"I recently tried to refinance my mortgage and was unsuccessful in doing so. I think the tightness of mortgage credit—lending—is still probably excessive."

- Ben Bernanke, speaking at a conference earlier this week

"There are cracks emerging in the Teflon tape that is the S&P 500."

- Mike O’Rourke, author of The Closing Print and Chief Market Strategist at JonesTrading

Choosing sides. Let’s call a spade a spade: For the last two years, I’ve been wrong about the US stock market. After the rambunctious rally that followed the nearly 20% sell-off in August of 2011, I began to believe a correction was due. For a time in 2012, my angst was somewhat validated as the market came close to a 10% pullback. But since then, it’s been a joyride up the proverbial hockey stick.

On the other hand, my esteemed colleague, Anatole Kaletsky, at our partner firm GaveKal Dragonomics, has stayed resolutely, and correctly, bullish. Consequently, his views merit your close attention. In early September, Anatole concisely outlined his reasons why he remains a bull in his essay "The Case for a Structural Bull Market," which we are running as this month’s Guest EVA.

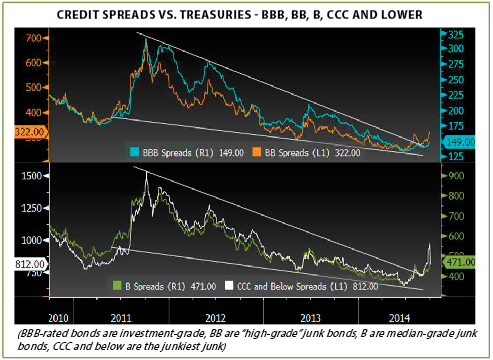

In fairness to Anatole, this was written a month ago, and there have been some less than supportive developments since then. Louis Gave—who, along with his father, Charles Gave, and Anatole, founded GaveKal—recently gave a talk where he noted that global economic trends are deteriorating. He specifically cited that overall growth is sputtering (again!), a number of stock markets around the world are wobbling, the liquidity situation is worsening as QE3 ends, and credit spreads are widening, despite the partial snap-back by CCC-rated bonds over the last couple of days.

To our way of thinking, one of the most worrisome developments is the sudden and dramatic change in credit spreads (the yield differential between non-government and treasury bonds). Several EVAs this year have indicated that this has typically been the ultimate canary in the coal mine. As you can see from the charts below, there appears to be a major trend change underway.

This clear reversal in spreads, combined with the other factors Louis mentioned, especially the end of the stock market amphetamine drip known as QE3, might make this October a lot like the one seared in my memory from 27 years ago. And that leads me to an interesting point…

In preparation for running Anatole’s piece, I’ve read it over multiple times and marked up several sections. In doing so, it dawned on me that our outlooks are similar in a number of ways, including our shared concern that this October could be a reprise of 1987. He and I have both written on this a few times this year and, he’s previously speculated that we might see the huge run-up that occurred in 1987 prior to the crash. (Many forget that, despite the fourth-quarter meltdown, the S&P finished up 2% in that wild and wooly year.)

Yet, thus far, we haven’t seen anything like the vertical ascent that occured 27 years ago, and it’s getting awfully late in the game for that to happen this year. (Maybe 2013’s 30% rise, along with a 9% add-on, through this August, were equivalent to the thrilling 40% surge in 1987 prior to the implosion.) Moreover, you may have noticed even the mighty S&P has started to show signs of fatigue. Of course, stocks may just be taking a breather before resuming their seemingly never-ending sprint, but there is some noticeable below-the-surface erosion unfolding, particularly a shrinking list of stocks participating on the upside.

Naturally, I’ve got rather significant quibbles with Anatole’s views, especially that we are in a new long-term, or as he calls it, structural bull market. While financial markets have been ebullient since 2008, that has certainly not been the case with global economies, including everyone’s new favorite country, the US of A (which was largely viewed as a has-been just three years ago). Anatole also believes the global economy is now poised to bolt head; in my opinion, it better hurry and I’m not holding my breath. Even the world’s alleged growth-driver, the US, continues to in an erratic expansion.

Additionally, Anatole asks a series of profound and provocative questions on pages 3 and 4. As he notes, most of these will need to have positive answers to justify his "structural break-out" view. To me, that sure seems like a whole lot of things that need to break the right way, and soon, to keep this market at such vertiginous valuations. Long-term, I do agree with Anatole that America will cope with most of these challenges. But in the near-term, I continue to believe a crisis is needed to force our paralyzed policymakers into serious reform mode.

As always, though, I try to give EVA readers both sides of an argument, even when I strongly believe mine is closer to reality. But just so you don’t think I’m waffling, I’ve added a short essay from Charles Gave at the end. As you will read, he’s much less sanguine about a happy ending to the era of central banks manipulating financial markets. It’s time for investors to decide which scenario is most probable. Pick carefully, very carefully.

THE CASE FOR A STRUCTURAL BULL MARKET

Anatole Kaletsky

It’s almost three months since I recommended a ‘Buy in May’ strategy for US equities. At roughly the same time Charles reiterated his ‘balanced portfolio’ call for a long position in US equities hedged with long-dated US treasuries. Since then both equities and bonds have performed well. The S&P 500 has risen almost 6% while 30-year US Treasury bonds have gained about 3% in price (as of July 25, 2014).

The question now is whether both these asset classes can continue to rise together. Gavekal’s last Quarterly Strategy Chartbook and a clutch of our recent Daily notes have emphasized the risks that a disappointing economic performance and an eventual monetary tightening could pose to stretched equity valuations.

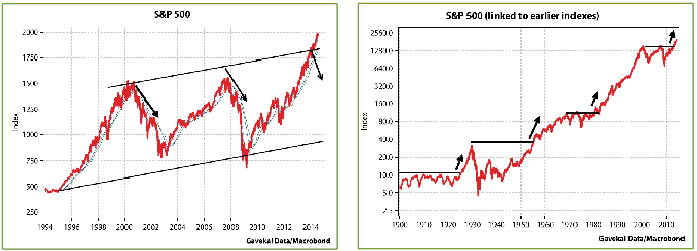

At our London and New York seminars, and at dozens of client meetings across the US, Europe and Brazil over the last couple of months, I’ve taken a different tack. After a five-year bull run in equities which has broken out decisively to set new highs on all the US indexes, I’ve suggested that investors should be asking not whether they should take profits, but whether the equity market gains of 2009-13 were merely the prelude to a longer term upswing in equities that could continue for the rest of this decade, and perhaps beyond.

The end of a bounce or the beginning of a breakout?

For the benefit of readers unable to make our seminars or client presentations–and with apologies to those already bored with my Panglossian views–I’ve decided to set out my bullish arguments in a series of Gavekal reports. I begin today by posing the key question that every investor must ask after an uninterrupted five-year bull market: Are equities at the end of a five-year cyclical bounce or are they at the start of a 15-year structural breakout?

The question intimately concerns all investors, whether they allocate assets strategically between equities, bonds and cash, or manage individual asset classes and have to choose between adding risk to boost returns or taking profits to preserve capital.

History suggests two directly contradictory answers, illustrated in the charts below. On a 20-year view it is time to take profits because the market has reached the top of an established trading channel, which means the emphasis should be on capital preservation. The 120-year view, by contrast, suggests investors should stay long following a sustained breakout from a decade-long trading range; the opportunities for capital growth are just beginning.

The bullish breakout view is becoming more plausible. But to prove it right will require a structural improvement in economic conditions over the coming decade, relative to the bear-market period from 2000-13. Even to suggest such a possibility would have seemed ridiculous a few years ago, since everybody ‘knew’ that the post-2008 ‘new normal’ would be much weaker and more unstable than the previous era. To support their structural pessimism, bears cited phenomena including deflation, excess leverage, monetary manipulation, government deficits, demographics, income inequality, underinvestment, collapsing productivity growth and the exhaustion of natural resources.

Searching for new structural improvements

How then could anyone believe in a structurally bullish story? Yet someone must have believed it, since global stock markets have kept going up. One likely answer is that the structural headwinds have been fully recognised, and that some have gradually subsided or even turned into tailwinds that portend stronger and more sustainable global conditions. As time goes by, it is becoming increasingly apparent that each of the bearish structural arguments can be countered by an equal and opposite question pointing the other way:

To decide between the cyclical bounce and the structural breakout stories, investors must form a view on questions of this kind. The problem is that nobody can be sure of the answers, since structural trends can take many years to emerge and decades to play out. And by the time the answers on technology, energy, demographics or capital misallocation are completely clear it will be too late to profit. There is, however, one thing we can confidently say today about the tug-of-war between structural obstacles and opportunities: financial and business opinions about these long term structural questions will be strongly influenced by whether medium term cyclical economic conditions are improving or getting worse.

Cyclical conditions determine structural views

As an example, consider the way majority opinion has shifted on the last two issues–energy and productivity growth. In 2011, when investors and businessmen believed almost unanimously that the world was running out of energy, shale oil had already been discovered and fracking technology already had a long track record. Yet the promise of these discoveries and technologies was ignored because the world economy seemed to be stuttering on the brink of a double-dip recession. For similar reasons, the opportunities from robotics and other new technologies were disregarded, as investors assumed that a cyclical slowdown in productivity growth was a permanent structural consequence of technological exhaustion, as argued by Robert Gordon and other productivity pessimists.

This experience suggests that, whatever the ultimate truth about the balance between structural opportunities and obstacles, the market’s view will be strongly influenced by what is happening to the global economic cycle. This brings me to the other questions I plan to address:

HOW TO GAME A RIGGED MARKET

Charles Gave

Markets are on alert in a week that could see more great insights from the gods of central banking on high. Investors seem a little spooked with the MSCI emerging markets index off 4% in the last eight trading days, while currency volatility has picked up as the US dollar has strengthened. And yet despite these minor ructions, there remains a deeper sense of calm. It is the sort of quiescence born of insiders’ knowledge that the nature of financial markets has changed, and in a way that favors them.

In the past, money sat at the center of the economic system. When money was created, it moved slowly through the real economy toward the fringes where assets were located. Too much money caused a bull market; too little and we got the reverse. Now asset prices sit at the center of the system and money is relegated to the periphery. Every right-minded person knows the main role of a central bank is to create sufficient money to stop asset prices going down, because if this can be achieved then a little of that elixir may just flow into the real economy and create growth.

Indeed, talk to a central banker, preferably a retired one, and they will admit that they have one long-term goal which is to stop asset prices from going down the following week. This is because so much debt is linked to these assets that should prices start to fall then the mother of all margin calls would materialize. Most central bankers have read Irving Fisher’s great 1934 tome The Debt Deflation Theory of Great Depressions and they don’t want something similar starting on their watch.

To achieve the desired results, central banks have bought bucket loads of government bonds, on the simple idea that if the anchor rate was pulled down, then all rates would follow including the discount rate used to value long-dated assets, and thus the value of said assets would go up. In the case of equities, the particular traits of investors in these markets has meant that central bankers could play a more indirect role.

Today, most money managers can be described as having five core beliefs, or at least operating principles: (i) it is not certain that central banks can control asset prices forever and it could end in tears; (ii) I am one of the few investors smart enough to understand this; (iii) most other money managers are dumb enough (especially the indexers) to believe that central banks really can control asset prices; (iv) so despite being very smart, and knowing better, I have to keep buying shares, but (v) because I am very smart, I will see ahead of the others when the time is right to get out, and in any case I have some very good risk control systems which will kick in and prevent me suffering too huge a loss.

The astute reader will have recognized a sophisticated version of the prisoner’s dilemma taken from game theory; i.e., the system continues to work so long as nobody breaks the rules. However, to escape the dilemma in good shape, it is necessary to be the first one to break the rules.

The implicit reasoning in this assumption is that if the investor cannot be first out then they can at least be second or third. However, such a stance rests upon two key assumptions that are less than rock solid.

In short, it may make sense to stay invested, but we have reached a point where protection against an untidy denouement to the present market phase should be built into the construction of a portfolio. It is not enough to rely on a protection that will be executed in response to price signals. In constructing what Nassim Taleb would call a "non-fragile" portfolio my simple recommendation would be to remain long US bonds and short -dated dim sum bonds. Those wanting to maintain an equity component to the portfolio should stick with Asian and US shares. It should be noted that a 50/50 portfolio of long-dated US treasuries and short-dated dim sum bonds has outperformed the S&P 500 since November 2013 by a solid 4%, and with much lower volatility. When a very defensive portfolio starts to outperform the best stock market in the world, it is seldom good news.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.