“Strained affordability is not only a source of risk for developers and foreign investors. Rising interest rates and tighter lending conditions can abruptly end a real estate boom if property becomes too pricy, as the current example of Sydney shows.”

–UBS in its Global Real Estate Bubble Index

Back in early-September, we ran a fascinating interview with Rick Davidson, former CEO and President of Century 21. In the exchange, Rick hinted at the beginnings of a real estate slowdown in the US, anticipating coastal markets would see the tide shifting first, before a more broad-based tightening took hold. Since then, ominous headlines have made waves in national publications, echoing and expanding on this outlook (you can find a particularly popular one in The Wall Street Journal).

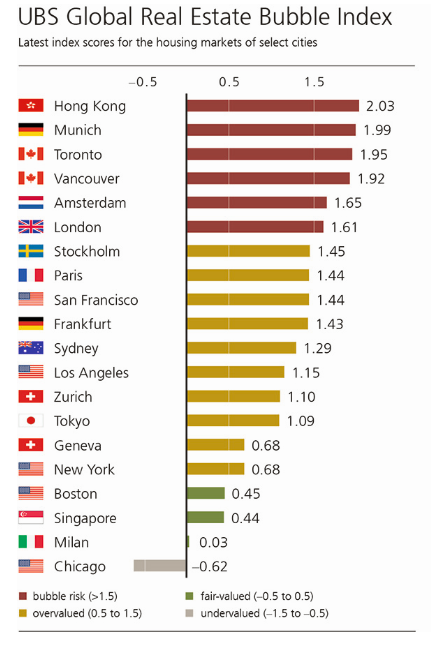

While it’s easy to get bogged down in home-country bias and focus attention on US markets, for globally-minded individuals who have been watching other major international metros, the story is more alarming in many cases. UBS recently published a study that illustrates just how overvalued – and bubbly – several major real estate markets are globally.

The worldwide representation of this chart – with cities spanning four continents – shows the truly wide-reaching nature of Bubble 3.0 (a term that Evergreen coined and on which it has written extensively). One reason higher interest rates have been causing so much trouble in financial markets of late is massive mortgage debt related to all of these inflated housing markets. This point illustrates one of our long-conveyed views that the extremely elevated level of debt globally makes both markets and economies very vulnerable – especially as rates rise. And while much of the world has been experiencing a tightening in the housing market, no bubble is more concerning than Australia’s.

Australia, you say?

Yes, the land Down Under has benefited from the longest period of economic expansion in modern history, avoiding the dreaded “r” word for over 27 years. (Side note: for optimists ignoring the tea leaf readings in the US, that is surely a factoid to find hope in for a “soft landing” and the continuation of the current 10-year expansion – even if it may soon be the longest in US history.) As you will read below in the insightful missive by one of our favorite guest authors, Danielle DiMartino Booth, the Aussies' lengthy streak is in jeopardy for a myriad of reasons, but hinges on its substantial reliance on its housing sector.

The final frontier of economic resiliency is in jeopardy. Let’s hope China – by way of the US – doesn’t spoil the g’day.

*Editor’s Note: For more from Danielle, we recommend reading her popular book Fed Up: An Insider’s Take on Why the Federal Reserve is Bad for America. Additionally, Danielle provides terrific daily and weekly insights via her Daily Feather and Money Strong letters.

THE NOTHING BEYOND

AUSTRALIA: THE FINAL FRONTIER OF ECONOMIC CIVILITY

By Danielle DiMartino Booth

Ne plus ultra, “Nothing More Beyond,” was the warning that greeted navigators and sailors at the opening of the Strait of Gibraltar. The message was clear: Cross this maritime Rubicon into the realm of the Unknown at your own risk. Legend has it that Hera, the queen of the gods, drove Heracles mad, which ended tragically with the greatest of Greek heroes slaying his wife, son and daughter. His sanity restored, he sought to atone for his atrocities. Pythia, the Oracle of Delphi, instructed Heracles to humble himself at the disposal of his cousin, King Eurystheus, for 12 years in whatever capacity requested. The result was the 12 labors of Heracles, the tenth of which involved cattle raiding from the monster Geryon’s herd at the edge of the Unknown. Hence that great Rock which stands sentry to this day.

There are however, friendlier, equally ancient, interpretations of the origin of the hulking pillars erected by Heracles. Mythology holds that he was not just a hot hunk, but also a munificent multitasker. According to lore, rather than transverse the mountain that was once Atlas to reach the site of his tenth labor he simply smashes through and slays the mountain. In a kinder, gentler mythological world, he used his superhuman might to narrow an existing strait to impede any monstrous entry to the Mediterranean Sea. In what can only be described as Ancient Greek magnanimity, Heracles also devised the two great pillars to uphold the heavens and in so doing, freed Atlas from his eternal damnation of carrying the weight of the celestials on his broad shoulders.

As much as we’d like to embrace this softer version of history, descendants of Atlas will always have a bitter taste in their mouths at the mention of the Herculean name. The much more common version of history involves Atlas being outwitted by Heracles. Take your pick – outmaneuvered or pitied. Neither induces that sense of pride to which Greeks endlessly aspire. If nothing else, Atlas’ clan will always have the stars to behold given their namesake, second-best of Greek heroes, was the first to instruct us mere mortals in the science of astronomy to navigate and measure the seasons.

Giving short shrift to Atlas also discounts his lessons for the ages on the virtues of endurance, of seeing something through from start to finish. Toilers of the dismal science marvel at the tenacity of the Atlas equivalent of the day, the economic stalwart of Australia. The land Down Under last exited recession in September 1991, making the 27 year stretch that’s followed a modern-day record run of uninterrupted economic expansion. Over that span, GDP has grown by a remarkable 3.2% per annum on average.

The Federal Reserve’s Jerome Powell even spoke admirably of Australia in his watershed speech at the New York Economics Club in which he acknowledged Fed policy was tighter than he had previously surmised. The London-based Centre for Economics and Business Research projects that by 2025, Australia will have leap-frogged two spots to become the world’s 11th largest country (right behind Canada).

The beauty of Australia is that the wealth is nicely spread vis-à-vis other developed countries. Fade the country’s average net worth of $411,060 which ranks second only to Switzerland; it is skewed by the wealthiest Australians. What’s truly exceptional is that according to Credit Suisse’s 2018 Global Wealth Report, at $191,453, Australians have overtaken the Swiss in terms of median wealth per adult – that’s the wealth of the average countryman and woman at the midpoint of distribution. That helps explain why only 6% of Australians have a net worth below $10,000 vs. 18% for the United Kingdom and 28% in the United States.

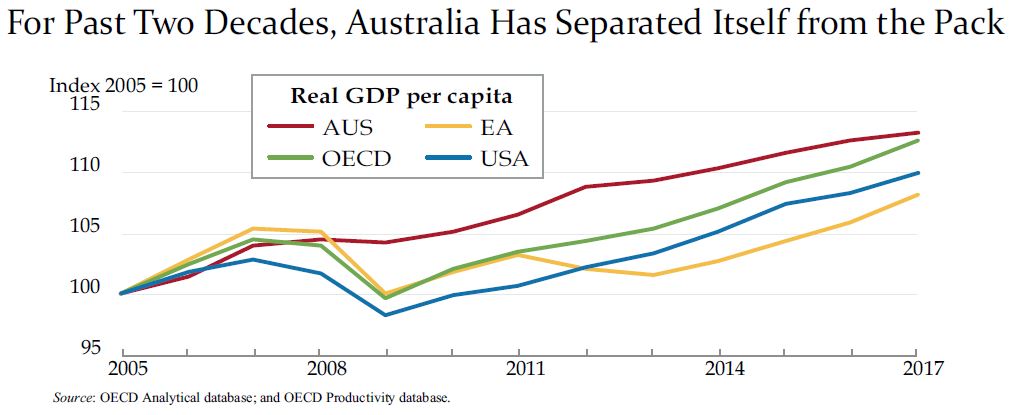

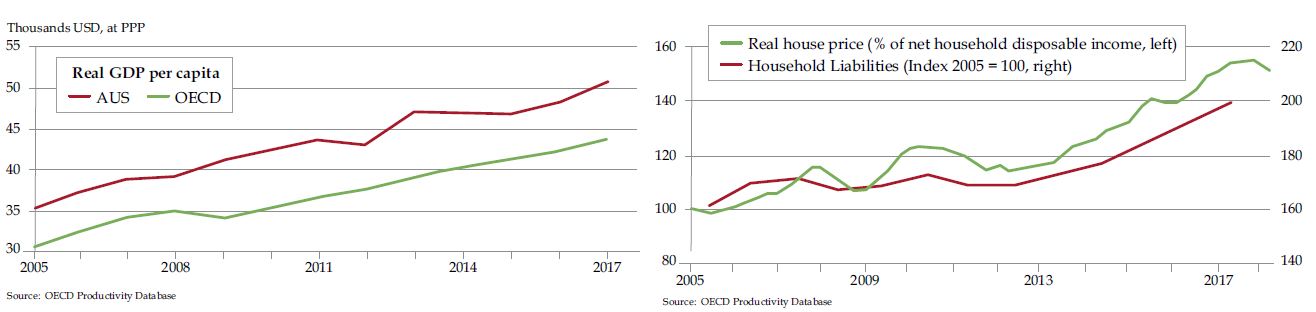

Pictorially, it is clear something changed for the better about 20 years ago when inflation-adjusted GDP per capita separated itself from the developed world pack. You may note that the advantage gap has closed in recent years with the rest of the countries in the Organization for Economic Cooperation and Development (OECD).

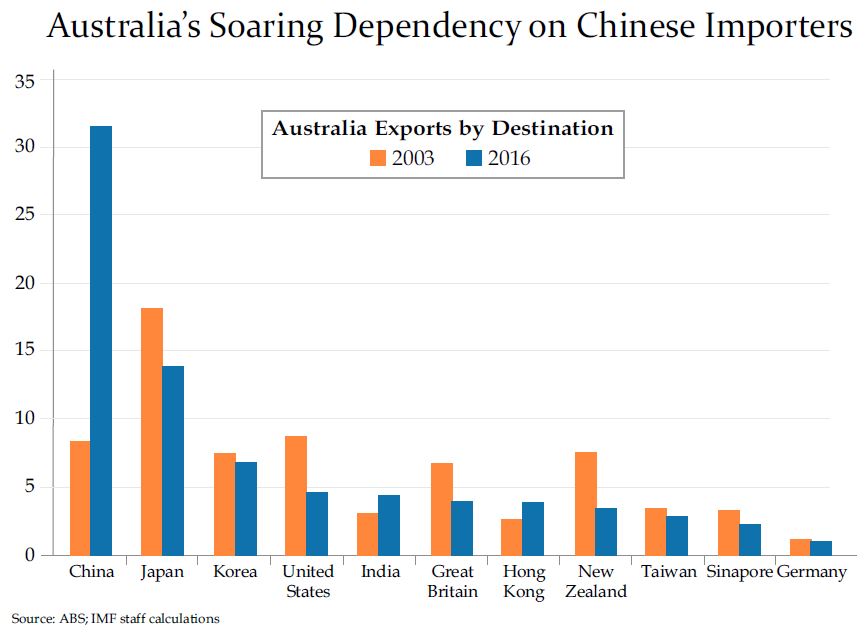

This next bit of analysis will come as no surprise aside from the magnitude of the shift that’s taken place. It’s hard to fathom, but back in 2003, China was the destination of 7% of Australia’s merchandise exports. Japan and South Korea were bigger trading partners at the time. Fast forward to 2016, the most recent year for which we have data, and China now takes in a third of Australia’s goods exports, more than all non-Asian nations combined.

Of course, back in 2013, China’s economy was growing at a 10% reported rate. Over the period depicted, GDP growth averaged 9.6% — phenomenal levels even if one takes a hatchet to them to account for government manipulation of its statisticians.

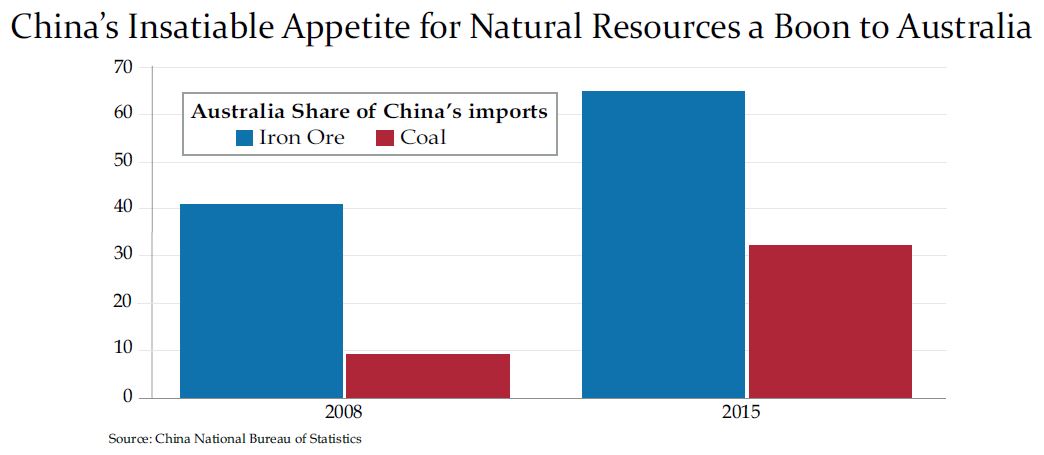

Drill down (pun alert) to Australia’s richest resources, and you see that over a seven-year span, China came to absorb nearly two-thirds of Australia’s iron ore to feed its massive appetite for steel and about a third of its coal, a trebling over the period.

Add up all of Australia’s mineral exports and they comprise around 35% of Australia’s total exports. At 35% of international traded in coal, Australia leads the world as its largest exporter. But the country is also the largest exporter of iron ore, lead, diamonds, rutile, zinc and zirconium, the second-largest of gold and uranium, and the third-largest of coal.

According to the International Monetary Fund (IMF), the stability of Australia’s supply chain with China has helped it foster trading relationships with other Asian countries along the Chinese/Australia trading route. As of 2016, roughly 75% of all Australian exports landed in Asia vs. 55% in 2003.

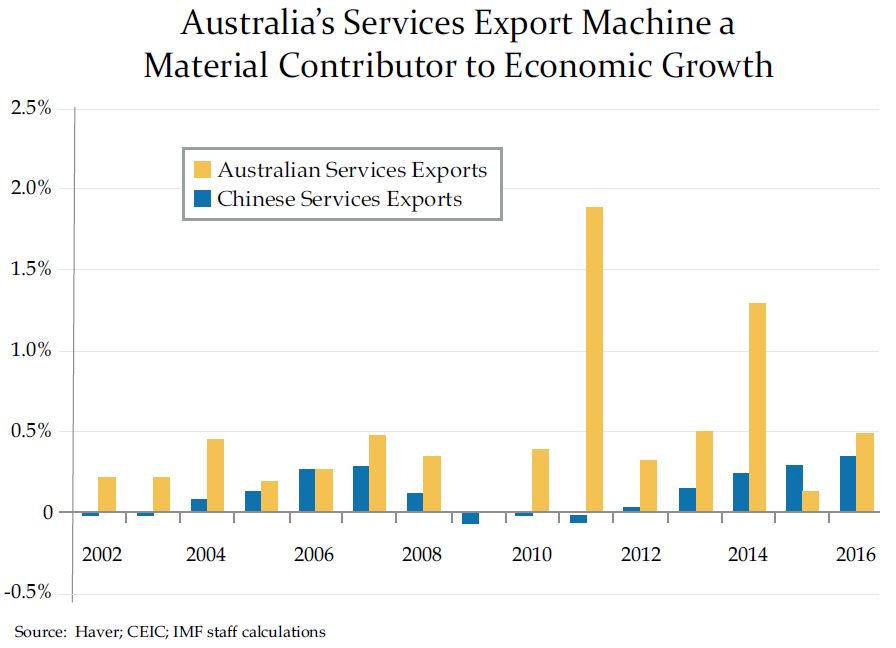

Many economists limit their discussion to trade between China and Australia. But the relationship goes much deeper. Over the past decade, the number of Chinese visitors to Australia each year has risen by 273%. That compares to just 43% for all other nations. Moreover, the Chinese tend to spend more per visitor than those from other countries, which adds up quickly. In 2007, Chinese opened their wallets to the tune of $1.3 billion. By last year, that figure had swelled to $8.3 billion.

Part of this willingness to open their wallets is tied to the appeal of Australia’s higher education system. Students may comprise just 7% of all visitors, but they account for 37% of the money spent, more than any other cohort. As you can see, in recent years, Australia’s Services Exports, including education and tourism, have become a more meaningful support to Australia’s GDP. Eyeball the contribution at about 0.5%; that’s still meaningful in the context of an economy that’s been growing by 3.2% on average since 1992.

You couldn’t be blamed if the psychological term “codependency” has come to mind. Is Australia addicted to Chinese growth? Is its economy and, by extension, its population’s wellbeing too reliant on its biggest trading partner? The answer is yes and no.

Most (non-American) economists predict that China will unseat the United States to become the world’s largest economy by 2030. That’s saying something considering that on a purchasing power parity (PPP) level, China’s economy was smaller than that of Brazil’s in 1960. In the event you’re rusty on your economic terminology, PPP compares different countries’ currencies using a “basket of goods.” Two currencies are on par with one another, when a basket of goods is priced the same in both countries. On this equilibrated level, China has in fact already surpassed the United States.

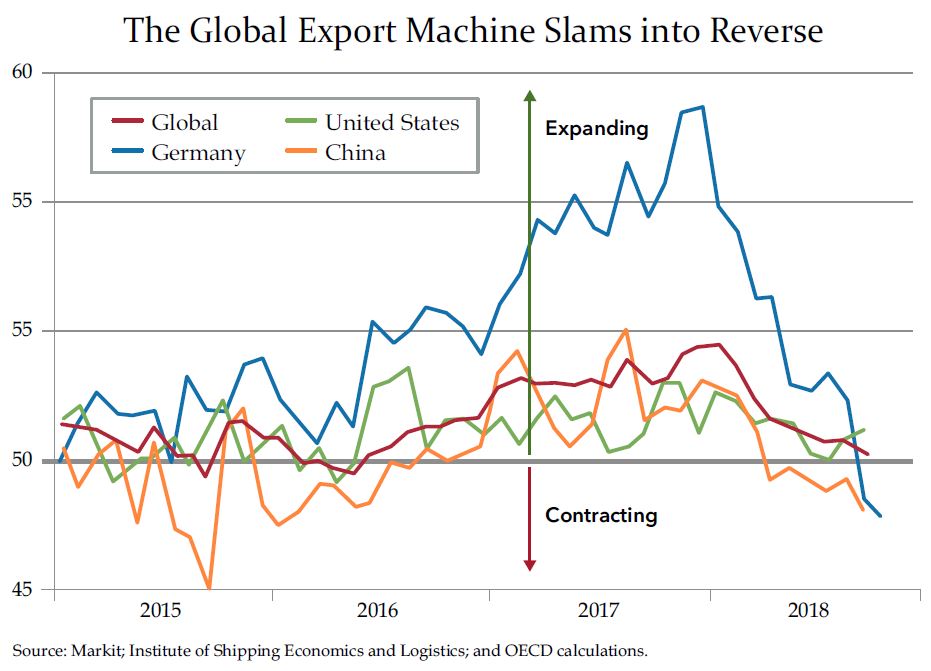

That should bode well for Australia assuming growth continues to favor the eventual global dominance of China. But first, we all have to traverse the global economic slowdown in the making. In what can only be described as a stunning reversal of fortunes, global trade has flatlined. This next graph depicts new orders for the manufacturing sector among China, Germany and the U.S., the world’s three largest exporters in that order. For the moment, new export orders are still expanding in the U.S. But we would caution that U.S. export orders have fallen to a two-year low care of the strengthening in the dollar. The gravitational pull of the slowing in the rest of the world should claim the U.S. as its last victim as uncertainty about the eventual outcome of the trade war persists.

As for China and Germany, two other countries that are discovering their economic overreliance on one another the hard way, they’ve long since dipped into contractionary territory in their export sectors. This development does not bode well for Australia.

Even assuming the U.S. escapes the fate of its global exporting peers, which is delusional, such an occurrence would do a whole lot of nothing for Australia which only exports 5% of its Goods and Services to America, less than the 8% it exports to the European Union. The composition of Australian exports goes a long ways to explaining its reliance on emerging economies that continue to build out their urban centers and infrastructure. Note that none of the top four categories of Australian exports to the U.S. — motor vehicles, aircraft, medical equipment and telecom parts — have the heft to command a slice of the pie depicted below.

It’s likely that every time an Aussie reads an article dismissing parallels between the late 1990s Asian financial crisis and the currently unfolding episode, they must breathe a sigh of relief. Keep Asia importing Aussie goods and services at all costs must be the mantra. The catch is the country’s biggest challenge comes from within.

Over the past year, net exports have not been the biggest contributor to Australian GDP nor even the second-largest. The country’s bread and butter, rather, is its residential real estate sector which contributed over twice that of exports and government spending on infrastructure. To be clear, the 3% growth rate is nothing to sneeze at.

It’s the pace at which growth is slowing that has raised some the blood pressure at the Reserve Bank of Australia (RBA), a stalwart central bank that’s stood out on the global stage for resisting the asinine policies adopted by its debt-monetization-inclined peers.

In the third quarter ended September, seasonally-adjusted quarterly growth slowed to 0.25%, a third of its 0.9% growth in the second quarter and half of what the consensus was projecting. The government warned that this pace was the worst since the third quarter of 2016 when growth actually contracted. More notably, on a seasonally-adjusted basis, GDP per capita actually declined.

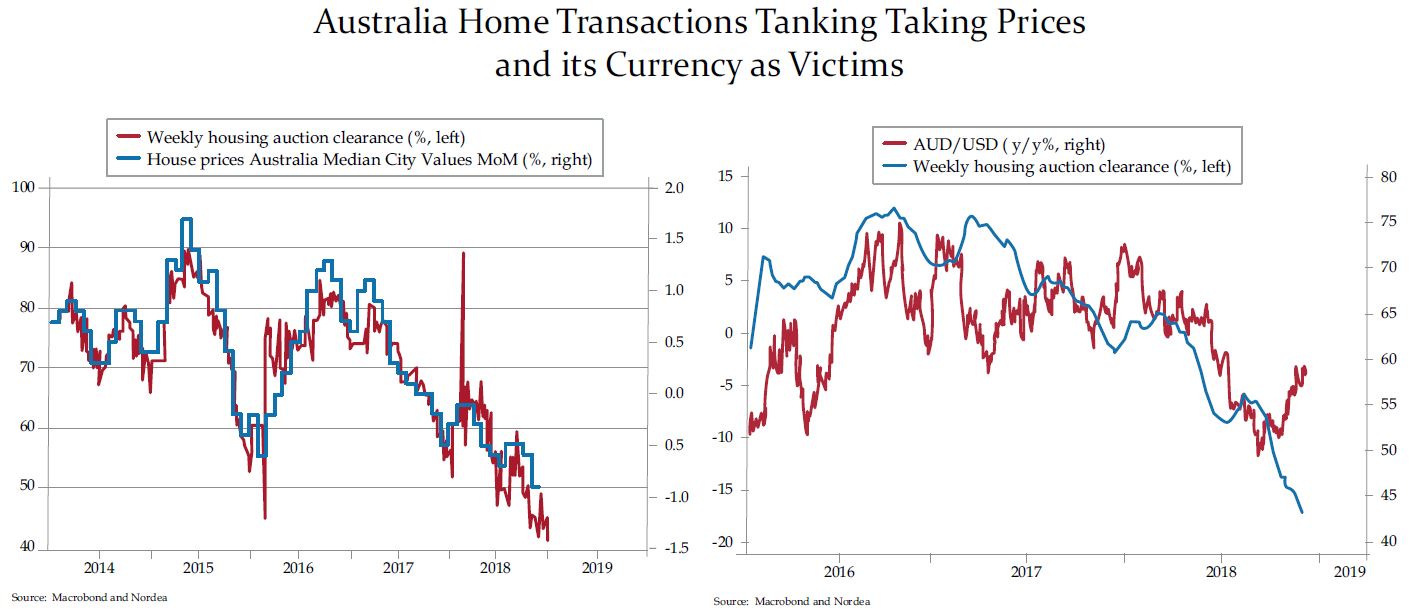

The main culprit in the GDP slowdown was a ratcheting back in private consumption. What’s put Australian households in such a foul mood? At the risk of death by depiction, allow some recent charts to graph a picture. Since peaking last year, home sales have slowed to such an extent prices have followed. October marked the 15th straight month of falling house finance commitments and the 13th consecutive months of declining owner-occupied financing, the longest negative stretches since 1991.

The country’s outsized reliance on its housing sector has also hit the Aussie dollar. The combination of the two is thus a double body blow to Australian net worth and their ability to escape the local headlines with some travel abroad, which is now a wee bit pricier a proposition.

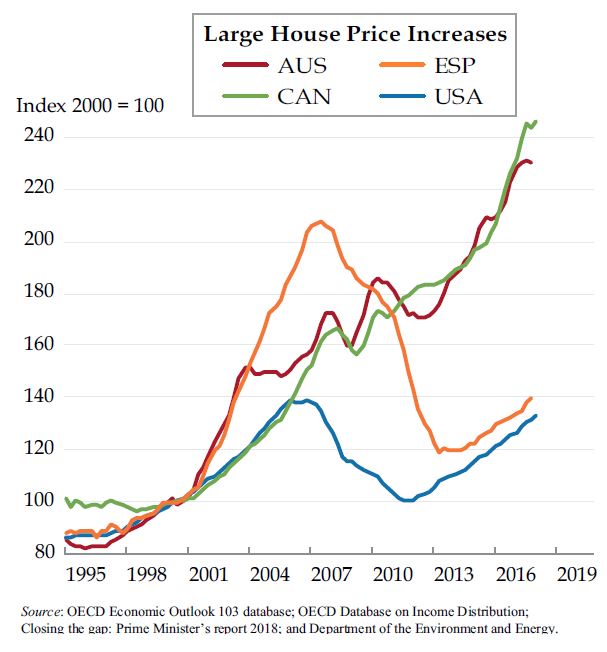

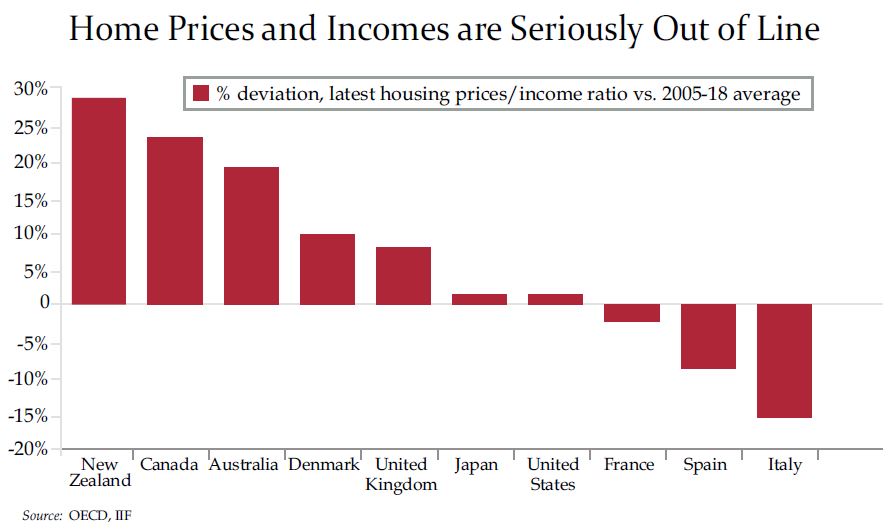

The story is nothing new to Americans who consider themselves to be hardened veterans of housing busts. But then, our central bank has been a floosy compared to the RBA, in terms of monetary policymaking discipline. That said, the risk is the constant, soothing purring of the Aussie export engine has anesthetized the RBA to a comatose state. Compare both Australia and Canada to the epic bubble that inflated in Spain and the relatively tame bubble that visited U.S. shores. Yes, these countries do make even the most hardened speculator blush.

![]()

Looked at slightly differently, only New Zealand and Canada sport house price/income ratios that are more out of whack than those of Australia. An aside, yours truly is a huge fan of the Italian countryside. If you are as well, you might want to set an alarm to go villa hunting once the global recession has set in. Just a suggestion.

It’s equally notable to see that the United States market is sort of in equilibrium despite what we know and increasingly read – that an affordability crisis is sweeping the country in the face of rising borrowing costs and the past few years' runaway home price that’s pushed prices back up to their pre-crisis peaks.

In a fresh study, the OECD, referring to Australia, worried that such confluences of events rarely end with soft landings. “Though house prices have eased recently, they remain high in level terms (they have more than doubled in Sydney and Melbourne since 2005),” said the report. “Also, the ratio of house prices to incomes has increased substantially in recent years and the ratio of mortgage debt to household incomes remains elevated.”

As was the case with the deflating of the U.S. housing bubble and not surprisingly, the worst damage is being done in the biggest cities with prices in Sydney and Melbourne down by 8% and 6% over last year. A separate and distinct parallel is the influence foreign buyers have had on these marquee markets as Chinese money has poured onshore. Of course, the same clampdown that spurred China’s dumping $1 billion of U.S. commercial real estate has to also be taking a deep bite out of a Australian housing.

The same dynamic playing out worldwide is also apparent in Australian high-end housing, which is also suffering disproportionate home price declines as is the case in Hong Kong, London and New York.

![]()

Because of the massive runup punctuated by Chinese foreign investment, Australia is vulnerable to withstanding harsher home price declines compared to other global markets. The glaring exception would be Hong Kong, a market that’s been swarmed to a greater extent by deep-pocketed offshore investors.

Broadening out, it would seem to be naïve at best to look at the next pair of charts in isolation. Few countries can brag that their economy is an island, not even an island nation as immense as Australia. Australia’s outsized growth over that of OECD nations did not, in other words, drop as a gift would from the heavens.

Conversely, no country could hope to escape the fate promised by households being indebted to the extent Australians are against a backdrop of a housing bubble for the history books. Rather than providence, it is China, the world’s second-largest economy that has afforded Australia the ability to escape what would have long since been a less-tethered country’s destiny.

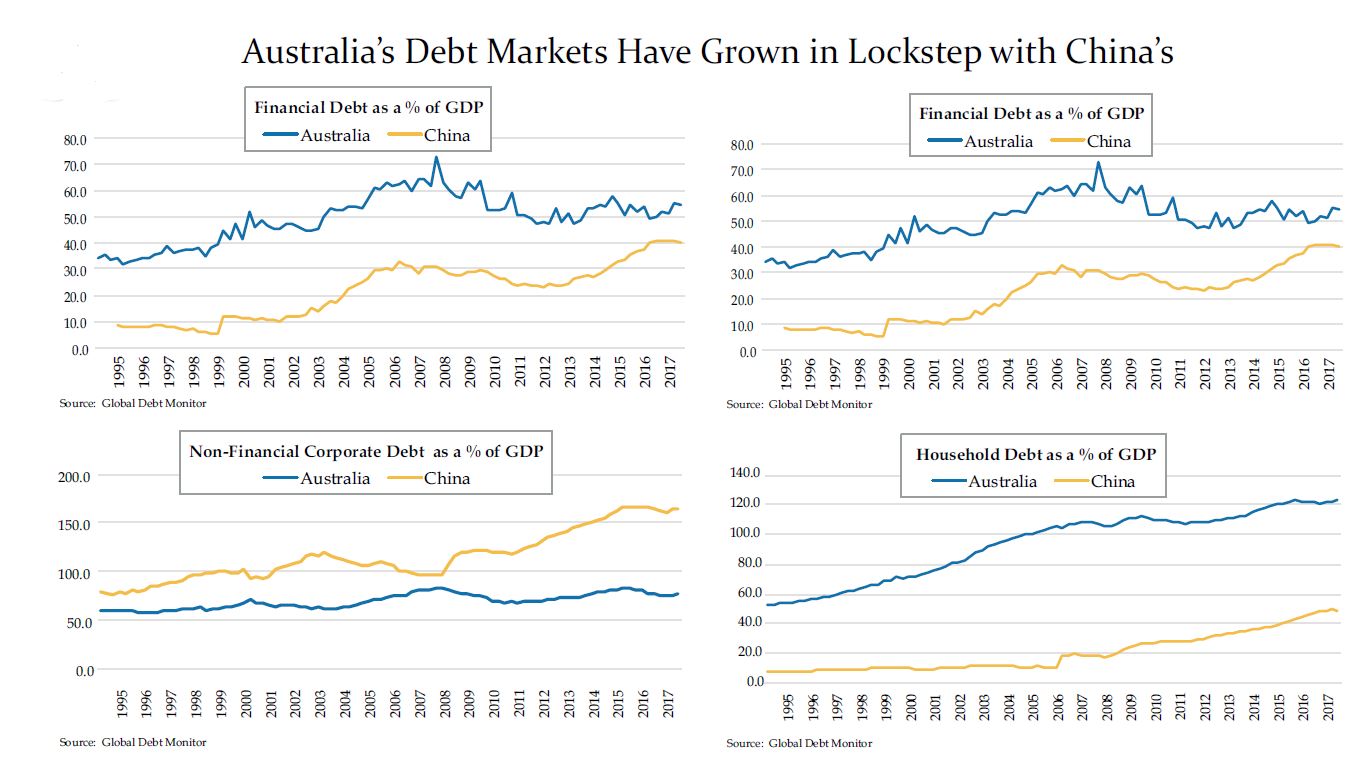

So hyper-extended is the country’s finances behind this next chart, it needs no formal introduction. If you’ve been away for an extended period of global leveraging, however, you can be excused for not knowing it is China in all its glory. As you can see, in the years leading up to the financial crisis, China’s aggregate debt to GDP hovered just above the 150% line. But crises can be expensive clean-up jobs. The continuous effort needed has now pushed debt to GDP north of 300% leaving the country swinging in the wind vulnerable to global vagaries as no other.

Like the bloodlettings that were once applied to relieve a patient’s woes (and kill them in the process), Australia appears to have adopted the same broken medicine to propel its country’s economy. It is visually uncanny to see how closely in tandem the debt build has been in both countries’ financial and government sectors. The one corner of the debt markets that has not grown in concert is non-financial corporate debt. Call that Australia’s fortunate exclusion. Australia’s household sector, at the opposite end of the spectrum, clearly stands out as a shortcoming of its own making and in turn, undoing.

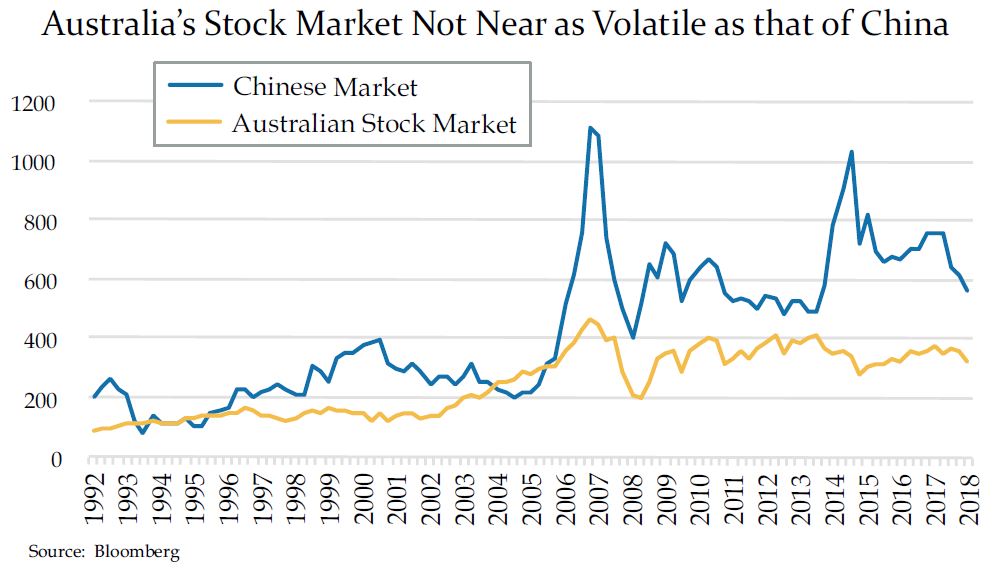

The equity side of the equation is not near as skewed as that of the debt markets. Even so, it’s clear that increasingly as a factor of time, Australian stocks react to moves in China’s stock market. The message should be clear: The Aussie dollar is a huge benefit to the country’s stability.

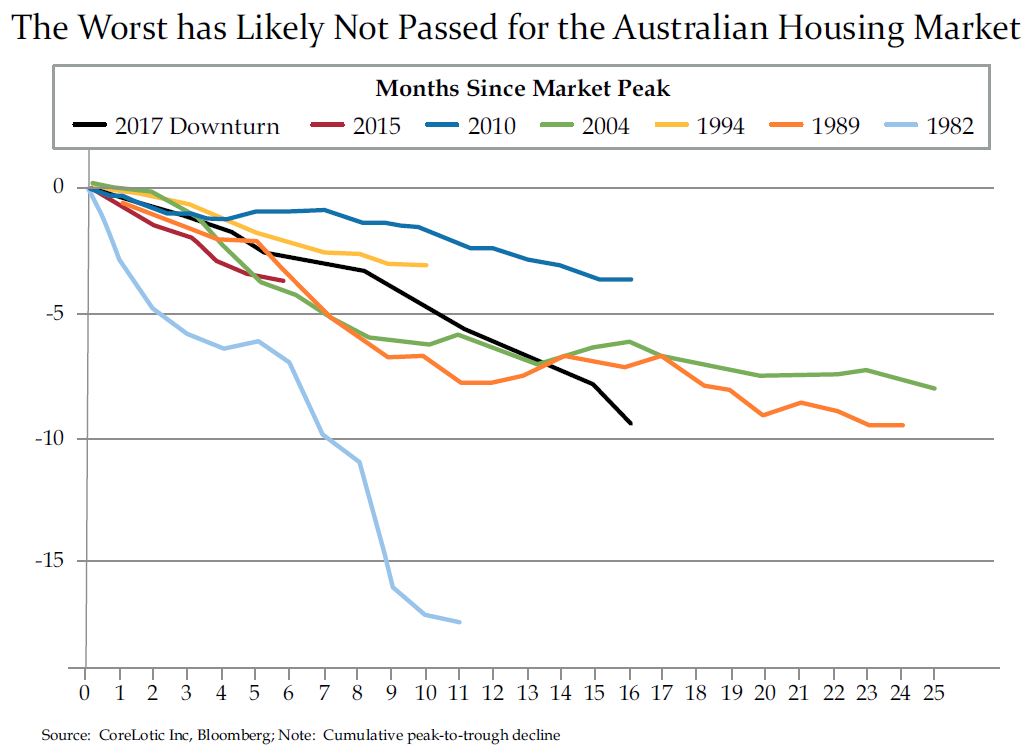

The world’s rational economic leaders have rightly placed Australia on a pedestal as an example of prudence in central banking to be admired and emulated. The likelihood of the country escaping recession in the next downturn, however, look increasingly unlikely. As prolonged and painful as home price declines have been thus far, they do not appear sufficient to prick Australia’s housing bubble. The outcome of the home price declines circa 1982, the last time the country was in recession, appears to be the much more likely conclusion to the near 30-year run the economy has enjoyed.

Societe General’s Albert Edwards, who is often derided as being a permabear, nevertheless sums up the upshot of Australia’s economic end game via the prism of its unquestioned dependency on China’s economy. If Chinese authorities cannot right the ship of their own economy, it is fair to deduce that Australia will suffer right alongside its economy’s biggest benefactor. If you’ll indulge Edwards’ articulate conclusion in full:

“One investment certainty that has now lodged itself firmly in investors’ minds is that the Chinese economy will not suffer a hard landing because the authorities are in control - seemingly able to turn the policy taps on and off almost at will. Investor confidence in China’s resilience could yet prove to be disastrously overplayed.

The naysayers, such as I, have consistently been proved wrong about the ability of China’s policymakers to successfully navigate choppy waters without capsizing the economic ship. And it is wholly natural that investors, having been proved overly bearish about the economy in the past, have given up worrying about a Chinese hard landing - but now that ship looks to be taking on water once again.

I like the ship metaphor. I have likened the Chinese economy to a ship that appears to be sailing smoothly across the horizon when viewed from the shore, destined for the port called the “Largest Economy in the World”. But, if instead you view the ship from the bow, you would see it yawing from side to side, with the policy-setting sailors running from one side of the deck to the other to counter the increasingly violent rocking.”

If it is here that there be monsters, in the Unknown, the waters Heracles demarcated with his wit and might, Australia looks set to go down with China’s ship.

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE *

* Due to the severity of the recent market selloff, we have reduced our equity underweight from 50% to approximately 43%.

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

** Due to recent weakness, certain BB issues look attractive.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.