"Deficit spending is simply a scheme for the hidden confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights."

-ALAN GREENSPAN, 1966

It may come as somewhat of a shock to even casual EVA readers, who would have had a hard time missing my repeated endorsements of gold, that I really don’t like it as an investment vehicle. Instead of being a gold bug, the truth is, gold really bugs me.

The reasons for my antipathy are manifold, but here’s just a few for starters: It’s a bet against the dollar, which implicitly means a bet against the US; its true value is almost impossible to ascertain; it has been confiscated by the US government in the past and could be again; holding it physically is problematic and relying on a counter-party can be dangerous (as Lehman showed). But the truly huge drawback, in my view, is that it doesn’t pay you a cent to hold it.

As almost all EVA readers are aware, I like cash flow. Even if a company retains most of the cash it generates from operations, I’m still a fan because the reinvestment of that income stream builds value over time, at least with competent management at the helm. Even more important in this regard is the fact that so many Evergreen clients rely on their portfolio to provide them with livable cash flow. In effect, they now get their paychecks from the investments we manage for them, which is truly an awesome responsibility.

Thus, gold and its pale cousin, silver, are not natural fits with our investment process. Yet, over the last seven years, I’ve mostly recommended gold and it, in turn, has been mostly good to our clients. Of course, over the past two years, the action in bullion has been anything but bullish, as it has tumbled 30% from its zenith in September 2011. Despite this pathetic performance since then, we’ve stuck with it, and the closely-related investments in miners, for one crucial reason: It protects our myriad income investments from their worst nightmare of runaway inflation.

Having been a young broker during the late 1970s and early 1980s, I remember what double-digit inflation did to bonds—and stocks for that matter. Although we don’t see a repeat on the horizon, the unparalleled amount of money fabrication and debt monetization seen since the Great Recession has the potential to eventually generate even higher inflation than we saw during the disco decade. On the other hand, growth-retarding US economic policies, including the debilitating QEs, could enfeeble the US for years, leaving it in a long-term Japan-like funk.

Singapore-based Grant Williams, who I’ve often mentioned over the last year, writes one of the more entertaining and illuminating newsletters, Things That Make You Go Hmmmm, and believe me, I’ve gone "hmmm" numerous times upon reading his essays! Happily, Grant will be visiting Evergreen’s Bellevue offices next week, giving my team and me a chance to spend hours debriefing a man who has become one of the most widely-read financial scribes in the world.

This month’s guest EVA is a condensed version of one of his recent issues that I found especially interesting. It focuses on the tremendous demand for physical gold that has occurred in Asia since the price broke in April, and the almost inexplicable disconnect with the severe weakness in "paper" gold (ETFs and futures contracts). Grant makes a convincing case that gold really hasn’t lost its glitter and that its appeal as "central bank insurance" remains intact.

It also dawned on me that another ramification of Grant’s analysis is that US investors should have part of their income holdings domiciled in Asia. Among other reasons for this conclusion is that alternate iteration of the old golden rule: Whoever has the gold, makes the rules!

NEVER THE TWAIN

Grant Willaims, Things That Make You Go Hmmm

The mere mention of the Silk Road evokes a very different time and place, pre-Amazon.com, when trade was conducted face-to-face and merchants travelled on horseback and foot the breadth of continents to find buyers for their merchandise, returning with goods in exchange.

The Silk Road was, according to Wikipedia:

... a historical network of interlinking trade routes across the Afro-Eurasian landmass that connected East, South, and

Western Asia with the Mediterranean and European world, as well as parts of North and East Africa. The Silk Road includes

routes through Syria, Turkey, Iran, Turkmenistan, Uzbekistan, Kyrgyzstan, Pakistan and China. Extending some 4,000 miles

from Europe to Asia, uniting West and East in trade, it took its name from the Chinese silk which, from the days of the Han

Dynasty (206 BC – 220 AD), was bought and sold along its length.

Wikipedia again:

The central Asian sections of the trade routes were expanded around 114 BC by the Han dynasty, largely through the

missions and explorations of Zhang Qian, but earlier trade routes across the continents already existed.

Trade on the Silk Road was a significant factor in the development of the civilizations of China, the Indian subcontinent,

Persia, Europe and Arabia. Though silk was certainly the major trade item from China, many other goods were traded, and various technologies, religions and philosophies, as well as the bubonic plague (the "Black Death"), also traveled along the Silk Routes.

Silk and technology, good. Bubonic plague, not so good; but that sort of thing can happen when you open trade routes across continents, I guess.

The Silk Road endured through centuries of human expansion as Chinese emperors, Persian kings, and even Alexander the Great traveled the route, looking to open new markets for trade; but it wasn’t until the first century BC that a discernible Silk Road (or rather a network of Silk Roads) was established by the Yuezhi and Xiongnu peoples of China, who forged a complex network of trade routes (and an even more complex set of diplomatic relations) with both India and the Western World.

However, it wasn’t until the Romans conquered Egypt in 30 BC that trade and communication among China, India, the Middle East, Africa, and of course Europe exploded in both breadth and depth to levels theretofore unimaginable.

Yes, theretofore. I said it. And yes, it IS a word. No, it’s not 1789; I just like the sound of it.

Despite the inconvenience of frequent wars, the Silk Roads became the axis along which trade between the continents blossomed; and inevitably, as if to prove Mark Twain’s assertion that history may not repeat itself but certainly rhymes, it was cheap Chinese-made goods that found the most favour with the wealthy inhabitants of the Roman Empire in the West, and specifically Chinese hand-spun silks, which the early Romans initially believed grew on trees (like money does in 2013) but which they later discovered were woven from thread created by the larvae of moths. Imagine the guy in the fancy toga who made THAT discovery: "Exspecta ... ex QUO?" (or, in English: "Wait ... it comes from WHAT?")

Now this is where things get interesting.

The Roman Senate tried desperately and, as it turned out, unsuccessfully to prohibit the wearing of silk on — wait for it — both economic and moral grounds.

The real grounds, of course, were economic; but by cloaking its reasons in morality, the Senate wished to appeal to the higher sensibilities of the citizens of Rome in order to deceive them into doing something that was against their better interests persuade them to play ball of their own volition. Of course, appealing on moral grounds to the same group of people who invented the orgy was a strategy flawed in the extreme; but early paparazzi coverage of celebrity lifestyles was patchy at best, and with the invention of the doorstep hundreds of years away, doorstepping was a verb that early Latin students never had to conjugate.

It is in those economic grounds for trying to stop the inflow of silk into Rome that we may find lessons, as historical parallels once again demonstrate the benefits of studying the past.

In his "Declarations" Seneca the Younger laid out the establishment’s moralistic case against silk:

I can see clothes of silk, if materials that do not hide the body, nor even one’s decency, can be called clothes…. Wretched flocks of maids labour so that the adulteress may be visible through her thin dress, so that her husband has no more acquaintance than any outsider or foreigner with his wife’s body.

Nice try, establishment. The real reason?

Gold.

Of course.

The insatiable lust for silk amongst Roman high society sent huge outflows of gold to Chinese coffers, and that was something the authorities simply couldn’t allow to continue. Why? Because gold was money. Gold was wealth.

Gold was power.

The merchants of the East knew it and coveted gold for all of those reasons. The ruling class in the West knew it and tried to stop the transfer of gold from their own vaults into those of the Indian and Chinese merchant classes. But the citizens of the Roman Empire, growing ever more decadent by the day, were happy to swap their gold for the luxuriant fabric.

Money for "bling".

Attitudes toward gold persisted through the centuries as citizens of the East grew accustomed to wealth confiscation, regular defaults by their rulers, inflation, hyperinflation, and the need to have their wealth held outside the banking system in a form that was durable, portable, divisible, convenient, consistent, limited in its availability, and widely accepted through history. Wealth was something to be accumulated and passed on to future generations to provide security — not something to squander on holiday villas, speed canoes to waterski behind, and souped-up chariots.

It was once that way in the West, too; but like the Romans two thousand years ago, the modern inhabitants of the Western World grew decadent and preferred to spend their wealth on trophy purchases or use it as collateral in order to engage in speculative leverage.

Growth was converted to wealth, wealth was exchanged for goods, and when wealth expansion subsided, there was always credit, which masqueraded quite nicely as growth in the eyes of people only too willing to confuse one for the other in order that the party continue.

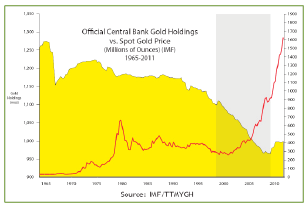

When Nixon ended the gold standard in August 1971, he sounded the all-clear to really get the credit party started, and as you can see from the chart below (which will be familiar to regular readers, as I have shoved it under your noses several times already), the credit providers in the USA found a public willing to indulge itself with Borgia-like ferocity:

The differing attitudes to gold, Western vs Eastern, have been ingrained through centuries of human development; and they have been making themselves abundantly clear in recent times as physical gold moves inexorably from West to East.

I won't go into the recent disconnect between "the Gold Price" and "the Price of Gold" again, as I've written and spoken about it extensively in recent months; but the insatiable demand for physical gold amidst a dramatic sell-off in paper has, I suspect, paved the way for some real problems in the coming weeks and months; and those problems have begun to manifest themselves, bizarrely enough, in the very country that in recent months has topped the buying charts for physical gold.

In the all-important second quarter of 2013, the two biggest buyers of gold in the world were two of the countries at the Eastern extremities of the old Silk Roads — China and India — and it is through journeying to India that we can now learn lessons about the future from the study of the past.

Indian demand for physical gold swamped even Chinese demand in Q2 2013, as Indians stocked up on the monetary metal not only in the form of jewelry ahead of the traditional wedding season but also in investment form: coins and bars. All the while, their national currency, the rupee, was disintegrating before their eyes.

In the absence of monetary mettle, Indians demanded monetary metal.

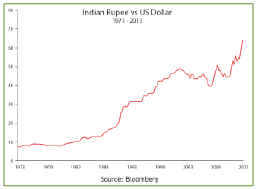

Between May 1st and August 20th, the rupee fell 20% against the US dollar, and whilst that move may not have resonated with most Westerners, it certainly did with India's richest man:

(UK Guardian): India's richest man is down to his last $17.5bn (£ 11.2bn), after plunging value of the rupee wiped out a quarter of his fortune, in dollar terms.

Mukesh Ambani, the chairman of Reliance Industries, which operates the world's largest oil refineries, has lost $5.6bn of his personal wealth since 1 May, according to the Bloomberg Billionaires index.

His fortune took a further hit on Thursday, as India's currency hit fresh lows, adding to the sense of panic in emerging markets. Developing economies, excluding China, have seen an outflow of $81bn in emergency reserves since early May, as central banks try to prop up their currencies. That's a very real hit, but Indians are used to moves like these in their currency, though the trend over the last 40 years has been largely a one-way ticket to a weaker rupee.

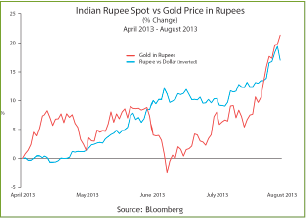

However, that chart tells only half the story. To really understand why Indians covet gold so much, let’s take a look at another chart, this time showing the recent performance of the rupee AND gold:

Et voilà! Since April, gold has strengthened 20% in rupees whilst the currency has depreciated by a similar amount vs the US dollar.

Purchasing power protection in action, folks. Just one of the beauties of owning gold.

Naturally, the Indian government is concerned that its citizens — conditioned over the centuries to understand exactly why owning gold is important — are exchanging their rupees for gold in droves, because their activity is exacerbating the slide in the rupee. So...

Cue capital controls:

(The Times of India, Aug 14 2013): India has banned imports of gold coins and medallions as part of steps to curb its current account deficit, Arvind Mayaram, economic affairs secretary, said on Wednesday, after total gold imports picked up again in July.

The federal government will take more steps to stabilize the rupee as and when required, he said, adding the current measures were not permanent in nature ...

As drastic as the government’s action may seem, it is just the latest in a long line of (futile) attempts to curb Indian citizens’ ability to own gold:

(Reuters): Following are the measures taken by the central bank and the government in 2013:

Jan 21 - The government raises the gold import duty by 2% to 6%.

Jan 22 - The government more than doubles the duty on raw gold to 5%.

Jan 30 - Finance Minister P. Chidambaram says there are no plans for additional taxes or curbs on gold imports.

Feb 1 - The Reserve Bank of India (RBI) plans to introduce three or four gold-linked products in the next few months.

Feb 6 - The RBI says it would consider imposing value and quantity restrictions on gold imports by banks.

Feb 14 - The central bank relaxes rules on gold deposit schemes offered by banks by allowing lenders to offer the products with shorter maturities.

Feb 20 - The Trade Ministry recommends suspending cheaper gold jewellery imports from Thailand.

Feb 28 - India keeps its gold import duty unchanged in its annual national budget, defying industry expectations.

Feb 28 - India proposes a transaction tax of 0.01% on nonagricultural futures contracts, including for precious metals.

March 1 - The Finance Minister appeals to people not to buy so much gold.

March 18 - The Reserve Bank of India says it is examining banks that sell gold coins and wealth management products to identify "systemic issues", with a view to closing any legal loopholes.

April 2 - The Finance Ministry suggests it is unlikely to raise the import tax on gold further to avoid smuggling and would instead introduce inflation-indexed instruments.

May 3 - The RBI restricts the import of gold on a consignment basis by banks.

June 3 - The Finance Minister says India cannot afford high levels of gold imports and may review its import policy

June 5 - India hikes the gold import duty by a third, to 8%.

June 21 - Reliance Capital halts gold sales and investments in its gold-backed funds.

June 24 - India’s biggest jewellers’ association asks members to stop selling gold bars and coins, about 35% of their business.

July 10 - India’s jewellers announce they might continue a voluntary ban on sales of gold coins and bars for six months.

July 22 - The RBI moves to tighten gold imports again, making them dependent on export volumes, but offers relief to domestic sellers by lifting restrictions on credit deals.

July 31 - India hopes to contain gold imports well below the 845 tonnes that were shipped last year, the Finance Minister says.

Aug 13 - India hikes the import duty on gold for a third time in 2013, to 10%. Duties for silver and platinum are also increased to 10%. The customs duty on gold ore bars, ore, and concentrate are increased to 8% from 6%.

Aug 14 - India turns the screws on gold buying again, banning imports of coins and medallions and making domestic buyers pay cash.

Get the feeling that in the middle of the world’s largest democracy, a small group of people doesn’t want a large group of people owning something?

Now, naturally, Indian citizens, seeing their government’s desire to restrict their ownership of gold, simply stepped up their pursuit of gold dramatically:

(Mineweb): Even as gold retailers reel under new RBI curbs, gold smugglers appear to be gaining ground in India. The seizure of smuggled gold has surged 365% in the April to June quarter of this financial year, thanks to the incessant restrictions on the precious metal. Margins for smuggled gold have also jumped, beating other smuggled items like sandal wood and ketamine drugs....

Revenue authorities had said smuggling could rise to over 150% over last year. However, the increase in import duty in June, from 6% to 8% as well, as the Reserve Bank of India’s (RBI’s) recent measures to curb gold imports have precipitated smuggling.

As I said previously, people in the East fundamentally understand the value of owning gold — and not being able to get it just makes them want it more.

Fortunately (for inhabitants of the subcontinent, at least), as the fervor to own gold in India increased, it happened to coincide with the paper-driven sell-off in the West, as traders and weak hands were taken in by the pummeling of COMEX futures and liquidated positions in ETFs.

Richard Dyson laid it out perfectly:

(UK Daily Telegraph): Gold market commentators say that, while ETFs account for just 6pc of the overall demand for the precious metal, ETF investors’ ability to buy and sell with ease has a dramatic impact on price. The supply chain for gold bars, coins and jewellery, on the other hand, is long and more complex, the argument goes, so that even though these markets generate greater total demand — something like 70pc — it takes longer to filter through.

So western investors in effect presented consumers in India, China and other smaller, Asian countries with a buying opportunity unseen for years.

Bingo!

That is exactly what has happened.

Physical gold has been sucked into the East and into very strong hands — the kinds of hands that don’t let go of it easily. Certainly not as easily as those in the West who were scared out by a 20% correction.

But the level of the frantic desire to accumulate physical gold here in Asia and especially in India has surprised even me (almost); and this week a whole new level of light was shed on just how frantic that desire has been by a data point involving, of all places, the UK and Switzerland:

(FT): UK gold exports to Switzerland, the hub of the gold refining industry, leapt to 798 tonnes in the first six months of the year, up from just 83 tonnes in the first half of 2012, according to data from Eurostat, the European Union’s statistics office.

Now, at this point I can hear you asking, "What the heck does this have to do with Asian gold demand?" Well, allow me (or rather, the FT) to continue:

(FT): Large-scale selling by investors triggered a 26 per cent slide in gold prices from the start of the year to a near three-year low of $1,180 a troy ounce in June.

The price fall has stimulated a huge increase in demand in Asia, particularly China, whose gold association reported a 54 per cent increase in demand in the first half of the year.

Matthew Turner, precious metals analyst at Macquarie, said the rise in gold exports had closely tracked outflows of the metal from exchange-traded funds, a popular investment product which helped to popularize gold when they were launched a decade ago.

"If investors don’t want the gold it has to go somewhere else," said Mr Turner of Macquarie. "The Chinese are simply willing to pay more for it."

The large-scale shift of gold out of western trading hubs towards Asia has led to a spike in business for traders and refiners.

The London Bullion Market Association said that the daily cleared trading volume on the London market by its members hit a 12-year high of 900 tonnes — worth $39bn — in June on the back of "strong physical demand, particularly from China and India".

At the same time Swiss gold refiners, such as Metalor, Pamp, Valcambi and Argor- Heraeus, have enjoyed a boom, melting down large 400oz bars from London vaults and reprocessing them into smaller products that are preferred by Asian buyers.

"The Swiss are running three or four shifts to keep the refineries going non-stop. They’re throwing bodies at it," said one senior gold trader.

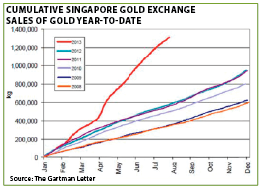

The story is the same in Dubai, where refiners have 90-day backlogs in producing the small bars and coins so craved by Asian buyers, while here in Singapore there has been an absolutely extraordinary explosion in gold demand as the Freeport storage facility is deluged with not only Eastern investors but also savvy Westerners looking to move their gold to a jurisdiction they feel won’t come under the kind of pressure being exerted in India.

Dennis Gartman published a fascinating chart this week that demonstrates just how crazy demand for gold has been here in Singapore in 2013:

Devaluation of your currency is a constant threat in Asia, as is the other peril that gold provides such good protection against: inflation. And this week the Wall Street Journal offered an insight into just how terrified Asians are of inflation, when it examined the cost of dying:

(WSJ): Deep in China’s spirit world, an inflation crisis is brewing that would give central bankers chills.

For hundreds of years, Chinese have burned stacks of so-called "ghost money" for their ancestors to help ensure their comfort in the afterlife. The fake bills resemble a gaudier version of Monopoly money, emblazoned with the beatific-looking image of the Emperor of the Underworld.

Traditionally, paper money burned in China came in small denominations of fives or tens. But more recent generations of money printers have grown less restrained. The value of the biggest bills has risen in the past few decades from the millions and, more recently, the billions.

The reason: Even Hong Kong’s dead try to keep up with the Joneses, and their living relatives believe that they need more and more fake bucks to pay for high-cost indulgences like condos and iPads.

This year, on the narrow Hong Kong streets that are filled with shops that specialize in offerings for the dead, there appeared a foot-long, rainbow-colored $1 trillion bill. "What we have right now is hyperinflation," says University of Hong Kong economist Timothy Hau. "It’s like operating in Zimbabwe."

"Inflation is everywhere, so of course it happens in the underworld too," says Li Yinkwan, 42. The $1 trillion bill is the most popular note in her shop, she says, "because it allows the ghosts to buy many things, such as a fancy car and a big house."

Still, she said that there is also a place for burning smaller-value bills. "The ghosts need spare change to buy daily necessities, too," she says, such as clothes and food. On a recent Friday, all the trillion-dollar bills in her shop and the shops next door were sold out. "I’m sorry," Ms. Li said to one customer. "There are still some $100 billion notes left."

OK ... you can read the entire article on page 23 here, and I’m belabouring the point now. However, it is SO important to understand it properly.

Here in the East, there is a desire to own gold that utterly transcends anything commonly understood in the West. It is hard-coded into the DNA of several billion people, who, acting together, will provide a strengthening bid for gold for decades to come. Those people are getting wealthier, and with their increased wealth comes both an increased need to protect it and an increased desire to hold it in a form they have come to trust. And THAT, dear reader, is gold.

It’s simple.

The exodus of gold from the UK to Asia via Switzerland is no accident and no one-off. The surge in imports of gold into China through Hong Kong is, likewise, not a flash in the pan. Indians’ desire to own bullion, jewelry, coins — anything golden — is not going away. Trust me.

It is time to put aside Western attitudes to gold and gain an understanding of how it is viewed by the real buyers — those in the East. Those who buy physical metal to hold and to bequeath — not those who sit at home in front of their computers, buying and selling paper claims on a metal most of them have never seen up close — are going to determine the future path of the metal.

In the late 1970s, Asia was a poor continent. and though its appetite for gold was undiminished, its ability to purchase it was restricted.

Through the 1980s and 1990s, central banks were continuous sellers of gold (chart above), which helped keep a lid on the price, but now ... NOW, we have the makings of a perfect storm.

All of these factors will undoubtedly conspire to make the next six months (and beyond) a lot less painful for holders of gold than the last six were - a shift that has already begun to take shape

As Roger Waters once wrote:

Who is the strongest?

Who is the best?

Who holds the aces?

The East

Or the West?

Those 'aces', in the form of physical gold, are moving inexorably East, and with them go prosperity, influence, strength, and, eventually, power.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.