“As we are now experiencing a pretty irrational time due to central bank money printing/price-keeping operations, the next bear market will likely start with passive managers being unable to sell overvalued shares.”

– Charles Gave

An Up-Beat View From Down Under by David Hay

One of the main goals of this newsletter is to examine both sides of a particular issue or viewpoint, be it on the economy, financial markets, or even the pros and cons of artificial intelligence (AI). Admittedly, this can be challenging in the case of the former two topics after a seemingly eternal up-cycle. But, in this EVA edition, we are giving it our best effort – with a hefty assist from our guest author.

As discussed numerous times in prior EVAs, the current environment reminds me very much of twenty years ago, during the most overheated days of the late, ultimately not-so-great, tech bubble. Of course, there are, as always, a plethora of variances. One is that the US federal government is hemorrhaging red ink these days whereas in 1999 bulging surpluses were accumulating (feeling nostalgic yet?). Productivity, the essential ingredient for growth in a graying society, was in a powerful uptrend versus this decade’s depressing downslope. Also, the stock bubble at the time was almost exclusively confined to anything and everything tech-related whereas during this go-around there has been a lengthy list of mini- and maxi-bubbles, both in and outside of the stock market.

Yet, even though 1999 eclipsed 1929 as the biggest speculative American stock market frenzy of all-time, its demise produced more winners than losers during the first two years of the bear market that ran from Q1 of 2000 until Q2 of 2003. It’s remarkable how well most non-tech stocks did, until the summer of 2002 when nearly all equities were body-slammed. (The next bull market didn’t start, in hindsight, until April, 2003.)

For instance, the Vanguard value index mutual fund rose by 4% from February of 2000 until April 1st of 2002, even as the S&P itself slid by 13% and the NASDAQ did a 60% power-dive. Yet more dramatically, the equally-weighted S&P 500 index, in which the smallest company has the same value as the largest, actually rose by 22% over this same time frame. (Unlike today, at the end of the 1990s, small cap stocks were generally unloved and undervalued, setting the stage for that dramatic out-performance.)

The problem was that most investors were much too heavy in growth in early 2000, especially of the large cap variety, and much too light on value areas like financials, MLPs, utilities, REITs, small cap non-tech, and industrial stocks. (By the way, a recent EVA gave a timely tout on one of these but to avoid the jinx effect, I won’t mention which one…not that it will be too hard for EVA readers to decode).

This month’s Guest EVA, from the exquisitely talented Gerard Minack, author of the Down Under Daily, is calling for yet another up-year in the longest bull market ever (once again, referring to the US; collectively, overseas stock markets have essentially gone nowhere over the past 12 years). Yet, as you will soon see, he’s particularly positive on the long-lagging value sector plus emerging markets and Japan.

This synchs with Evergreen’s optimistic case for next year, a twist on the Great Rotation meme that was supposed to signify a massive shift out of bonds into stocks, a possibility Gerard is allowing for next year. (Evergreen’s bear case is a full-blown recession that ends the longest bull run ever with a base case for a mild downturn that wounds but doesn’t kill the bull; this old guy worries that the bear scenario is much more than a low-probability event.)

Based on Gerard’s hopeful thesis, the revival by the long-neglected value stocks will more than off-set any correction in the growth sectors. However, he is also noting that with secular stagnation still the dominant economic condition (i.e., sub-par GDP growth in the developed world and not a whole lot better in the developing countries), he doesn’t think long-term bond yields will rise significantly. That also jives with Evergreen’s view. Last year showed how the world begins to crumble once 10-year US T-notes yield over 3%. Since then, the planet has added many additional trillions in debt making higher rates even more problematic. Specifically, the world’s debt-to-GDP is 20% higher now than it was 12 years ago during what was the biggest credit bubble ever seen—up to that point.

Also, as Gerard rightly highlights (his Exhibit 6), the P/E ratios on growth stocks worldwide have dramatically detached from those for value shares. Though he doesn’t say so, there is little doubt in my mind this is a function of the trillions flowing into passive ETFs and mutual funds that, generally, are forced to keep adding most of their assets to the in-vogue mega-cap stocks. It’s those issues which have been driving this market for years, especially in America.

As a result, in the US, the top 10 companies in the S&P now amount to 24% of the total market value. This is down a few percentage points from the nuttiest levels of 1999/early 2000, but it is nonetheless a highly dangerous concentration in a handful of popular names. (Admittedly, Evergreen owns several of these but we have been systematically taking profits on them.)

He further logically observes that there is a connection between the staggering outperformance of the US market vs the world and tech stocks vs the rest of the market. The S&P 500 has roughly a 90% correlation, or linkage, with tech. Thus, when technology issues are on a roll, the S&P almost always is, too, as it has been for so many years. Then, almost by definition, the US will also be the MVP among global stock markets.

A close study of market history reveals that it’s very, very challenging for a sector, like tech, and a market, like the US, that has dominated for the prior decade to maintain that outperformance over the next 10 years. And yet, with millions of investors plowing trillions into index vehicles, that’s exactly the bet they’re making. As was the case twenty years ago, it’s likely to be a very costly wager, similar to betting on the most popular asset class of 2017. Lest you forget, that was Bitcoin and the other crypto currencies. As they say a picture is worth a thousand words…and perhaps warnings, too.

Source: Bloomberg, Evergreen Gavekal

Source: Bloomberg, Evergreen Gavekal

The Risks in 2020 Seem Evenly Balanced by Gerard Minack

I am upbeat on next year. Worryingly, it seems that so are most other people. Even so, I see the risks around my moderately upbeat base-case as evenly balanced, not slanted to the downside. Some thoughts:

Politics is an obvious – and likely, persistent – uncertainty for investors. It’s easy to list downside political risks: Trump (let me count the ways...); trade; Brexit (both the UK leaving, and someone leaving the UK); China (let me count the ways...); the political backlash against big business; climate change; etc. Two points on this:

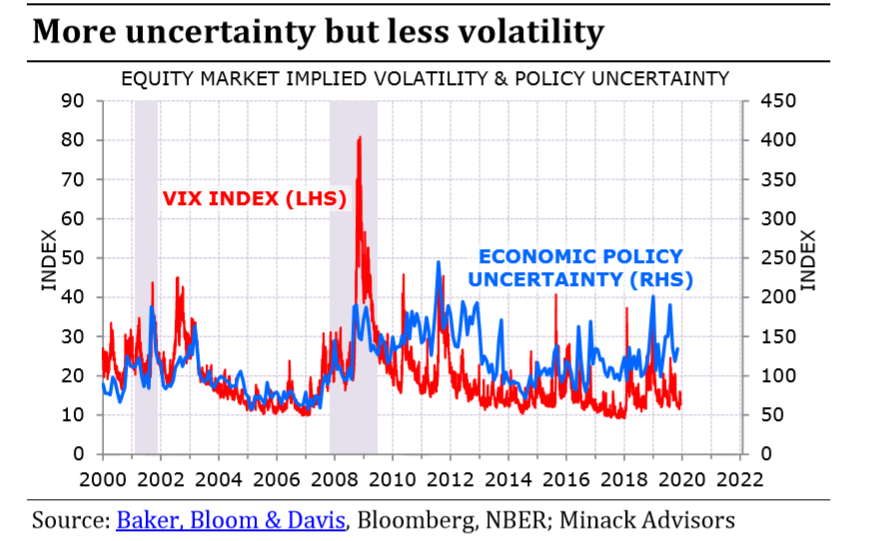

First, investors appear largely unfazed by politics: implied volatility in financial markets remains remarkably low relative to political risk (Exhibit 1).

Exhibit 1

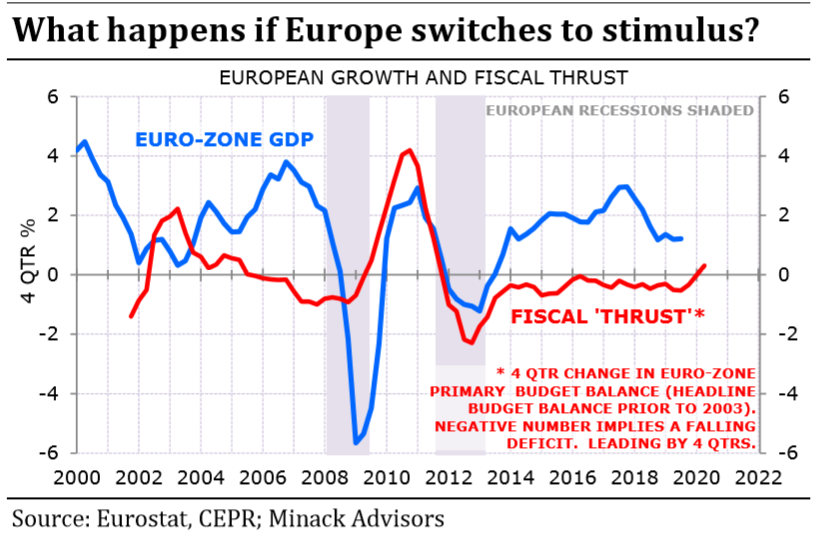

Second, I think there’s at least one upside risk: that fiscal stimulus is dialled up. The most likely candidate is Europe, and it could go hand-in-hand with an upside growth surprise (Exhibit 2).

Exhibit 2

A second risk is a perennial: that 2020 is the year the US hits inflation-boosting capacity constraints. The key capacity constraint is labour. The labour market is working in that wage growth has increased as unemployment has fallen (Exhibit 3).

Exhibit 3

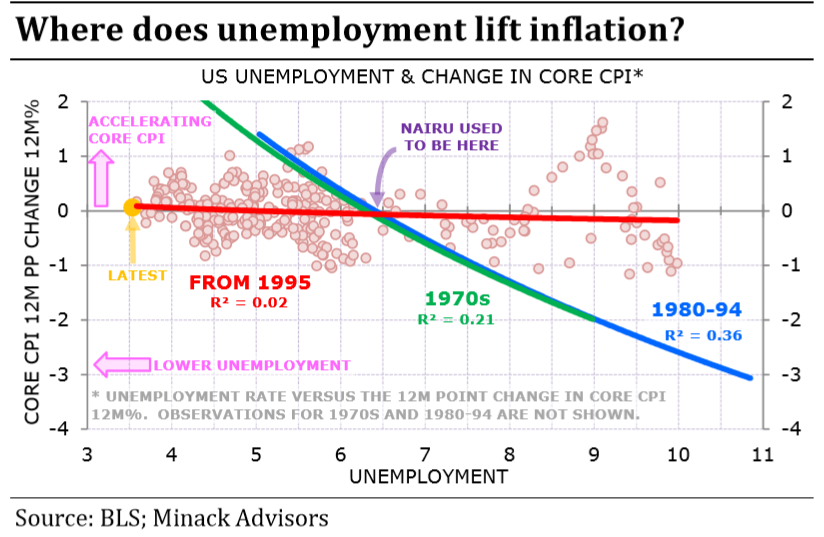

What has stopped working is the link between unemployment and inflation (Exhibit 4). I am like most: I think there has to be a level where unemployment is low enough to push up wages fast enough to generate inflation. This cycle has proven that we don’t know where that level is, but I think hitting it will be a bigger risk in 2021 than 2020. I appreciate that inflation is a risk more discussed than hedged. It would be big if it happened.

Exhibit 4

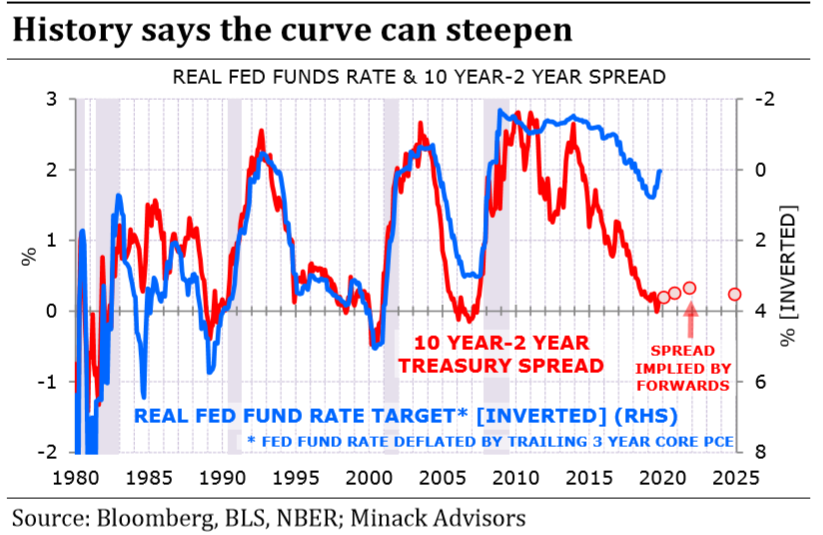

What is clear – and is part of my base case – is that the hurdle the data need to jump to get central banks to tighten is now very high. Pre-emptive policy is dead; central banks will only tighten when inflation is rising, and not before. This points to a steeper yield curve. My base case is that the US 10 year heads towards 2½%. But there is a risk of overshoot: historically low policy rates are associated with steep yield curve. The curve now is very flat given current real short rates (Exhibit 5).

Exhibit 5

Just as there is an upside risk to bond yields, I think there is also upside risk for equity valuations. Some modest re-rating is part of my base case for 2020. But the re-rating could be surprisingly strong. Exhibit 6 shows a simple 3-factor model for US equity valuations. It effectively suggests that conditions are as propitious as they ever have been for equity valuations. The model incorporates the fact that very low rates are detrimental to equity valuations, so a modest rise in long-end yields would be supportive for a re-rating.

Exhibit 6

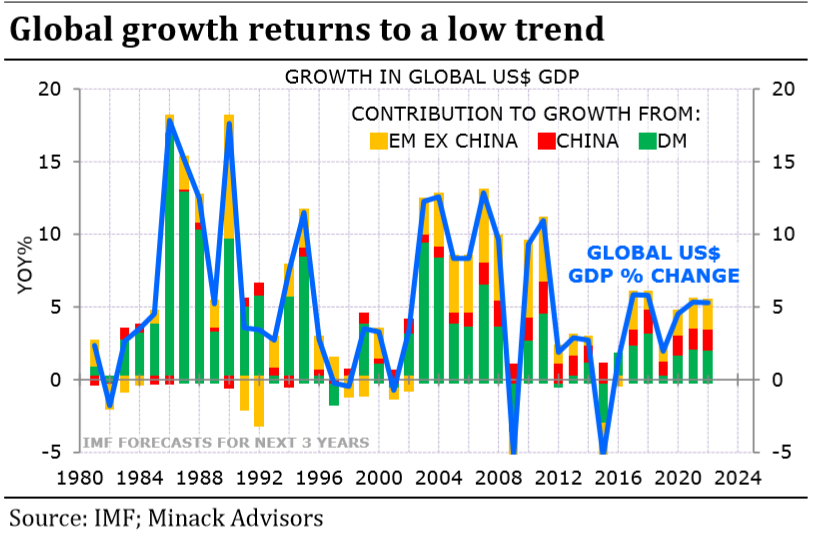

I broadly agree with the consensus view that global growth will accelerate in 2020, but only to around what seems to be a low trend rate (Exhibit 7, which includes IMF forecasts). I am relatively confident that growth will improve in the developed economies. All the set-backs for developed economies in this cycle have been self-inflicted. If policy is kept easy – both fiscal and monetary – then growth should be reasonable.

Exhibit 7

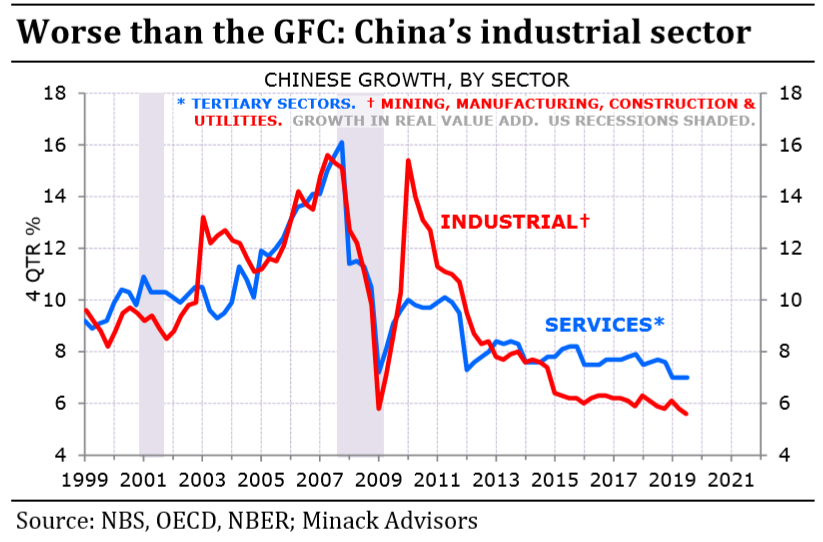

There are more risks amongst emerging economies. China remains a concern. Industrial sector growth is weaker now than in the GFC nadir (Exhibit 8).

Exhibit 8

Chinese policy makers are boxed in by several factors: 1) inability to boost consumer/service sector activity to fill the gap left by the structural slowdown in industrial sector activity; 2) stimulating growth via additional capex risks adding further excess capacity; 3) pushing the corporate sector to invest more risks adding to excess leverage; and 4) the global environment is more challenging, economically and politically. This is a backdrop where even a moderate shock could test China’s macro resilience.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.