocks trading above $100. Of course, a stock isn’t over-priced merely because it trades north of the century mark but this method has sounded some great warning sirens in the past.

Clearly, it was early this time, probably because there are so many mid- and small-cap companies that have broken into triple digits due to the dizzying run-up by those styles in recent years. It’s just another way of saying that the non-blue chips are where the extreme overvaluation has been during this up-phase.

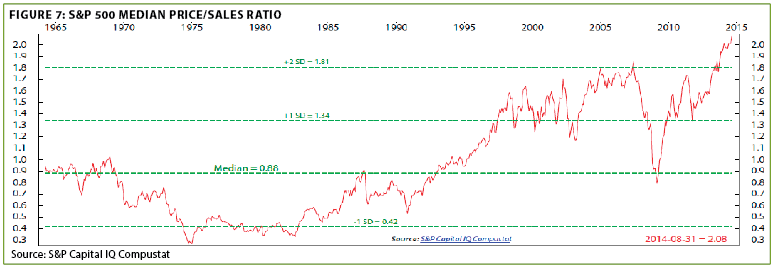

On that score, I cannot help but re-run a chart I’ve shown before: the median price-to-sales ratio. The "median" aspect means that it is much more of a measure of the typical publicly-traded stock, without undue influence from mega-cap issues. There is simply no question it is uncharted territory for this purest of all valuation metrics (meaning, no distortion from accounting gimmicks and the profit margin cycle). Again, I continue to be amazed at how few investment professionals reflect upon the implications of this graphic, maybe because it is so hard to rationalize away.

Moving away from NDR, one of Evergreen’s favorite daily sources of incisive insights is Jones’ Trading Chief Market Strategist, Mike O’Rourke, author of The Closing Print (I would highly recommend all serious investors sign up for his free service). His chart on the next page is a combination of the S&P 500 and the dollar versus other stock markets priced in non-dollar currencies. As Mike says, "In essence, at that time (the 2000 peak) $1 worth of S&P 500 bought you the most ever it could of global assets." Clearly, we are basically right back up to that apex. (See Figure 8)

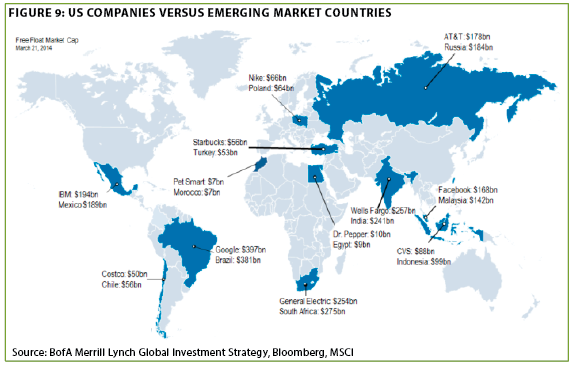

Along similar lines, the man I refer to as Evergreen’s human search engine, Rob Dainard, came across the following map of the world with some interesting market capitalization figures. Unquestionably, Corporate America remains the envy of the planet when it comes to profitability. However, the fact that IBM’s market value is greater than that of all Mexican stocks, or that AT&T’s market cap exceeds the entire Russian stock market, speak volumes about how richly-valued US equities are versus the rest of the world.

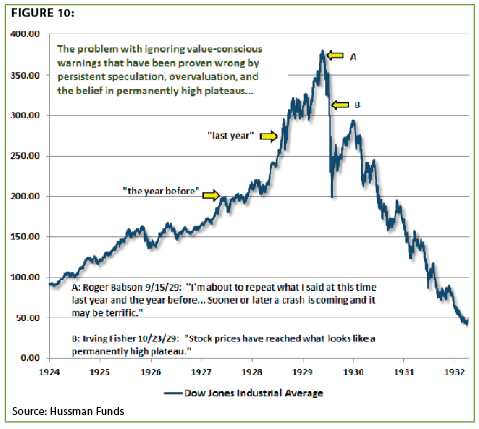

My last chart is courtesy of John Hussman and it concerns a man--long departed from this vale of tears--who has become one of my new posthumous icons, Roger Babson. Some of you may have heard of the school he founded in Massachusetts, Babson College. His Babson’s Reports was also one of America’s first investment newsletters, which is another reason I admire him. Additionally, his "Ten Commandments of Investing" (shown on page 11 of this EVA), are classic—and very much worth re-reading based on current market circumstances.

One of the reasons I have such an affinity for this obviously talented individual comes from a series of speeches he gave back in the late-1920s to the National Business Conference. His first was in September, 1927, when he warned about over-priced stocks. The next year, with the market up almost 40% from his last talk, he warned again. On September 15th, 1929, with stocks up another 35%, he was, somewhat incongruously, invited back to speak again. After admitting that he had been wrong over the prior two years, he didn’t waver: "I’m about to repeat what I said at this time last year and the year before…sooner or later a crash is coming and it may be terrific." By contrast, America’s most famous economist of the time, Irving Fisher, was assuring investors of a new, perpetually elevated, era. (Hmmm, I think I’ve read the same kind of reasoning a lot over the last year or so.) (See Figure 10)

As you can see, the market nearly doubled from when Mr. Babson began to caution about its inflated condition (since stocks are "only" up about 50% from when I started calling for a correction, this makes me feel much better!). Yet, despite some furious counter-trend rallies, it wasn’t long before stocks round-tripped back to where he started waving red flags, eventually tumbling far below that point.

Please don’t think that I’m predicting a replay of that terrifying market era, or of the NASDAQ’s 78% vaporization after the dotcom bubble, or even the nearly 60% collapse following the housing blow-up six years ago. However, a brief item caught my eye the other day as relayed by the ever-vigilant David Rosenberg that slams home how our current situation is straight out of the theater of the absurd. To wit: "Major déjà vu. I am hearing more and more talk about a QE4 as the Fed is forced to react to the stock market correction." To validate David’s intelligence-gathering skills, a senior Fed official on Monday brought up QEQ (that would be QE Quatro!)

Friends, readers, and countrymen, the S&P 500 was down less than 4% from its all-time high when David wrote those words! Even on Wednesday, when the Dow was down 460 points, this has been nothing more than a garden-variety correction. If such a minor jiggle can cause Wall Street to call for another monetary fix from the Fed, the foundation of this market is even more fragile than I thought. And that’s a pretty scary thought!

Now, let’s consider what the talented Mr. Dicks has to say...

THE TALE OF TWO: A BIFURCATED US ECONOMY

By Jeff Dicks

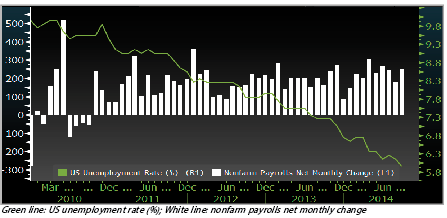

By most broad measures, the US economy has made significant strides since the financial crisis. We have seen the unemployment rate drop from 10% to just under 6% today. And so far in 2014, this trend has continued to gain momentumm with over 200,000 jobs added on average per month.

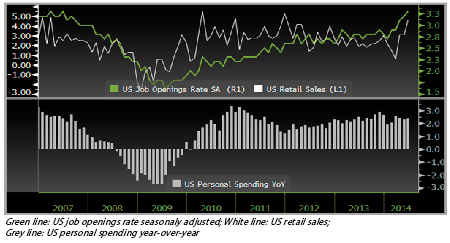

Along these lines, job openings have also made new highs this year, climbing by 230,000 from July to August. This should further help personal spending and retail sales.

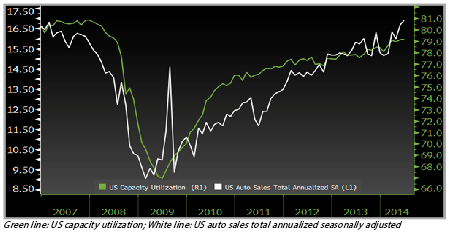

A stronger labor market has certainly been a function of an improved manufacturing sector, which is now operating close to the peak in 2007 (based on capacity utilization). The strength in manufacturing can be seen through US auto sales, which recently exceeded the 2007 high (sales closely track production).

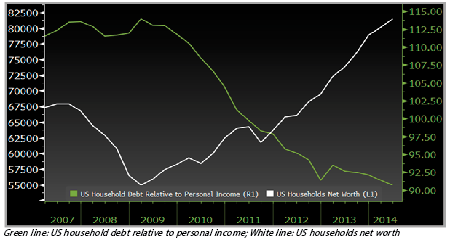

In addition, US households have meaningfully mended their balance sheets, and household wealth just made all-time highs. These are both very positive developments for the consumer, and future spending ability. Moreover, the recent crash in oil prices should produce at least a $70 billion windfall for American households.

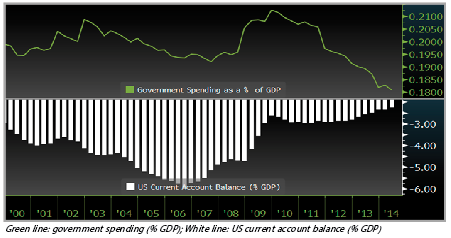

Lastly, government spending as a percentage of GDP has dropped meaningfully, as has our current account deficit. Both of these developments put the US in a stronger financial position, despite the utter failure of Congress to rationalize entitlement programs (portending a future disaster if not resolved, in our view).

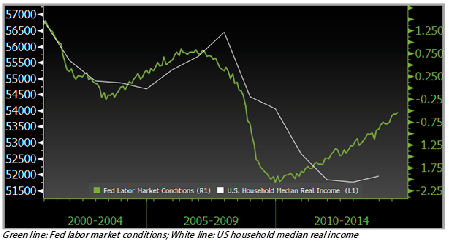

However, upon closer analysis, there’s more than meets the eye at first glance. In terms of the labor market, while we have seen significant improvement over the last few years, real wages are still down significantly over the last 15 years. This has caused labor market conditions to be far below the previous peak.

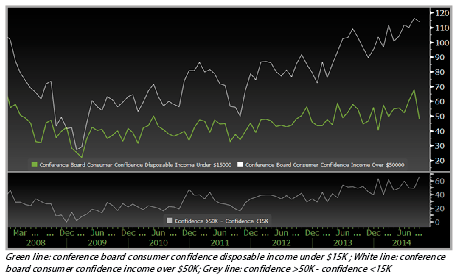

Without increasing real wages, the consumer will continue to be strapped, particularly Americans who are "asset-lite". The result is a divergence between consumer confidence in low- and high-income workers, as seen below.

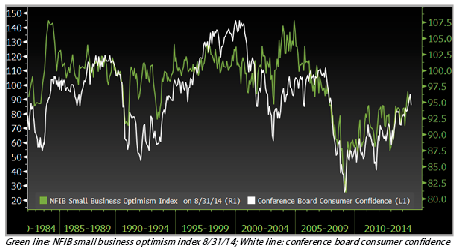

Overall, consumer confidence is still materially below previous peaks and much lower than would be expected this late in a recovery. In addition, while small business confidence is improving, it’s still far below where it was prior to the financial crisis.

This suggests that the typical American consumer is not buying into the asset-driven prosperity, such as it is, generated by the Fed’s monetary experiment. In fact, we believe this is a key reason that spending has remained anemic despite huge increases in household wealth.

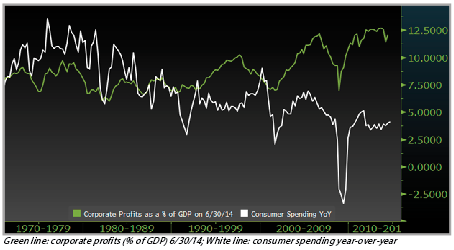

Here, we can see the same divide between consumer spending and corporate profits as a percentage of GDP. This illustrates corporate profits have not been re-distributed to the consumer—a byproduct of declining real wages. We continue to believe that it will be tough to attain higher growth when hard-working Americans continue to take home a smaller piece of the overall pie.

And, while the manufacturing sector has shown signs of improvement, both total construction spending and new and existing home sales remain significantly below their pre-recession peaks. This is a key reason why this recovery has produced the lowest rebound in GDP growth on record.

In fact, here is how real GDP has grown following the last five recessions. As you can see, this is not exactly a booming US economy! The green line below shows that real GDP has grown a measly 11.5% since the end of the last recession. Simply put, the current recovery has been a serious under-achiever.

In summary, we believe the Fed’s reliance on extreme monetary measures to catalyze the US economy has had mixed results, at best. The good news is that the usual pre-conditions for an economic downturn are nowhere in sight. One of the most reliable of these has been an inverted yield curve (i.e., when short-term interest rates rise above longer rates).

While that is comforting, Evergreen believes that the next domestic recession will not be foreshadowed by an inverted yield curve in our new post-bubble environment. For example, Japan and Europe have had multiple recessions in recent years without their yield curves inverting (as did the US in the 1930s). Rather, we believe a panic in the financial markets could be the trigger for the next contraction. This is why we expect the Fed to respond very aggressively—likely launching QE 4—should the current market reversal turn into a rout.

As Dave discussed in his section, QE Quatro may not be in our distant future but, possibly, only a 15-20% market swoon away!

Roger Babson’s Ten Commandments on Investing

1. Keep speculation and investments separated

2. Don’t be fooled by a name.

3. Be wary of new promotions.

4. Give due consideration to market ability.

5. Don’t buy without proper facts.

6. Safeguard purchases through diversification.

7. Don’t try to diversify by buying different securities of the same company.

8. Small companies should be carefully scrutinized.

9. Buy adequate security, not super abundance.

10. Choose your dealer and buy outright (i.e., don’t buy on margin.)

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.