“But no single country…is well prepared. And even if one country is doing the right things to protect itself, it has to be a global thing. We need to cooperate globally on epidemic preparedness and prevention in the same way we are cooperating globally to stop people from getting nuclear weapons.”

– Bill Gates in 2017 interview

One of the most poignant global pandemics in recent memory has been the unexpected outbreak of the coronavirus in China’s Hubei province. The spread and impact of the disease even changed this week’s plan to release the next edition of Bubble 3.0, instead favoring some pertinent commentary from Gavekal’s Arthur Kroeber on the “Wuhan Flu”. (Don’t fret though, we will be publishing our next version of Bubble 3.0 on buy-backs next week). As of Friday morning, the virus had infected a reported 31,400 individuals with over 630 confirmed deaths according to CNN. While the virus has largely been contained to China up to this point, worries of a truly global crisis have sparked never-before-seen measures aimed at slowing the spread of the disease.

It is also hard to have confidence in the reports on infections and fatalities by the Chinese government – a regime with a long track record of disseminating misinformation. There are several unofficial sources asserting that the numbers are far higher than what’s been reported. Bloomberg even stated in a recent article that “One set of researchers from the University of Hong Kong estimated in the Lancet, a medical journal, that there were more than 75,000 cases in Wuhan as of January 25th, with cases doubling every 6.4 days.” While this and similar reports could be exaggerated, the fact of the matter is that almost everyone is guessing at this point.

Case in point, the world seemingly received some much-needed good news on Wednesday when Chinese and UK media reported separate breakthroughs in the development of an effective drug to treat and combat the virus. Sky News even reported that a vaccine coming out of Imperial College London “is thought to be able to reduce the development time from two to three years to just 14 days.” However, later in the day, the World Health Organization (WHO) tempered expectations, publicly stating “There are no known effective therapeutics against this 2019-nCoV and WHO recommends enrollment into a randomized controlled trial to test efficacy and safety...A master global clinical trial protocol for research and prioritization of therapeutics is ongoing at the WHO.”

As this week’s author points out, the coronavirus epidemic is “a fast-moving target, so anything written about it today is likely to be out of date by tomorrow.” As such, it is almost impossible to pontificate on the long- term (and even short-term) impact the virus might have. However, what is clear is that there has and will continue to be health, economic, and political fallout that extends beyond the epidemic’s epicenter and into the global system. Let’s hope that the ultimate impact is muted, and that Asia and the rest of the world can return to business-as-usual in short order.

Although its health impact outside China has so far been minimal, the novel coronavirus epidemic (or “Wuhan flu,” as we’ve dubbed it) is clearly the biggest risk to China’s economic growth this year, and the main source of risk and volatility for global markets. It’s also a fast-moving target, so anything written about it today is likely to be out of date by tomorrow. Yet thanks to the heroic efforts of public health officials, scientists and journalists over the past couple of weeks, we now have enough information to begin to make useful judgments on the epidemic’s effects. We can divide the issues into three categories: health risk, economic impact and political fallout. The broad—and tentative—conclusions are:

Health risks

As is normal in the early stages of an epidemic, there’s been a lot of uncertainty about the risks of the Wuhan flu, but the fuzzy picture is gradually becoming clearer in a couple of respects. First, despite the headlines touting tens of thousands of cases in dozens of countries, at the time of writing—about two weeks after Wuhan and surrounding areas were quarantined—99% of the approximately 20,000 confirmed cases are in China. And within China, two-thirds of cases, and virtually all the 400-odd deaths, are in Hubei province. The ten coastal jurisdictions stretching along China’s coast from Hong Kong to Dalian in the northeast, which account for 41% of China’s population and 53% of its GDP, have around 3,000 cases.

In other words, in Hubei there are 23 cases per 100,000 population; in China’s most economically important and internationally-exposed regions the figure is just 0.5 per 100,000. Obviously, these figures could change, and some epidemiologists worry that the true number of cases in China could be much higher. But at present the epidemic seems more a central China affair than a truly global phenomenon.

Second, the severity of the Wuhan flu appears to be less than that of other recent flu scares, though quite a bit higher than normal seasonal flu. Mortality-rate estimates have come down and now hover a bit above 2%, compared to 10% for SARS and the 1919 Spanish influenza, and 30% and up for more virulent flus like MERS and avian influenza. From here the reported mortality rate is more likely to fall than rise (as is usual in epidemics), as better reporting leads to the identification of less severe cases.

There is also something of an inverse correlation between mortality rates and transmission, both for viruses in general, and for respiratory viruses in particular. If a virus does not kill its host, the period of infection during which it can be transmitted is longer, and the probability it will be passed on is correspondingly greater. For coronaviruses and other influenzas, human-to-human transmission depends on the viruses binding to cells in the upper respiratory tract (from where their infection is spread by coughing or sneezing). Viruses that do not bind in the upper respiratory tract, but instead penetrate deep into the lungs are more likely to cause fatal infections, but are also less readily passed on. There have been rare and scary exceptions like the Spanish flu, which combined high transmissibility with high mortality. At present, the Wuhan flu does not look like one of these exceptions. (For a good illustration of how this coronavirus stacks up against other flus and diseases, see this New York Times graphic.)

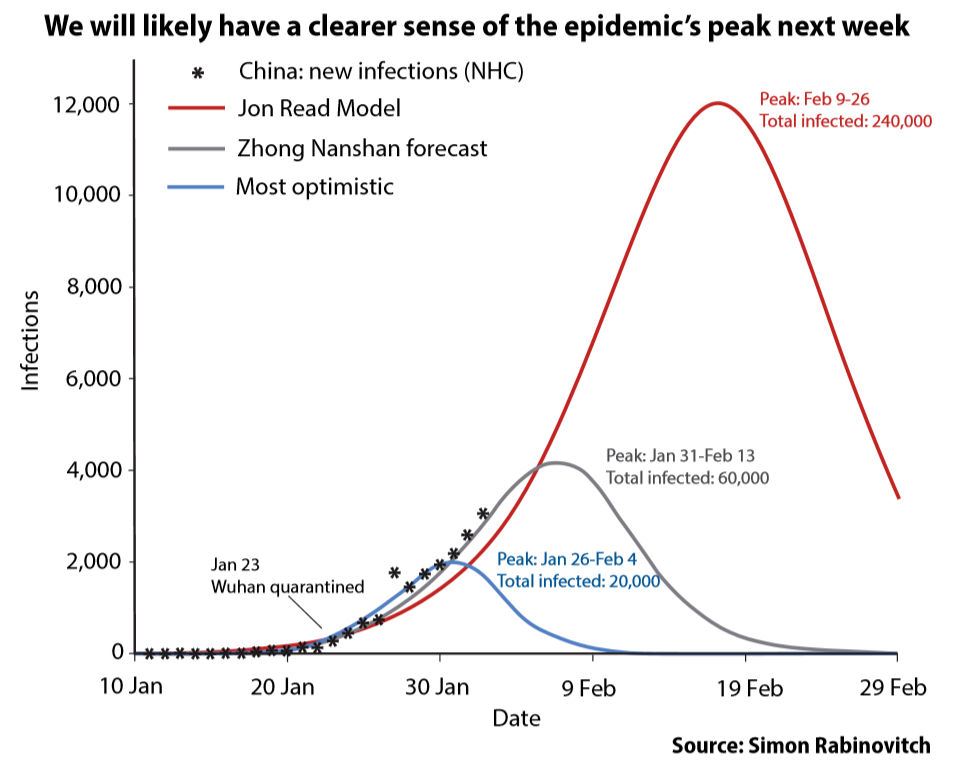

Unfortunately, we can have little confidence on the key question: how much worse will the epidemic get, and when will it peak? A useful guide to the possibilities is the chart below, distributed on Twitter by the Economist magazine’s Shanghai correspondent Simon Rabinovitch. It shows two projections of the virus’ spread, one by the eminent Guangzhou-based epidemiologist Zhong Nanshan (who rose to fame as a voice of scientific discipline during the Sars epidemic), and the other from a respected lab run by Jonathan Read at Lancaster University, which put out an early estimate. The stars represent the actual number of new infections.

Basically what the graph shows is that infections have blown past an early rosy scenario promoted by the government, and are tracking both Zhong’s estimate—which now looks like a best-case scenario—and Read’s more alarming projections. It will probably be a week before we have any clear sense of whether the epidemic will peak in mid-to-late February, as Zhong now predicts, or get dramatically worse.

Economy and markets

Last week we made two main points about the economic impact of the epidemic: first, that we should expect an initially severe hit followed by a strong bounce-back after the virus is seen to be under control; and second, that China’s economy will be affected far more by the severity of government policy responses—Draconian quarantines and restrictions on travel and movement—than by the disease itself.

Given the uncertainties involved, it’s a fool’s errand to come up with highly specific forecasts for the ultimate impact on Chinese, regional or global GDP. But we can set some parameters. The discussion here assumes that, even if a lot more cases are reported in the coming month, the disease stays largely contained within China and peaks somewhere in the next 2-6 weeks. Obviously, if it does turn into a global pandemic all bets are off and both China and developing countries with weak public health systems will be at much greater health and economic risk. Global supply chains would face more disruption, commodity prices would fall more severely, and central banks would come under more pressure to offset the impact with easier policy.

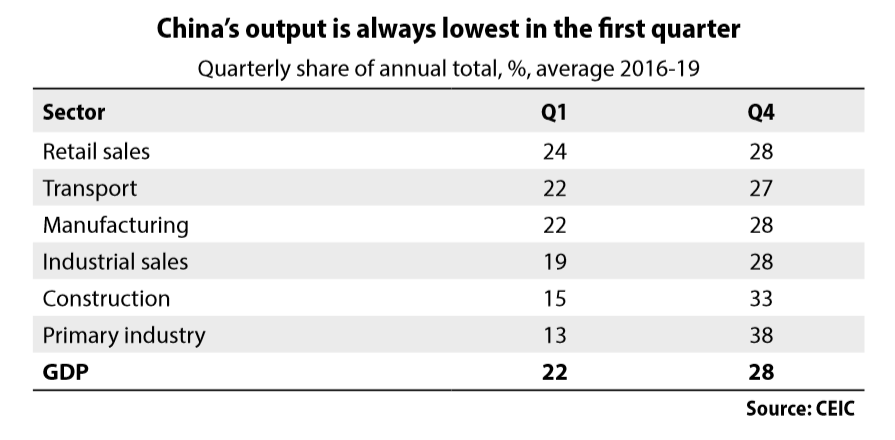

In the non-pandemic scenario, economic damage in China will be concentrated in the first quarter. Most volume measures in China show a strong seasonal pattern, with output lowest in the first quarter and highest in the fourth. In the last four years, Q1 accounted for 22% of annual GDP while Q4 delivered 28%.

So the good news is that if you’re going to have a massive negative economic shock, the first quarter is the time to have it, because less is going on anyway, and there is room for catch-up later in the year. The flip side of this, though, is that because of the small base, comparatively small volume changes in Q1 can have a disproportionately big impact on year-on-year growth rates. We can reasonably expect, therefore, that the growth rates for a swath of indicators in Q1 will be horrific.

How horrific? We can make a first approximation simply by counting the working days lost by the extension of the official Chinese New Year holiday by an additional eight days. This cuts the official number working days in the quarter by -13%, from 61 to 53. In theory, on this basis alone, substantial double-digit declines in many production-side economic indicators might be expected over the first three months of the year.

In practice, however, in a normal year industry begins to wind down 10-15 days before the official holiday and takes another 10 days or so to regain steam afterwards. As a result, the low productivity period for industry extends for about two weeks either side of the lunar New Year’s Eve. So if the current eight-day extension of the holiday is not extended further, the year-on-year downturn in industrial production is likely to be smaller than a simple calculation of official working days lost might suggest.

Consumption might not be hit so hard, since the government has forbidden employers to lay off their employees or stop paying them, and many goods purchases can be made online. Nevertheless, services and durables purchases will presumably suffer, and corporate cash flows could shrivel as companies are forced to keep paying their wage bills while seeing a sharp fall in sales.

How much this affects full-year GDP depends on how much bounce-back comes in the subsequent quarters, once the epidemic is contained and normal commercial conditions resume. Consumer discretionary purchases will not bounce back: people will not eat more restaurant meals in June because they skipped a few in February. Other kinds of activity, though, have plenty of rebound capacity, either because they are seasonally skewed to later in the year anyway, or because they are necessary purchases (think homes and cars).

Three critical sectors to watch are construction, autos, and electronics. Our basic story about China’s economy in 2019 was that surprisingly strong construction activity offset recessions in cars and electronics; and our pre-coronavirus story for 2020 was that slower construction activity would be offset by a modest recovery in the two key manufactured goods categories— autos and electronics. All three have decent rebound capacity.

Construction is of particular interest because it is unusually seasonal: typically 85% occurs from April onward. In absolute terms, therefore, a big slowdown in activity in Q1 would not necessarily say much about the outlook for the year. Our base case was that construction growth would slow to 3% this year from about 8% in 2019. But if most construction activity gets back-loaded to the last eight or nine months of the year, the result could be a collapse in steel prices in Q1 followed by massive rebound in the spring.

For autos, our baseline view is that the recovery in car purchases visible at the end of last year is likely to resume once the epidemic is contained. Electronics is of interest not only because of the sector’s domestic effect, but because China is the indispensable hub for global production. Again, production volumes are usually light in Q1 and heaviest in the second half.

The global impact is a bit harder to assess until we know for sure whether other countries can simply keep focusing on reducing links with China, or if they need to take on more restrictive measures to slow the epidemic at home. The main immediate sources of worry are tourism and commodity prices. In much of Asia, Chinese travelers account for 30-50% of international tourism income, and even in the United States the figure is a hefty 14%. With most direct flights in and out of China now canceled for weeks or even months, southeast and northeast Asian economies will take a material hit.

Similarly, the oil price has plunged to the floor of its established range on reports that Chinese demand could fall by as much as -20%. A construction slowdown could extend the commodities rout into base metals. It is hard to see much joy for emerging markets in this environment, and the outperformance of the US economy and equity markets should continue. If the epidemic does get contained in the next month or so, however, the rebound effect favoring commodities and emerging markets (especially in Asia) could be dramatic.

Political fallout

The most enduring results of the viral episode could be political. Globally, the central theme is trust. The world reaction to this virus has been extraordinary— substantially more extreme than with Sars, despite evidence that the severity of the health risk is lower, and the fact that the central government response has been much more prompt, decisive and transparent. One simple example: most US airlines have canceled all direct flights to China for at least the next two months, and in some cases for three months. The last time such blanket cancellations were imposed was in the aftermath of the 9/11 attacks in 2001, when virtually all US air traffic was grounded—for a few days.

This massive reaction was first driven by the Chinese government’s own reaction of shutting down its economy since late January. If nothing is likely to be going on in China for the next month, there is not much reason to go there, and there is no reason for airlines to keep running empty flights. But this does not quite explain why flights need to be canceled for three months, nor why the border restrictions on people arriving from China (initiated in an extreme form by the US and emulated more flexibly by various other countries) need to be quite so stringent.

China’s government has attacked these restrictions as politically motivated, and in the case of the US there is more than a grain of truth in this, since Donald Trump’s administration has a vested interest in painting China in the most unfavorable light. But the bigger issue is that throughout the world, there is lack of confidence in (i) the capacity of China’s public health systems to handle a fast-moving epidemic; (ii) the willingness of local governments to competently address this kind of crisis and report accurate information up the chain; and (iii) the reliability of action and information-sharing by the central government. These fears are not just confined to Westerners: in Hong Kong, the largest pro-Beijing political party has demanded a virtual sealing of the border with China to prevent a spread of the virus into Hong Kong, which so far has reported only a handful of cases.

The concerns are well-founded, and hard for Beijing to address. In theory, lack of public health capacity could be addressed by large-scale technocratic investments. In practice this is not so easy, in part because central and southern China is probably the world’s biggest incubator of influenza viruses, for reasons including climate, the high density of duck and pig populations, and the ingrained popularity of live-animal markets. Controlling flu outbreaks will require extensive re-engineering of social and animal husbandry practices. Moreover, while building hospitals is quick, staffing them with qualified doctors and support teams, and plugging them in to a well-developed national epidemiological system will be the work of decades.

Even more intractable is the governance problem exposed by the Wuhan authorities’ efforts to keep the epidemic under wraps until it was far too late to contain it. Local government incompetence is a global phenomenon, but in open societies the whistle-blowers who were silenced in late December would have found outlets through the media or higher levels of government. The incentives for local officials to conceal bad news and paste a veneer of “stability” over any simmering problem have always been great; but under Xi Jinping, who has imposed a culture of strict obedience and harsh penalties for failure to maintain order, these incentives are arguably more powerful than they were a decade ago.

Finally, the Communist Party’s reaction function—which is programmed to move instantly from stolid denial to frantic overreaction—guarantees that any health crisis will have a phase during which people become convinced that the situation is far worse than Beijing is letting on, and that the overreaction signals a lack of control rather than the imposition of it.

These governance problems are likely to lead to opposite conclusions in China compared with the rest of the world. Much of the outside world will be reinforced in its conviction that China is an untrustworthy actor, and that this untrustworthiness is baked in to its opaque, authoritarian and overcontrolled political system. This could impose several long-run costs.

Although foreign companies are not going to pull up stakes from one of their biggest global markets, China’s public health unreliability will make it that much harder to convince international staff and their families to move there, and will create yet another reason for diversifying supply chains into other countries. And China’s efforts to convince the developing world that it has a political-economic model worth emulating will surely take a hit.

Within China, though, the eventual success of the anti-epidemic campaign will likely be read as a validation of authoritarian, top-down management— and the party will pull out all the propaganda stops to encourage that reading. There has been no shortage of grumbling and outrage on Chinese social media, but as usual the targets tend to be local, not systemic. The gap between China’s perception of itself as mainly competent, and the world’s perception of China as somewhat untrustworthy, will widen. And the tricky task of getting China’s unique system to play nicely with the global system will get trickier.

Data and ideas for this article were provided by Andrew Batson, Tom Holland, Rosealea Yao, Ernan Cui and Thomas Gatley.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.