"US tech stocks have been hit hard, as attention focuses on the underlying quality of themes like the migration to electric vehicles. Yet this shakeup is also happening against the backdrop of a fast-changing investment environment due to a strengthening US growth outlook, rising inflationary pressure and an unnerved bond market which is driving yields higher. In this video interview, Will Denyer of Gavekal Research seeks to unpack these dynamics in order to navigate a course through difficult trading conditions."

Watch the video interview or read the transcript below.

Gavekal's Nick Andrews interviews Will Denyer in a brief 9-minute conversation on his perspectives regarding the outlook for U.S. equities this year and beyond. Denyer is a regular guest of the Evergreen Virtual Advisor, with recent pieces such as, Bitcoin, gold, or Fiat? and The Senate Upheaval.

Andrews: …Clearly, we’re seeing the unwind of some of the excesses in the U.S. tech sector—and in particular, we’ve seen the electric vehicle (EV) space get ‘thumped’ … how are you seeing this unwind in the U.S. equity market?

Denyer: I think this is all part of the two big rotations we’re seeing for the post-Covid world. The first being a move from the Covid winners of last year—those that not only handled the crisis well but thrived during it; online retailers and the like—back into the Covid losers. The other is the rotation from growth to value, driven by interest rates. Growth stocks are inherently a long-duration asset because you’re discounting a large chunk of your earnings far out into the future. As opposed to value stocks which derive much of their value from near-term earnings. When interest rates rise, your growth stocks really get hammered, while your value stocks are relatively unhurt. EVs and tech stocks are both examples of either growth stocks or covid winners. The EV space is very exciting, but a lot of the earnings that you’re discounting are way off in the future. So as interest rates have risen, those guys are getting hurt.

Andrews: Let’s think about the rising interest rates. We have the Federal Reserve offering a very benign view of the outlook and a tolerance for potential inflation, while the market is taking a very different view. Can you tell me where you stand on this?

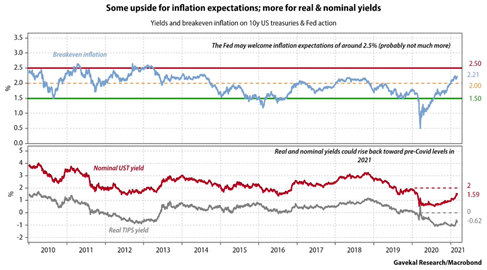

Denyer: The short answer is that I side with the markets. I don’t want to get too carried away—the Fed is not going to start hiking rates or do aggressive quantitative tightening tomorrow; these things are still a ways off and there is still some slack in the system. But that slack is abating very fast. My view at the start of the year was that we are already seeing a pretty fast economic recovery and now we have vaccines coming out. So, we are going to have more people everyday feeling a new level of confidence to go out and spend. Some businesses that have been closed due to economic restrictions are going to reopen. At the same time as that happens and we have strong fiscal stimulus, the table seems set for a nominal growth boom. Given how fast things have recovered already, the concern was ‘why are people buying bonds at negative one percent real yields’. It just didn’t make sense. My bet has been that we would see a normalization this year on bond-buying back toward pre-Covid levels and that I think is what we are in the middle of now.

Andrews: Let’s unpack that inflationary dynamic a bit. On Friday, we saw the monthly payrolls report that showed a pretty strong number, however, we still have millions of Americans unemployed, and…it’s not clear that we will see these people re-employed very quickly. Is not the fundamental driver of U.S. inflation the labor market? And will that not take a long time to repair?

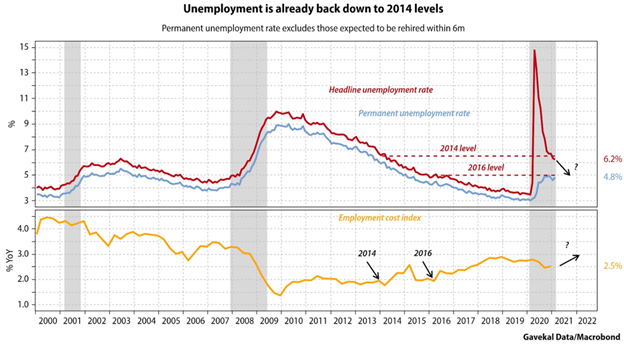

Denyer: There’s a lot of talk now about being inclusive and looking at a broad array of employment indicators, and I agree; the more data the better. But, the unemployment rate is still the most useful indicator of labor market slack because you’re looking at how many people that want a job have one. The unemployment rate is still higher than estimates of natural unemployment, but it is coming down very fast. We had the highest unemployment rate in post-war history less than a year ago. We now have recovered back to levels we saw in 2014. So in the span of a year, we’ve seen a labor market recovery that took five years after the last crisis. That is to say, things are developing much quicker than last time. And—as I said with vaccines, fiscal and monetary stimulus—we could get back to 2016 levels (< 5%) of unemployment by the end of this year. The reason why being that a lot of this unemployment was temporary.

Talking about inflation pressures: when it comes to wages there is a loose link between the unemployment rate and wages, and between wages and CPI (or other broader inflation measures). As I said, it’s a loose link but it’s one of many drivers and something to consider.

In 2014, we saw the first signs of wage pressure start to accelerate. That at first looked quite aggressive and then backed off. Then it started again in earnest in 2016, and that time never backed off. So between 2014 and 2016, you started to see wage pressures building. As I just said our unemployment rate is already at 2014 levels and could be at 2016 by the end of the year.

Andrews: So, we have a normalization of yields and a normalization in the U.S. labor market, as well as an ongoing…implosion of one of the big thematic drivers in the market. This doesn’t sound like a great brew. From your perspective, how do things wash out in terms of the overall U.S. equity market?

Denyer: In terms of the overall U.S. equity market, I’m still modestly overweight equities versus cash, and more aggressively overweight equities versus bonds. So I am still relatively constructive on equities. The reason why is that we have already seen a decent pick up on nominal yields (real yields have picked up some, though not as much and there is more scope for them to rise going forward). As real yields rise, that (all else equal) is negative for equities in general. But against that, you also have a boost to earnings. This is why bond yields are rising, as people look at higher nominal growth and then look forward to the day that the Fed tightens, even just tapering QE. Equities do get that counterforce; the boost to nominal earnings. You don’t get that in gold or bitcoin, which just get potentially hurt by the rise in real yields without an earnings boost. So overall, I think a modest overweight equities versus cash makes sense. But if bond yields keep rising at a high pace, it will be hard for equities to push higher. I’d say the safety bet today is to remain modest overweight equities versus cash but have it focused on the covid losers and the value stocks, which are less vulnerable to rising yields.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.