"When all the experts and forecasts agree—something else is going to happen.” – Venerated market strategist, Bob Farrell.

The No-Fear Fear

Let me be the first to admit it: I loathe being part of the consensus, at least when it comes to economists. My antipathy springs from the sorry track record of the overall economic forecasting community. Like the Fed, it has predicted exactly zero recessions since WWII which means it is something like 0 for 13.

Once again, very few saw the most recent downturn coming. (However, per our special double-edition EVA from September, 2019, we did actually warn of a likely recession soon, as we did in the fall of 2007.) Some might say that a no-recession call was understandable considering how rapidly Covid engulfed the planet which no mere mortal could have anticipated. But this lets economists off the hook far too easily since the official recession arbiter organization—the NBER*—has stated the most recent one began pre-pandemic. Further, both an industrial and earnings recession were well underway in 2019.

*National Bureau of Economic Research

Now, though, we are talking about emerging from, not sinking into, a recession. Consequently, it’s a much different set of circumstances and the “macro econ” tea-leave readers do a better job of calling recoveries. These days, when the Fed fights downturns by flooding the system with trillions of fabricated funds, it’s hard not to see those on the horizon. However, there’s something less joyous swelling that a number of economists see looming and I must concede—uncomfortably—that I also agree with that view.

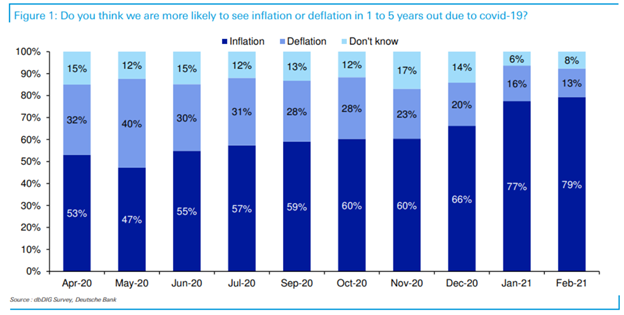

As you can see in the graphic below, economists have drastically increased their expectations of rising inflation, though most feel it will be of the mild variety (that’s where I’m in my more familiar dissenting role). More importantly, the financial markets are suddenly agreeing with them. That’s why the formerly supernova-like parts of the stock market are suddenly reeling. Rising interest rates and inflation are toxic for high P/E names like Tesla and a multitude of other issues selling at 100 times earnings or more.

As I’ve written before, I haven’t worried about inflation in nearly 40 years, ever since the late and very great Paul Volcker broke the back of relentless price increases. But I am now. However, I believe we’re not at the point where broad inflation—versus sharply higher prices in key commodities—is upon us…yet. If I’m right, we’re still in the sweet spot of an accelerating economy with the Fed on hold due to its desire to see higher inflation, such as up to 3%. This is a view I described in detail in our June 19th, 2020, EVA.

Speaking of “the sweet spot”, this week’s Guest EVA, “The only thing we have to fear is the lack of fear itself”, is on that theme. Once more, the author is the always read-worthy Gerard Minack, the scribe behind the Down Under Daily in reference to his home country of Australia. Like me, he’s pointing out how mainstream the notion of a robust recovery has become and, also similar to yours truly, he doesn’t disagree. Logically, he further expects corporate earnings to soar which is additionally the consensus outlook. (Per a note he just put out this week, unlike me, Gerard is less concerned about inflation, particularly of the sustainable variety. He does allow that should unprecedented fiscal and monetary stimulus ignite rapid growth, ending so-called “secular stagnation”, it could be a different story.)

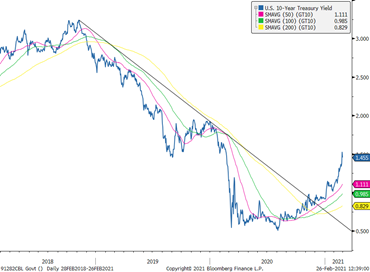

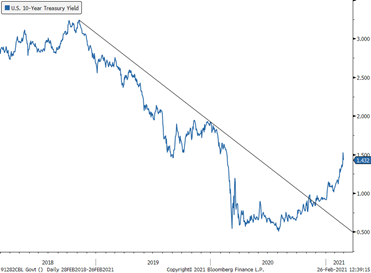

He’s not alarmed by the recent weakness in the bond market which has seen 10-year T-note yields rise from 0.5% to just under of 1.5%, a tripling of yields albeit off of a microscopic level. Moreover, it’s clear that the precipitous downtrend in treasury interest rates since Covid reared its ugly spike protein has now been broken. Thus, even higher yields are a distinct possibility.

Source: Bloomberg, Evergreen Gavekal

Gerard points out that is a normal occurrence when an economy moves from comatose to recovering and then to booming. As short rates stay down—thanks to the Fed—and longer rates rise, this creates the yield curve steepening he refers to; this is a most positive development for financial stocks. These have been ripping of late.

With the Fed committed not to raise rates for years, Gerard, too, sees the economy in “The Sweet Spot”, a phrase he uses twice in this note. Accordingly, he thinks markets could overshoot on the upside. As he concedes, perhaps the overshoot is happening now—or, at least it was happening until the recent sudden meltdown in what I’ve often referred to as the COPS (Crazy Over-Priced Stocks). Per Gerard, the problem is if Fed-head Jay Powell even hints of a slowdown from warp-speed monetary stimulus, markets could do a taper-tantrum 2.0*. Should inflation fears continue to escalate in the months ahead, particularly faster than the oft wrong-footed consensus now believes, he may need to do more than hint.

*The first taper-tantrum began in May of 2013 when then Fed chairman Ben Bernanke implied he might soon taper the Fed’s third round of quantitative easing (QE 3).

The Only Thing We Have to Fear is the Lack of Fear Itself by Gerard Minack

Views on the year ahead are as tightly bunched as I can remember. That’s understandable: no one disputes that 2021 will be a better year for growth than 2020, and no one expects any important central bank to tighten. Everyone also agrees the major macro risk is inflation, but the consensus is that that’s a 2022-or-beyond problem. But these views also drove markets higher last year, and there are clear areas of investment froth. My base case is that overall returns will be positive, but moderate, and the big trade is the shift in relative returns.

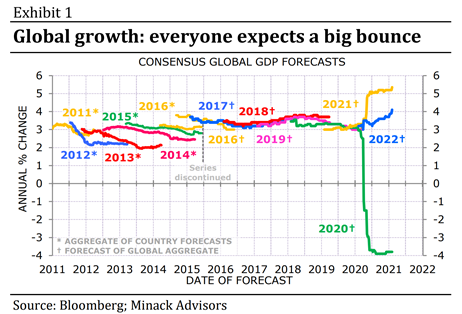

Arguably the most important building blocks for a top-down market view are the outlook for economic growth and the outlook for central bank policy. Unusually, this year there is no debate on the direction of either. After the largest economic downturn in decades, consensus is right to expect a large GDP bounce-back in 2021 (Exhibit 1).

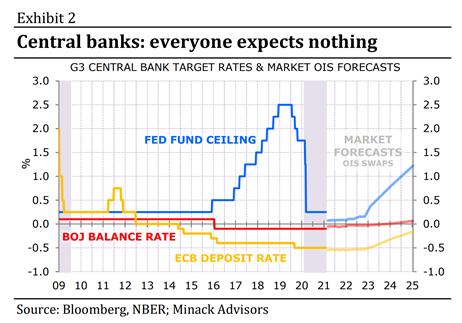

Investors are also right to expect no policy change from any important central bank (Exhibit 2).

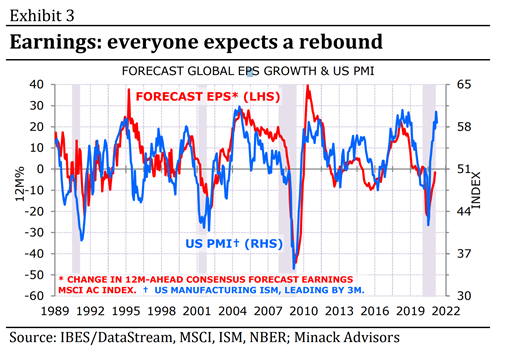

The follow-on points are fairly straight-forward. First, equity earnings will rebound sharply this year (Exhibit 3). Analysts are furiously upgrading EPS forecasts, but this is the stage of the cycle where outcomes nonetheless often exceed consensus.

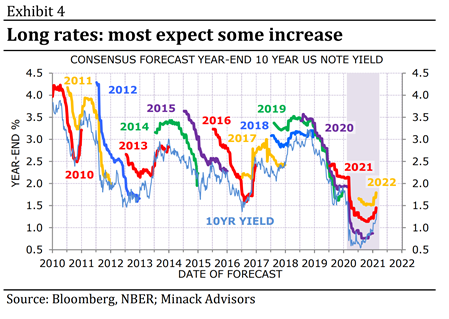

Second, long-end yields should be under some upward pressure. Of course, long rates have not been driven solely by fundamentals for some time, and there is a general view that central banks would step in to damp a rise in long rates that threatened the expansion. So, it seems appropriate that while long-end rates are expected to rise, the extent of the increase is not proportionate to the improvement in the economic cycle (Exhibit 4). With short rates pinned by unchanged policy rates, there’s also a view that yield curves will continue to steepen.

The best gains for risky asset in a typical cycle are when economic growth inflects then accelerates but before investors anticipate policy tightening. This is exactly the mix investors face in 2021. Every model, every historical precedent, says that this is the sweet spot, the stage of the cycle to be long risk.

The only wrinkle in that story is that, clearly, this is not a normal cycle. The better growth/no easing story pushed markets through much of last year. It was turbo-charged by the Pfizer vaccine announcement in November. Global equities had not recovered all their pandemic losses at that stage, since then they have rallied by 24%.

Equity markets normally lead earnings, typically by around 3-6 months. Now, however, global equities have raced ahead of what could reasonably be expected for EPS growth through the next couple of years (Exhibit 5).

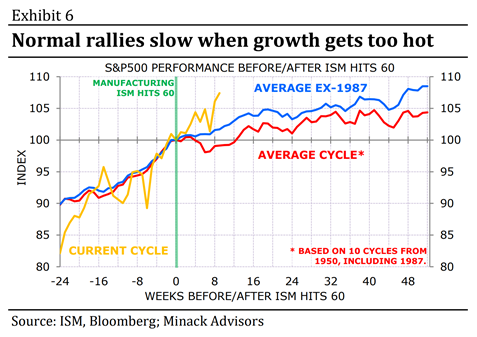

What normally ends the early stage sweet spot is growth running hot enough – say, ISM at 60 – to raise the prospect of policy tightening. This does not end the equity rally, but the pace of gains tends to moderate, and volatility increases (Exhibit 6).

This is effectively my base case for 2021, moderate gains for equities overall, but the bigger story is the rotation within equities.

The bull risk to my view is that the sweet spot remains sweet. Whenever investors anticipate better growth ahead – and the second half should be a cracker in many developed economies – without any threat of central bank response, equity gains may remain fast-paced. Ultimately this would prove to be an overshoot, but that’s what markets do.

Markets have already proved themselves impervious to news I thought may have tripped them up. That news included the (now receding) crescendo of infection through the last quarter of 2020; the discovery of new Covid-19 variants; renewed lockdowns with resulting macro weakness. To take the US as an example, I would ordinarily have expected equities to worry just a little about three consecutive monthly declines in retail sales and a three month stall in non-farm payroll growth; they have not.

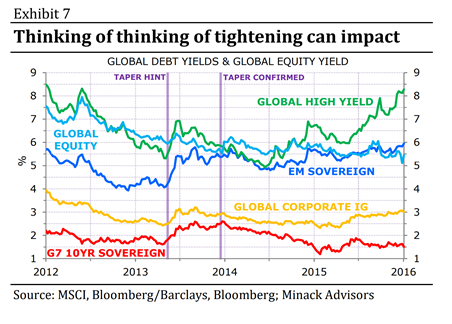

So perhaps the overshoot is on. If it is – and, as ever, I never make tactical calls with much conviction – then the prospect of a second half correction would rise commensurately. Bubbles are sensitive to even small pricks. What happens when Jay Powell says he is ‘not thinking of tightening’, instead of ‘not thinking of thinking of tightening’? When Ben Bernanke merely raised the prospect of tapering the Fed’s QE buying it caused a serious market set-back in 2013 (Exhibit 7). In short, I still think 2021 will end with only moderate returns.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.