“Trade wars aren’t so bad.”

-DONALD TRUMP

“There is no winner in a trade war… A trade war will only bring disaster to China, the U.S. and the global economy.”

-China’s trade minister, ZHONG SHAN

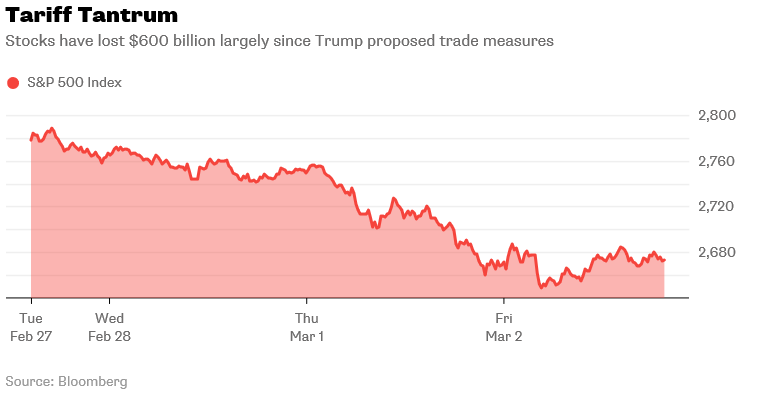

The Trump Trade Tirade. In an echo of the early February market meltdown, panic unexpectedly shook markets as President Trump unleashed the opening salvo in his war on trade at the end of last month. Bloomberg even went so far as to dub the pull-back a “Tariff Tantrum” in an ominous ode to the Taper Tantrum of 2013.*

*The Taper Tantrum refers to the 2013 surge in U.S. Treasury yields, which resulted from the Federal Reserve’s use of tapering to reduce the amount of money it “fed” into the economy.

But what started out as a forceful gust of wind with the potential to transform into a hurricane has at least temporarily turned into nothing more than the passing of a springtime storm. The tariffs – 25% on steel imports and 10% on aluminum imports – will exclude NAFTA (North American Free Trade Agreement) partners Mexico and Canada, and will also allow provisions for other countries to appeal the tariffs on a case-by-case basis. As one senior Trump administration official told reporters on March 8th:

“Any country with which we have a relationship [can] discuss with the United States and the president alternate ways to address the impairment of our steel and aluminum industries…This administration has the ability to modify the order.”

Despite these concessions, tensions between the US, European Union (EU), and China have continued to mount. On Monday, the EU kept its offensive tone as Dutch Finance Minister Wopke Hoekstra stated that “Europe is prepared,” while Trade Commissioner Cecilia Malmstrom said, “We are not afraid, we will stand up to the bullies.” Chinese trade minister Zhong Shan conceded that China doesn’t want a trade war but kept an aggressive stance by relaying “[China] can handle any challenge and will firmly defend the interests of our nation and our people.”

So how worried should investors be that this political bullying will turn into something more calamitous?

Using history as a guide, all-out trade wars prove to be devastating and this recent shift is a clear departure from trade policy that has held precedent for over 80 years. The most prominent trade war of the 20th century was ignited by the Smoot-Hawley Tariff Act of 1930. The results were so disastrous that the trade war prolonged the Great Depression, contributed to the rise of Nazis and other fascist leaders, and sank US exports by 61% from 1929 to 1933 before being repealed in 1934.

The initial public outcry, coordinated global response, and swift market pull-back caused by the tariff tantrum all foreshadow the possibility of a similarly disturbing reality should Trump’s protectionist push turn into a series of Mayweather-like blows.

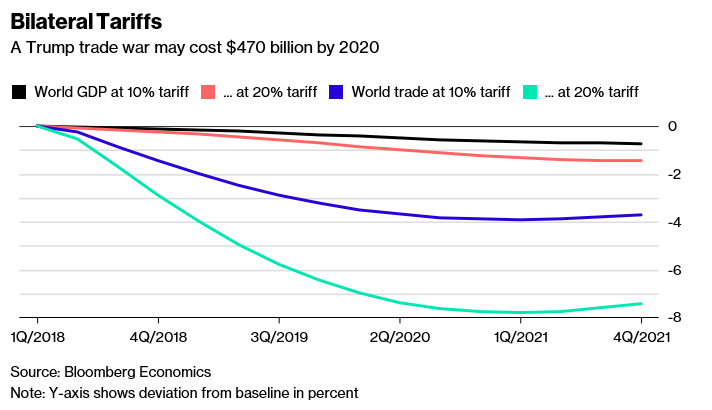

If rhetoric turns into policy, inflationary pressures would continue to build, already tense relationships among trade allies and foes would escalate, and it could cost the global economy a whopping $470B by 2020 as the chart below shows.

However, in the midst of all the antics and political strong-arming coming from the White House and other nations globally, it’s important to remember the true target of Trump’s trade tirade: China.

Bubbling Below the Surface: An Economic and Technological Cold War The chief goals of Trump’s protectionist ambitions are to limit China’s influence on bilateral trade and ensure the US has an upper-hand on critical technologies. China currently accounts for half of the US non-oil trade deficit and, while Trump’s initial tariff tantrum missed the mark on curtailing this deficit, it’s likely that subsequent tariffs will directly target China.

The more important long-term outcome of recent trade-related events is that the White House is working to ensure “America First” rhetoric translates into concrete policy around foreign-controlled technologies. This week’s swift rejection of Singapore-based Broadcom’s hostile takeover efforts of Qualcomm sent that message loud and clear. In a release sent from Washington on Monday evening, Trump stated: “There is credible evidence that leads me to believe that Broadcom [by acquiring Qualcomm] might take action that threatens to impair the national security of the United States.”

This marks the fifth time since 1990 that a takeover of an American firm has been blocked on grounds of national security. Two of those blockages have come under President Trump over the last six months. Additionally, several Chinese-related deals have been killed since Trump took office:

The main takeaway here is that Trump and his national security team are gearing up to take down any takeover attempts that give China an upper hand technologically.

The challenge up to this point has been defining specific policies that inflict real pain on China without causing equal or greater harm to US companies. Trade sanctions will likely incite retaliatory tariffs, and controls on Chinese technology investments might encourage Beijing to double down on its already huge investments in technological self-sufficiency. There is also a plausible risk that China will retaliate by selling a portion of its vast US treasury debt holdings, putting further upside pressure on already rising US interest rates.

Despite these risks, it’s pretty clear that Trump has come to play hardball with Beijing. The next round of trade sanctions will likely focus entirely on China, and be levied under section 301 of the Trade Act of 1974 for penalties of IP theft and technological crimes.

The jury is still out on the economic repercussions of such actions, but the purpose is clear: Washington is gearing up to take on Beijing in the fight for technological supremacy. When two titans fight, the world tends to shake. Yet, with so many asset classes priced for perfection there seems to be precious little margin-of-safety to insulate investors should these initial skirmishes escalate into a full-blown trade war. Let’s hope cooler heads prevail.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.