“Prepare for the unknown by studying how others in the past have coped with the unforeseeable and the unpredictable.”

– US General George S. Patton

After a cataclysmic hiccup in March, markets rebounded with a vengeance in the second quarter of 2020. In fact, the Dow closed out its best quarter since 1987 on Tuesday, while the S&P and Nasdaq had their best quarters since the late-1990s. Several tailwinds, including fiscal and monetary stimulus, economic re-openings, and positive virus-related news, all combined to drive stocks higher in the quarter.

This week, we are presenting the first part of a three-part series from Louis-Vincent Gave on the possible explanations for the impressive rally. Specifically in this edition, Louis dissects the premise that reopening the economy and returning to “life as usual” will lead to “more of the same” (i.e. sustained growth similar to what we experienced prior to the pandemic). Without spoiling the ending, Louis leaves room for two further explanations for the ferocious rally: (1) that investors have taken leave of their senses, or (2) are acting on the premise that cash may become worthless in the coming years. We’ve discussed both of these possibilities in recent newsletters (see No Revenue, No Profits, No Problem?; Bubble 3.0: End Game (Part II)), and since we believe these are vital topics to consider, we will be presenting Louis’ subsequent missives to readers in upcoming newsletters.

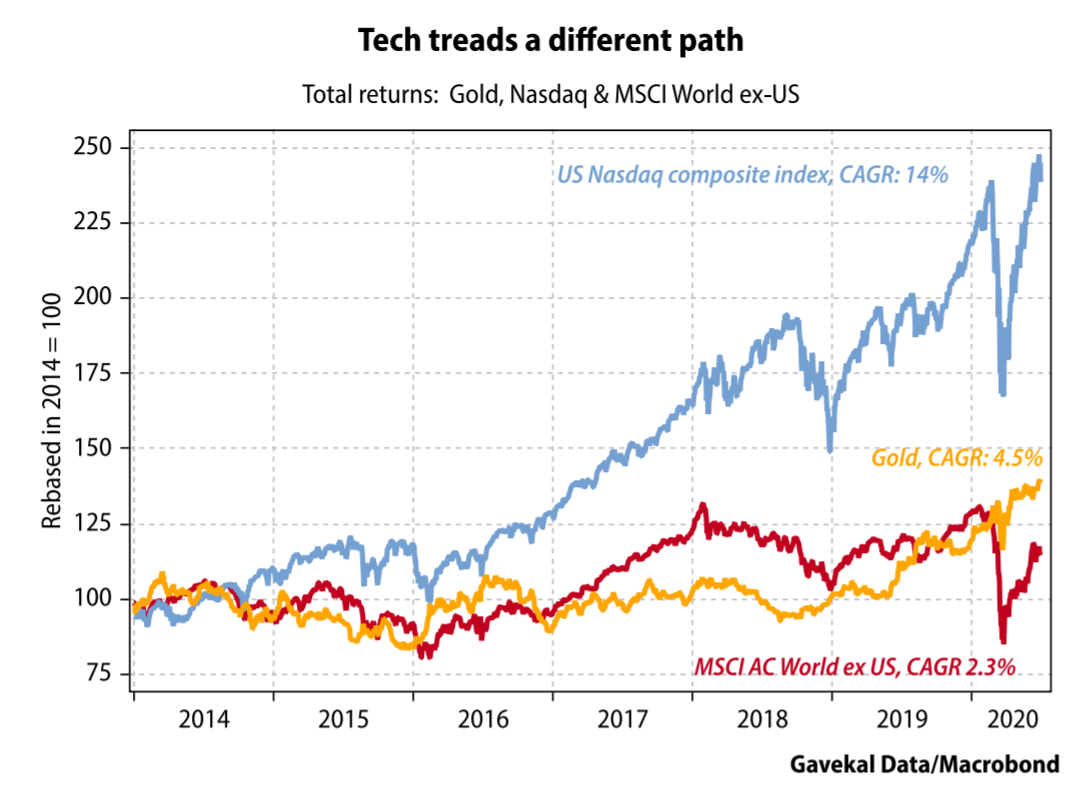

The rally in global equities since mid-March has wrong-footed most investors who were convinced that the threat of a record economic contraction would condemn equity markets to struggle for the foreseeable future. Yet most of the losses incurred in February and March have been made back and the leader of the previous bull market—US tech—has gone on to make new highs.

Confronting this impressive rally, investors have been forced to come to one of three conclusions:

Equity markets are pricing in a return to ‘more of the same’

After Lehman Brothers failed in 2008, the global economy ground to a halt. Banks stopped lending to each other, global trade cratered and money market funds broke the buck. In developed markets, policymakers were initially slow to respond but then cut interest rates to zero and beyond in some cases. Banks were back-stopped. The US adopted a US$850bn plan for “shovel ready” projects. China squeezed a decade’s worth of infrastructure spending into a few years. In time, growth rebounded, but remained lackluster. Inflation stayed low. And the US dollar was well bid. Against this macro background, equity markets started to rebound and embarked on a decade-long bull market, especially in the US.

With the Nasdaq having recorded a new high last week, markets seem to be pricing in a continuation of the above environment (mediocre global growth, low inflation and a strong US dollar). In light of activism by the Federal Reserve and other central banks, investors seem to think they have “seen this movie before”, with a plot that runs along the following lines: a crisis unfolds, spurring the Fed and other central banks to slash rates and ensure the survival of zombie companies. The result is an environment of weak growth and low inflation around the world, even as the US does better than the rest. Thus, the US dollar stays bid and interest rates remain low, which means that valuations hardly matter. Ergo, buy growth where you can find it.

And sure enough, if macro conditions in the next decade match those of the past decade, why should we expect a different outcome from that of the pre-Covid world? In such a scenario, the best portfolio would continue to be one built around US growth stocks and US treasuries.

Unfortunately, a fairly safe rule of thumb is that sequels are seldom as good as the original movie. And the foundations on which the above scenario rests may well prove to be shaky.

Foundation #1: We have seen this movie before

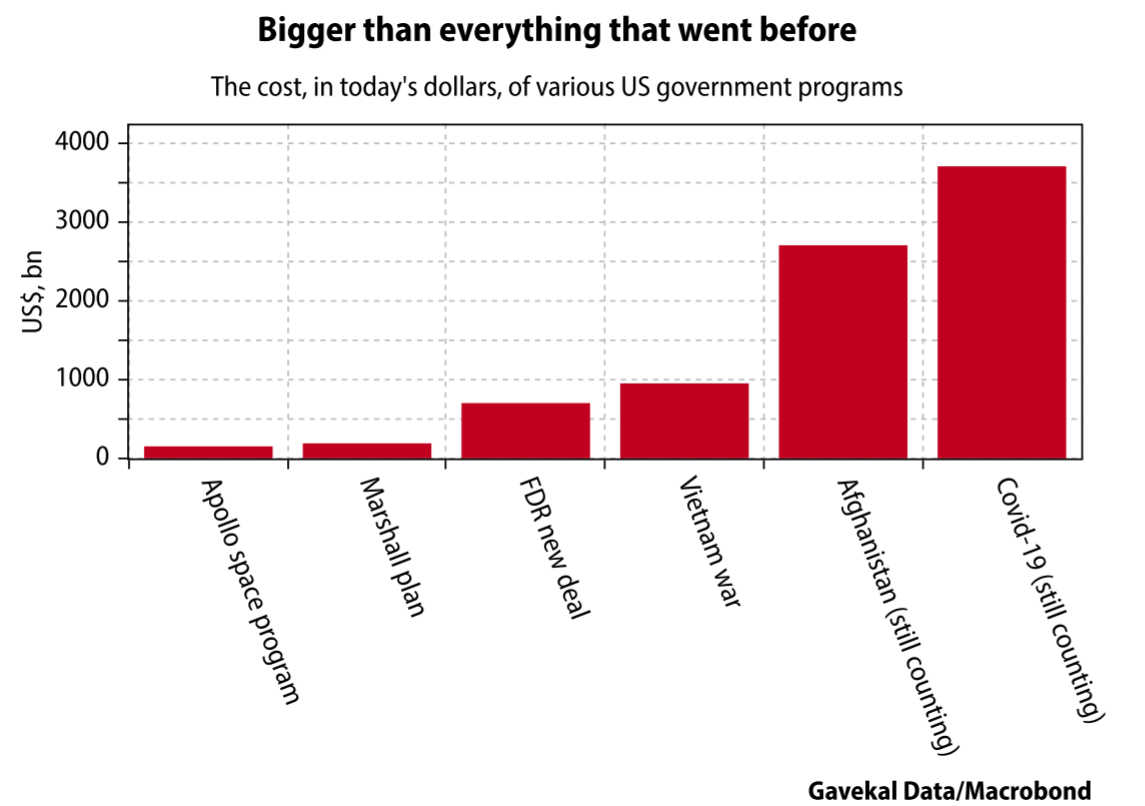

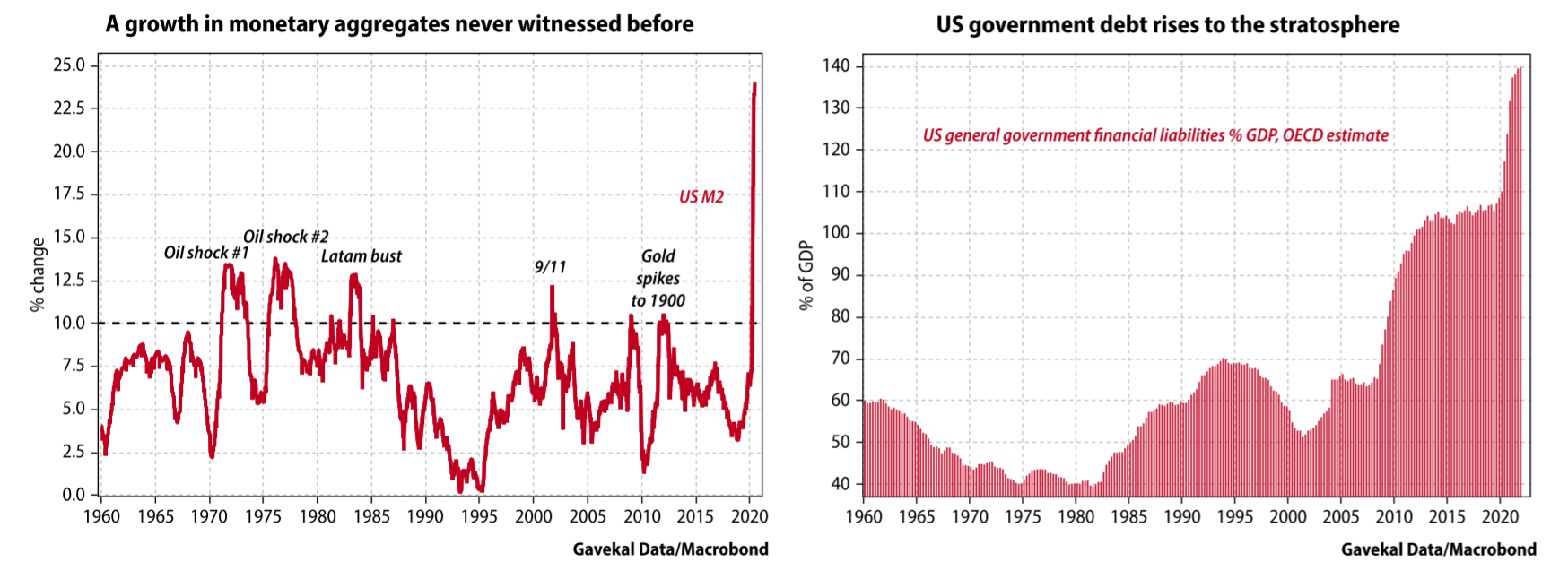

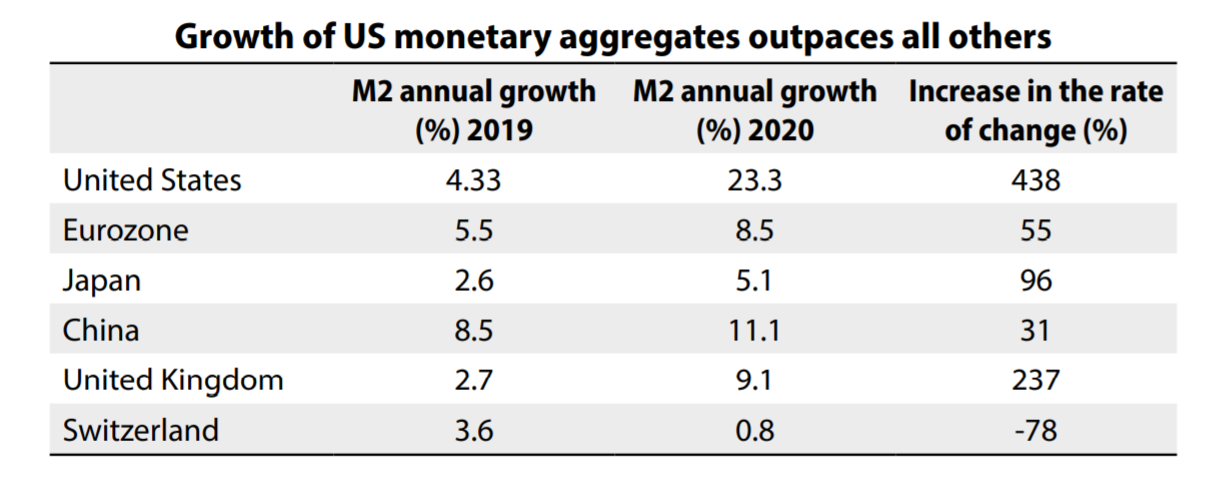

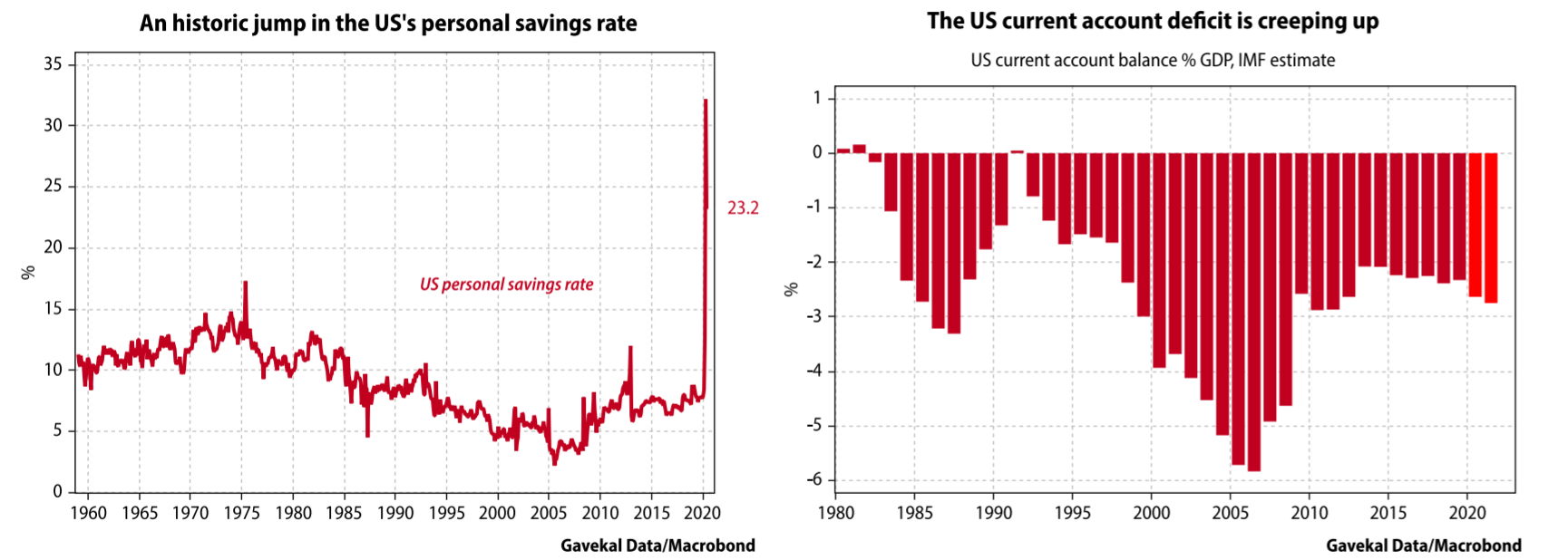

It is easy to poke holes in the argument that current conditions match the post-2008 environment. For starters, the collapse in economic growth across the globe is unprecedented; as has been the policy response. To illustrate what “unprecedented” means, consider the following charts:

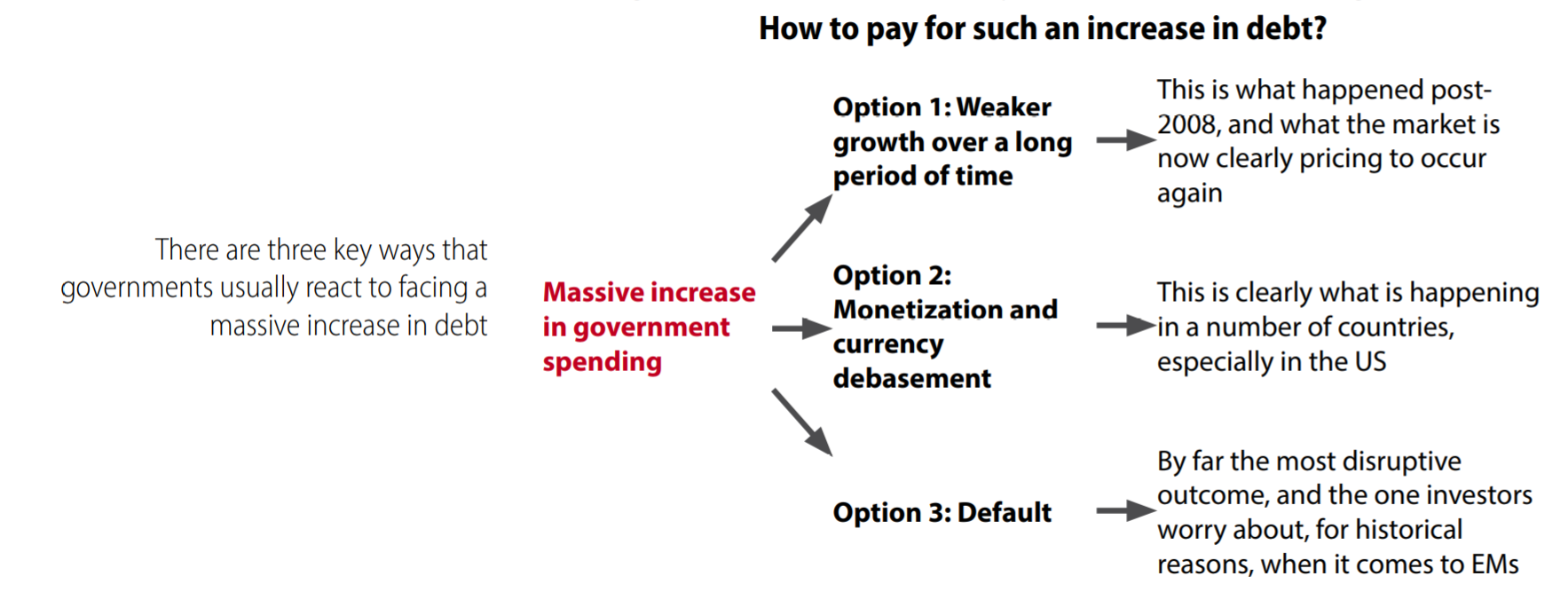

This brings me back to the question of whether the post-Covid-19 macro environment will be—as markets are now pricing in—broadly similar to the post-2008 crisis environment. When confronting a surge in government debt, investors have to assume that it will either be paid for through (i) lower future growth, (ii) massive currency debasement, or (iii) outright default.

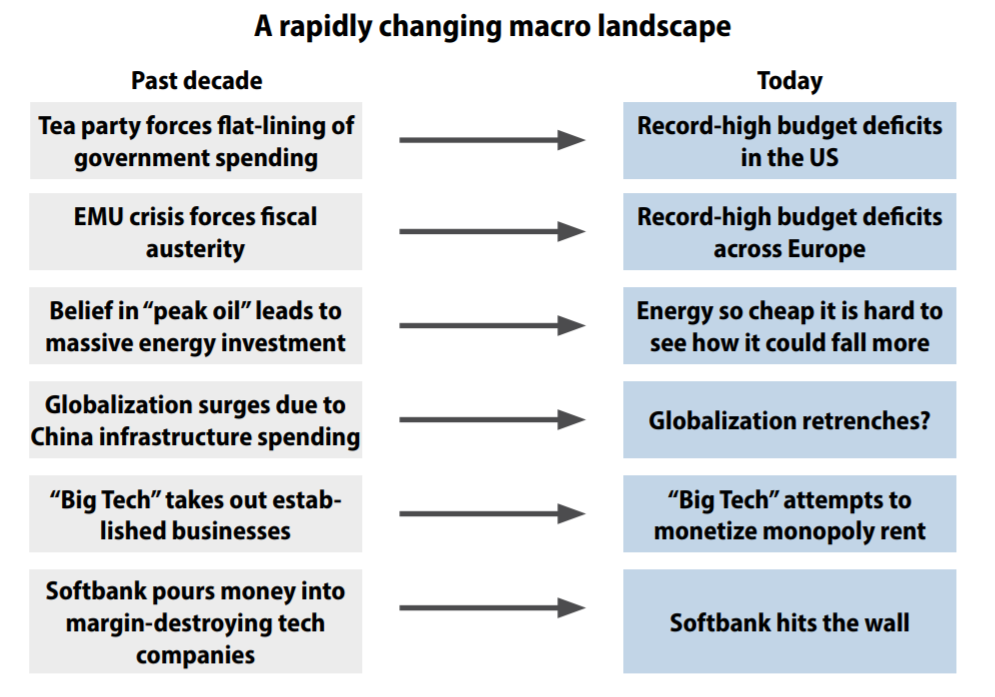

After the 2008 crisis, policymakers embraced option 1. In the US, the Tea Party took control of Congress and froze government spending for six years. In Europe, the 2011-12 eurozone crisis unleashed fiscal austerity. In China, the arrival of Xi Jinping to power in 2012 witnessed the start of a significant anti-corruption drive that froze spending on many projects.

Fast forward to today and the past is now another country. Fiscal austerity is as passé as the Harlem Shake. Thus, when it comes to fiscal policy, the current sequel already encompasses a significant plot twist to the original movie.

Foundation #2: The US will remain the cleanest dirty shirt

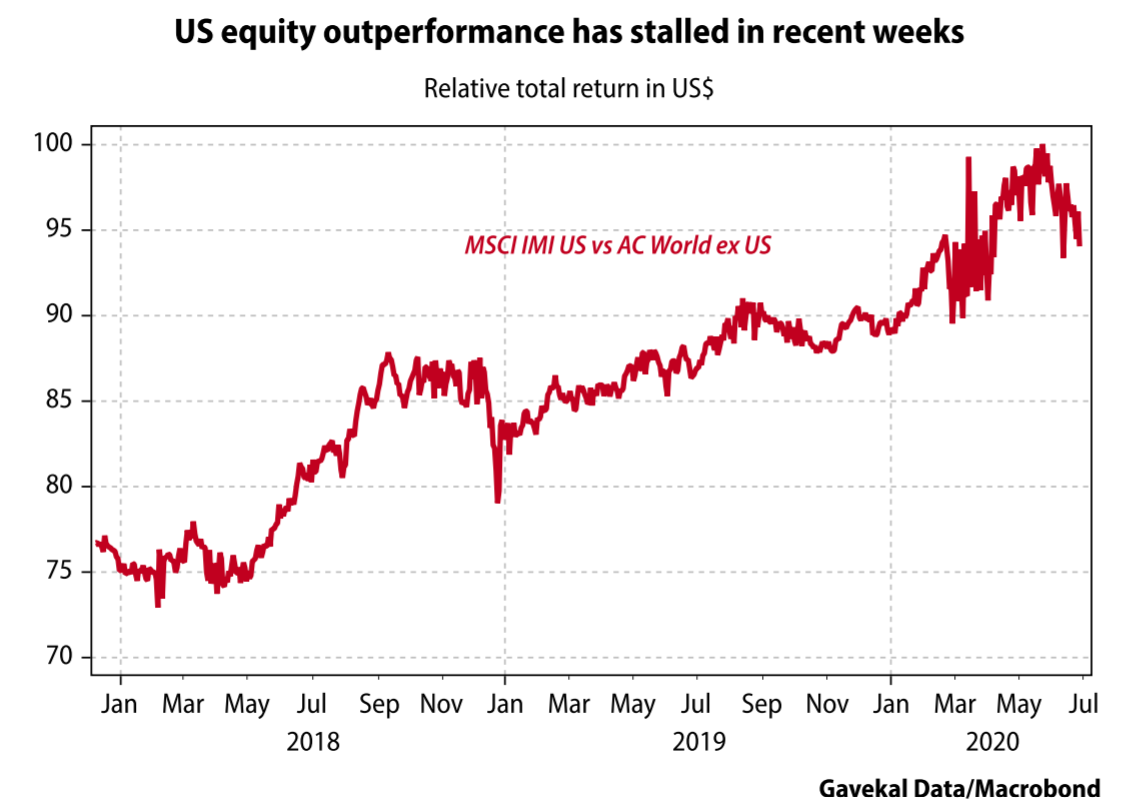

Given recent street riots, the continued rise in Covid-19 cases and the uninspiring choice that US voters face on November 3 (a choice as to who can spend the most unearned money fastest), the perception of the US being the world’s “cleanest dirty shirt” may be shifting. As a Canadian friend recently put it to me “living in Canada today feels a little bit like having an apartment above a crack-den”. Notwithstanding the Nasdaq making new highs, this spate of bad news may explain why since May 22nd, the US equity market has underperformed MSCI World (ex-US) by about -5%.

Such near-term underperformance may seem trivial given the US market’s massive outperformance of the past decade. Still, the fact it is occurring during rising markets and at a time when US retail investors are especially pumped up on “animal spirits” makes it noteworthy.

Unquestionably, the uncertainty of the political situation and the lack of clarity on the tax policies of a potential Biden administration, will likely be a Damocles sword over the head of US equity markets for months to come. And this at a time when policy risks in Europe, Japan and China seem to be abating. But beyond the short term back and forth of relative policy choices, a more important question is whether, after weeks of riots, the US still stands aloft as the “shining city on the hill” that President Ronald Reagan would frequently reference. In Clash of Civilizations, Samuel Huntington reduced humanity’s history down to the history of nine major civilizations, each finding its root in a distinct religion. Of these, Western civilization was founded on Judeo-Christian principles and on the importance of individuals acting within a framework of the law. Anyone who has ever read the New Testament gospels will quickly come to the conclusions that:

These beliefs made Western civilization unique in supporting societies where the law protects individuals against the state, which otherwise can inflict violence within its borders (the police and courts) and outside of them (through an army). Meanwhile, all other civilizations were founded on the dominance of the group over the individual, and on the necessity of an individual’s needs coming second to the community’s welfare.

This much is evident in the first words of the US Declaration of Independence: “We hold these truths to be self-evident, that all men are created equal, that they are endowed by their creator with certain unalienable rights, that among these are life, liberty and the pursuit of happiness”. From there, the US constitution is one long exercise in constraining the power of the state to prevent the abuse of power, nepotism and corruption.

It was this unprecedented exercise in putting the law above the state, and the individual above the community that set the US on its historically improbable path. Hence, for Western civilization the law can only apply to individuals and it is supposed to be the same for everyone. In practice that has not always been the case, but it is what we, as a civilization, have aspired toward.

Following the birth of the US and later through the emancipation of slaves and civil rights movement, we saw the emergence of a society where:

If the creation of the US was the pinnacle act of Western civilization, the foundation stone was abandoning “collective responsibility” and “collective punishment”. Unlike the other eight civilizations in Huntington’s book, the West dictated that the son cannot be responsible for the crimes of the father, nor the sister for the brother. Alas, history, as well as current events, show these principles are not always upheld. Yet the fact that we as individuals err reflects poorly on us rather than the goals. They remain the founding cement on which our civilization rests.

Whenever Western countries have departed too far from these goals (France imposing huge reparations on Germany after World War I and so making Germans collectively responsible for the Kaiser’s actions), disasters have usually ensued. The idea that a certain group of people can be held accountable for a historical crime (for example, Jews for Christ’s death) is pernicious and invites disaster. This is all the more so when a crime occurred generations ago and the people today had no part in it. In short, American strength has rested on a belief in individual responsibility over collective punishment. It is an idea embedded in the American psyche, which in times of crisis meant that the US always ended up being the “cleanest dirty shirt”.

But is this belief coming under attack in the US? To answer this question, we need to take a detour to France for, along with fine wines, luxury goods, and airplanes that do not fall out of the sky, France has come to dominate the niche market of exporting bad ideas. In the Paris of the 1960s, a new philosophical approach to justice was born by the likes of Jean-Paul Sartre, Michel Foucault and Jacques Derrida. With deep roots in Marxist theory, they argued that history emerged from a struggle between the oppressed and oppressors. The justice system was the creation of the “oppressor” class that seemed to mostly comprise white males acting to oppress females and the African and Asian populations. With this frame of reference, it makes sense for the oppressed to reject institutions which at their core are criminal.

Like a parasite that does not want to die, the idea of “collective responsibility” has been reintroduced during recent US protests. It is troubling that so many Americans have insisted on “collective blame” as one policeman’s criminal actions spur widespread calls to “defund” the police. Suddenly, all policemen are guilty by association. Just as all white Americans (even those that immigrated this year) must account for the stain of America’s past use of slaves.

To this non-American observer, the threat emanating from recent riots was not so much to life and property as to American society being split about the very concept of “justice”. If anything made America the world’s “cleanest dirty shirt”, it was the belief that an individual could have his day in court, where he would be judged on merit and only have to account for their own crime.

Attempts to adopt the concept of “collective guilt” and “collective punishment” may amount to nothing. Still, one has to acknowledge this is a new risk for the US and Americans are no longer united on the concept of what justice means.

Foundation #3: Tech is the only place to find growth

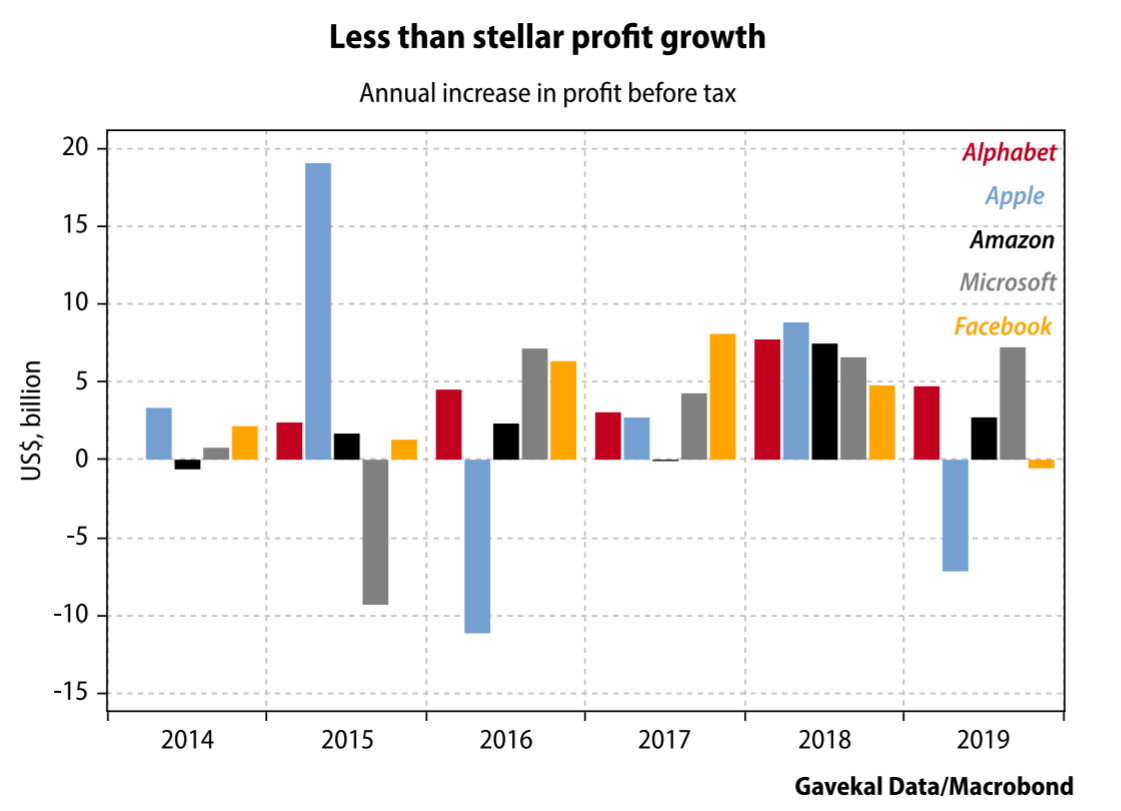

In recent years, big US tech companies have delivered growth on a scale rarely seen before. Since 2014, Alphabet has increased annual pre-tax profits by US$4.5bn on average, Facebook by US$3.7bn. Admittedly in 2019, both Apple and Facebook fell far below the average performance of recent years, Alphabet and Amazon performed in line with the average of recent years and Microsoft hit the ball out of the park. Hence, for all the talk of “FAAMG” being the only segment guaranteeing growth, it should be noted that two of the five failed to grow profits in 2019. This is somewhat ominous given that the environment in 2020 is far tougher.

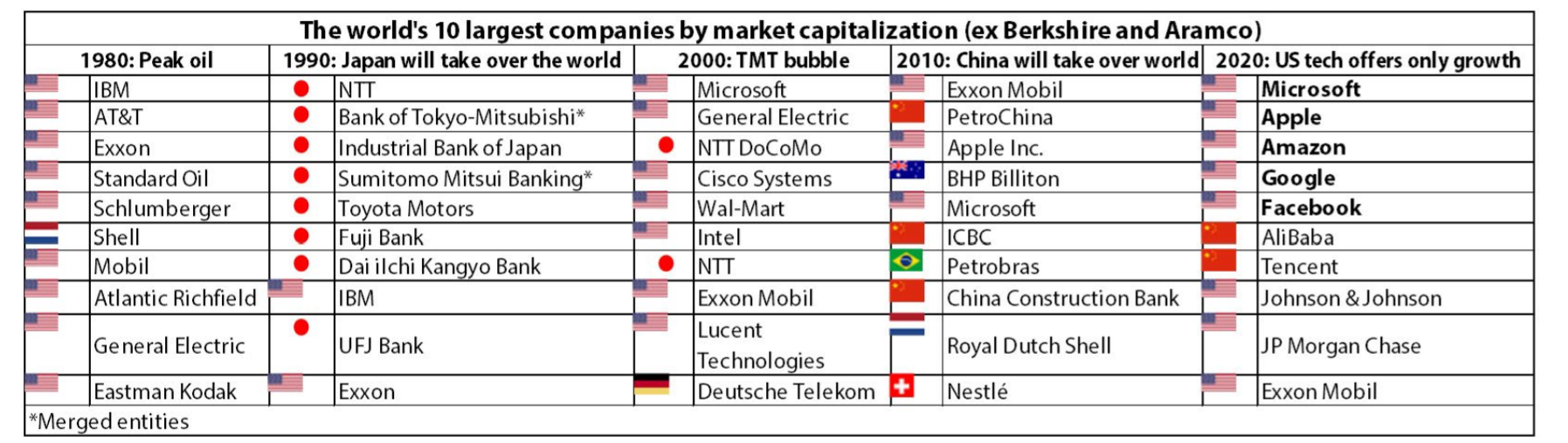

The obvious challenge that Big Tech firms face in delivering growth is their size. Growing at 30% a year is one thing for small and nimble firms; it is a different thing for a behemoth. In nature, very big animals (whales, elephants, Charles) tend to move slowly and the same is typically true of companies. History also suggests that the idea of growth only being found in technology could unravel faster than investors expect. In this regard, consider the table overleaf showing shifts in corporate leadership across the decades.

One challenge for very big companies is that in order to keep growing they eventually must capture someone else’s market. Such action tends to unleash expensive competitive warfare or, alternatively, trigger a regulatory backlash. In the case of Apple, operating profits peaked in 2015 at US$71bn and the lack of a new “must have” product has seen profits subsequently broadly stagnate.

Confronting this lack of growth, Apple is increasingly forced to “scrape the barrel” in a bid to justify an ever-expanding stock price valuation. Concretely, this means imposing a 30% tariff on businesses looking to expand their sales through the Apple App Store (see the recent Apple vs Hey controversy). And in time, such practice invites a regulatory backlash.

To put this another way, when Swiss Journalist Jacques Mallet du Pan was covering the French Revolution, he observed that “like Saturn, the revolution devours its children”. Today, no one can deny that the tech revolution has upended our work productivity, societies and social mores. Yet the fathers of this revolution seem to be increasingly turning on each other, whether it be:

The list goes on but the common thread is the quandary of where growth will come from to justify today’s punchy valuations. And whether governments will encourage, or look askance, at this future potential growth. In that regard, the fact that being anti “Big Tech” may, at this juncture, be the only bipartisan issue in Washington DC (aside from bashing China) will perhaps start to give investors pause. And if so, then this could end up having big macro implications, including for the US dollar.

Foundation #4: The US dollar will stay well bid

A strong dollar is a linchpin to the view that US tech stocks are the only growth story that matters. To an extent these two beliefs feed into each other. When the dollar strengthens, capital from all corners flows into large-cap US tech stocks, which in turn means more US dollar buying. One important effect of a stronger dollar is to make it harder for emerging economies to grow. In EMs, large-scale, productivity-enhancing capital spending programs are typically financed in dollars. Thus, a stronger US dollar equates to a higher cost of capital for emerging markets and so a weaker growth rate; in contrast, a weaker US dollar usually unleashes a wave of growth in EMs.

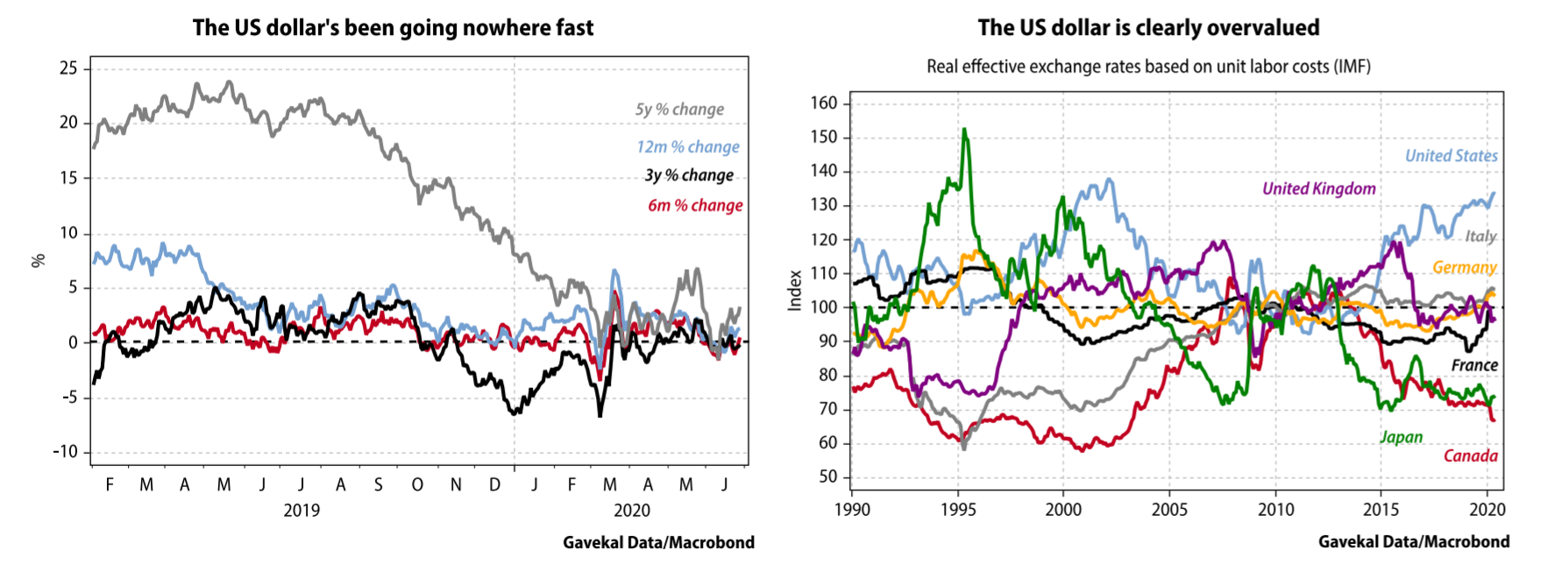

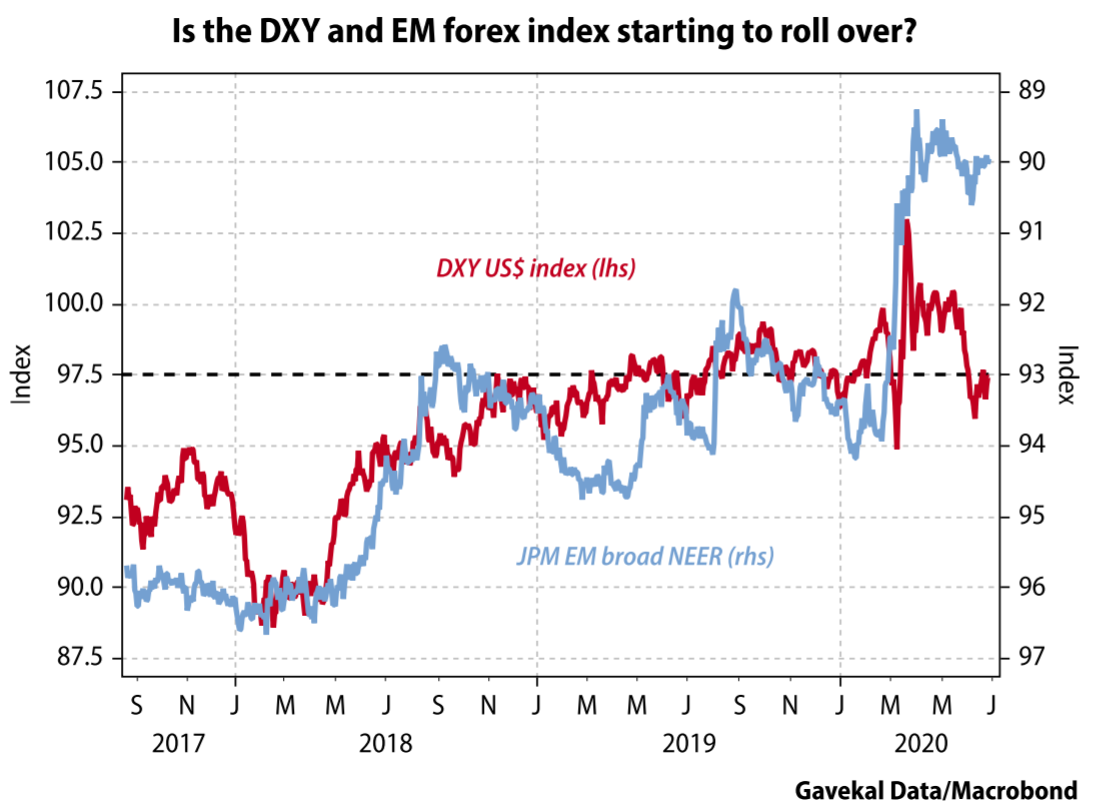

Yet, interestingly, the performance of the US dollar in recent times has been pedestrian. This, despite the outperformance of both US equities and the US economy and the prevalence of positive interest rates. The chart below shows that investors who held US dollar cash on a six-month, 12-month, three-year or five-year time frame have not seen material relative gains.

The US dollar’s outlook seems unlikely to change for the following reasons:

One doesn’t have to be excessively cynical to think Treasury Secretary Steven Mnuchin will open the fiscal floodgates before the election. The effect would be to unleash another surge of US liquidity, which will likely make its way abroad through a sharp widening of the US current account deficit. Such a possibility undermines talk of a further US dollar short squeeze.

A flood of dollars exiting the Treasury’s checking account could be amplified by money also leaving US consumers’ checking accounts. A key feature of the Covid-19 crisis has been much of the West’s working population staying at home. This has reduced spending on everything from restaurants to gasoline. The flip side has been burgeoning checking and savings accounts. Never before have Western countries in unison seen such a surge in savings rates as in the first half of this year. A key question is whether this money stays in US consumers’ bank accounts, or ends up being spent in an orgy of “revenge shopping” that is transferred to foreigners via the current account deficit.

If the latter scenario unfolds, the US currency is only likely to hold up by foreigners reinvesting their acquired dollars into US assets. This may occur if US equities can again outperform, or if investors come to believe that US tech really is the only growth game in town. In contrast, if US and European policymakers start to move against the tech firms then foreigners may think twice about recycling their earned US dollars back into the country.

In short, the supply of US dollars should not be a concern in the coming weeks and months. Putting it together, the picture is of rising supply and flat to falling demand. Such an unpromising outlook for the US dollar suggests that the next important move may be for a weakening to unfold. The only question left is whether this weakness has already started.

Foundation #5: Inflation is not a risk—not in the near term

Back in 2010 as the Fed embraced quantitative easing, many investors feared that inflation, or even hyper-inflation, would be unleashed. Comparisons were drawn to Venezuela, Zimbabwe and even Weimar Germany. Meanwhile, waiting for inflation became like waiting for Godot.

Just as success has many fathers, there were many reasons why inflation did not take off (my 2012 book Too Different for Comfort made this point). There was the collapse in energy prices linked to the shale revolution, the fall in monetary velocity as banks nursed their wounds and the post-2008 acceleration of globalization. The crisis pushed leaders to look for new solutions. They bypassed multilateral bodies like the World Bank, International Monetary Fund and World Trade Organization and instead created new institutions like the G20, Asian Infrastructure Investment Bank and the Silk Road Fund.

The 2008 crisis unleashed an epic infrastructure boom across China that added an additional 500mn Chinese workers to the global workforce. Before 2008, foreign firms had to pretty much locate factories in the Pearl River Delta, Shanghai or Wenzhou. Fast forward a few years and Chinese manufacturing could as easily be done in Zhengzhou, Chongqing, or Wuhan.

Unfortunately, the main revelation of 2020 is that the low price offered by facilities in Wuhan and similar cities was “false” as it did not factor in negative externalities from wildlife markets with dubious hygiene. The corollary of prices of the last decade being shown to be artificially low is that future prices will have to adjust higher. The implication is that the deflationary forces of the last decade cannot be relied upon to remain dominant.

Conclusion

The fact the macro landscape is changing fast should not surprise us given fiscal and monetary stimulus, rising geopolitical tensions, lower energy prices and an uncertain global growth outlook. Thus, it seems unsatisfactory to explain the Nasdaq being just above its pre-Covid-19 level by the world looking at “more of the same”. This leaves two other explanations for the post-March 23 rally, namely, (i) investors have taken leave of their senses, or (ii) investors are acting on the premise that cash may become worthless in the coming years. I will review both possibilities in upcoming papers.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.