Click here to view as PDF.

“Mimicking the herd invites regression to the mean, merely average performance.”

–Warren Buffett’s long-time partner CHARLIE MUNGER

“The inherent irony of the efficient market theory is that the more people believe in it and correspondingly shun active management, the more inefficient the market is likely to become.”

–Money-management superstar SETH KLARMAN

“Passive investing has reached mania status.”

–JEFF GUNDLACH, popularly known as the new King of Bonds

Editor’s Note: This week’s EVA is adapted from a letter sent to Evergreen clients on Wednesday, January 2nd. For non-clients who want more information on how Evergreen can help you navigate these increasingly choppy market conditions, please reach out to info@evergreengavekal.com.

While we hope you enjoyed the recent holiday season, that was some kind of Santa Claus rally last month! The only problem was that it was of the inverse variety. In fact, it was the worst December for stocks since 1931. Remarkably, this was magnified by a brutal abbreviated trading session on Christmas Eve, when the S&P 500 fell nearly -2 ½%. Most days before Christmas have been positive and, previously, the worst loss on this normally cheer- infused day was -1%.

Based on what a wild year-end it was, we thought we’d again interrupt our regular Evergreen Virtual Advisor schedule for a quick update. As you are aware, especially if you read our weekly EVAs, we’ve been preparing for this type of challenging market for quite some time. Consequently, the current weakness is not a shock to us. The only surprise is that it took this long to happen and that it occurred at a time of the year when stocks are typically buoyant.

Right before Christmas, the level of selling truly attained panic levels with many stocks and sectors. Accordingly, on a broader basis, the damage is actually much worse than the official S&P and Dow Jones indices indicate. The median US stock was down about -14% for 2018, as were the typical overseas markets. (However, large portions of the US market remain extremely expensive; thus, as we’ve recently communicated, it has become a “two-tier” market, split between compelling bargains and the still numerous priced-beyond-perfection issues).

Even balanced stock/bond portfolios had a rough 2018. As J.P. Morgan’s Chairman of Market and Investment Strategy, Michael Cembalest, noted this week, “diversified stock and bond mixes generated negative returns from -7% to -4%.” Much of this was due to the year-end melt-down that impacted almost all corporate securities, including the usually defensive areas of bonds and preferred stocks.

Our key message is that this type of blind and irrational selling is precisely what we’ve been expecting and have been prepared for with our substantial cash and cash-equivalent holdings. The cash we have in our clients’ portfolios is the main reason almost all Evergreen portfolios declined materially less than the S&P 500 from the peak in late September. It also gives us the luxury to buy when so many others are frantically selling.

Below, we have included a few brief comments to elaborate on these points and provide a fuller overview.

- The last decade has been an ideal time for “no-think” and fully-invested passive strategies that have simply rode the massive waves of central bank money fabrication. In the coming years, we believe agile and opportunistic money management is likely to provide far higher returns than straight index-type strategies. Nearly all trading is done today by computers and passive entities that don’t engage in traditional fundamental analysis. We believe this reality has been behind both the excessive rise in recent years experienced by US stocks, as well as the sudden fall since late September. The Wall Street Journal picked up on this in an article on December 26th with this headline:

“Behind the Market Swoon:

The Herd-like Behavior of Computerized Trading

Behind the broad, swift market slide of 2018 is an underlying new reality: Roughly 85% of all trading is on autopilot—controlled by machines, models, or passive investing formulas, creating an unprecedented trading herd that moves in unison and is blazingly fast.”

- Evergreen believes this herd-like behavior has created a lengthy list of exceedingly attractive investment opportunities. Because of our high cash position, we believe investors who followed our advice, and also now hold a large amount of cash, should view this mass and indiscriminate selling as an opportunity on which to capitalize. In our view, current market prices for many US stocks are far, far below fair value. It’s been a long time since we’ve been able to write those words. Consequently, we’d suggest not placing too much emphasis on where out-of-favor issues are trading these days—which is quickly becoming a large share of the market. In our view, there is little connection between current quotes and the true value of the many companies whose stocks have been body-slammed. Energy is perhaps the most glaring example, but this deep undervaluation is spreading out to include most market sectors.

- Next, even though we have felt a major correction was overdue, we have been wrong—at least, so far—that the conservative and high-income mid-stream (pipeline) sub-sector would hold up better. That area’s recent weakness is surprising given they have been reporting some of the best operating results we’ve ever seen. We expect energy in general, and, in particular, Master Limited Partnerships (i.e, mid-stream oil and gas companies owning pipelines, storage terminals, gas processing plants, etc) to lead a market rally that we see starting soon. We also believe investors have become much too negative on oil prices and the nearly 10% surge on Wednesday of last week was encouraging to see. We anticipate crude recovering much further, though it is likely to be a rocky ride at times. We further foresee an upside burst by the mid-stream companies, similar to what occurred from last spring to mid-summer when they produced roughly a 28% total return. We are gratified that in just the first three trading days of 2019, the mid-stream energy sector is up 7% (as of 10 a.m., January 4th, PST).

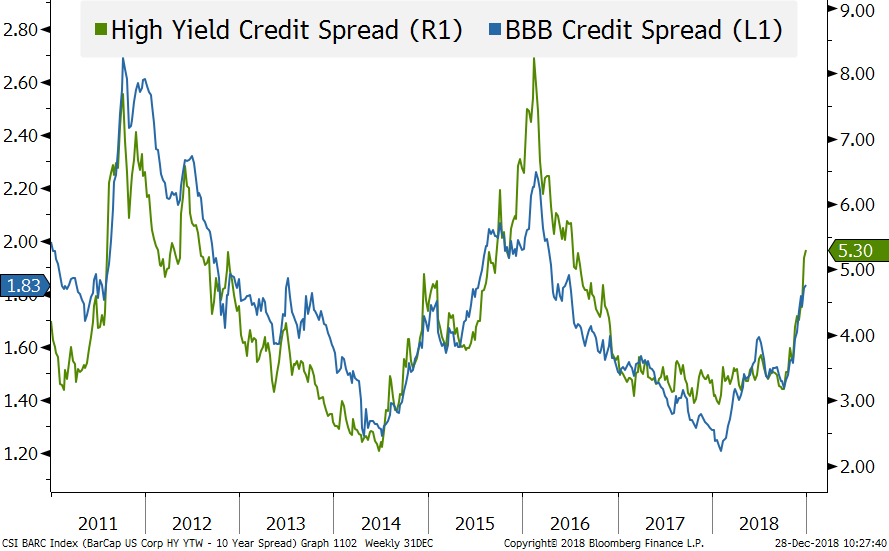

- Many investors ignore the bond market. We think that’s a major mistake. Credit spread* blow-out episodes, such as we are beginning to see, are extraordinary times to lock-in yields that are well above the prevailing level of what remain artificially suppressed interest rates. (Incredibly, there are still $7 ½ trillion of bonds around the world with negative yields!). If spreads continue to expand—almost a certainty should the US tip into recession—the panic in this area could hit a fever-pitch. Again, for cash-heavy clients who are prepared to buy into the selling frenzy, this could be the gift that keeps on “gifting” by locking in high single-digit or even low double-digit yields that will sustain cash flow for years to come.

Source: Bloomberg, Evergreen Gavekal as of 12/28/2018

- We are reluctantly coming to the conclusion that the US will experience at least a mild recession in the second half of 2019, which could be a so-called balance sheet recession. These are caused by the combination of falling asset prices and excessive debt (especially, today, in the corporate sector). Additionally, we suspect earnings estimates for the S&P 500 are still too high and that an actual decline in profits this year is increasingly probable.

- Trade tensions with China have obviously played a big role in the market turbulence of the past few months. Thanks to our partnership with Gavekal, which is headquartered in Hong Kong, we have access to critical insights as to how China is reacting to and coping with the trade war. Interestingly, since mid-October, Chinese stocks have actually risen slightly while the S&P 500 has fallen nearly 9%. A number of Chinese shares appear to be extraordinarily undervalued. However, the air is clearly coming out of China’s once-bubbly real estate market and that has the potential to be highly problematic for its economy and even social order. You may have read that dissatisfied Chinese property

speculators investors have been staging violent protests over the sudden swoon in prices. In our view, holding some severely depressed Chinese stocks makes sense but we would advise against going “all-in”.

As prior EVAs have noted, bear market rallies can be exceedingly vigorous. Considering the degree to which so many stocks, both in the US and around the world, have been pummeled, any snap-back could be surprisingly strong. Regardless, we want to be clear that we are no longer broadly bearish on stocks, even in the US. We believe that there are a number of issues that should be able to provide high returns over the next three to five years. However, investors should be prepared for what could well be another down year for the S&P and the Dow.

On the hopeful side, we’ve previously expressed our view that we could be on the verge of seeing a replay of 2000 and 2001 when the S&P fell steeply but many stocks that had been crushed by the rush into tech stocks during the late 1990s mania rose substantially.

As a result, our preferred strategy at this point is to remain cash-heavy but to methodically accumulate the shares of high-quality companies that have, in many cases, been cut in half—or more—if (and it’s a big “if”) their prices are low enough to constitute true bargains. Unfortunately, there are a plethora of US stocks that don’t come close to qualifying as undervalued, despite the fact they are down considerably from their recent highs.

It’s one of those trite but, in this case, true clichés that it’s now become a market of stocks versus just a stock market. Stock pickers, rejoice—indexers, not so much. Actually, indexers haven’t had much to shout about—unless in frustration—for a very long time, outside of some recent frothy years that are quickly being de-frothed. The annual return on the S&P 500 from 12/31/99 through 1/3/19 is 4.8%, including dividends. Unfortunately, for those whose fortunes—literally—are tied to the S&P, that modest number is likely to shrink even further in the year ahead.

*Credit spreads are the difference between the yield on government and corporate bonds. Significantly narrower spreads are generally a positive while materially wider spreads are almost always a negative.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE *

- Large-cap growth (select issues are looking much more attractive after the recent meltdown)

- Some international developed markets (especially Japan)

- Cash

- Publicly-traded pipeline partnerships (MLPs and other mid-stream energy securities) yielding 7%-15% (as a result of the powerful rally of the first three trading days of the year, buy more selectively)

- Gold-mining stocks

- Gold

- Select blue chip oil stocks (also buy aggressively due to the utter capitulation in the energy sector)

- One- to two-year Treasury notes

- Canadian dollar-denominated short-term bonds

- Short-term investment grade corporate bonds (1-2 year maturities)

- Emerging market bonds in local currency (start a dollar-cost-averaging process and be prepared to buy more on further weakness)

- Mexican stocks (due to the recent severe selloff, we are adding back exposure to a Mexican REIT that we sold materially higher)

- Large-cap value (there are a plethora of bargains now in this area)

- Intermediate municipal bonds with strong credit ratings

- Intermediate-term Treasury bonds (especially the five-year maturity)

* Due to the severity of the recent market selloff, we have reduced our equity underweight from 50% to approximately 43%.

NEUTRAL

- Most cyclical resource-based stocks (some are looking more attractive)

- Mid-cap growth

- Emerging stock markets; however, a number of Asian developing markets appear undervalued

- Solar Yield Cos

- Canadian REITs

- Intermediate-term investment-grade corporate bonds, yielding approximately 4%

- US-based Real Estate Investment Trusts (REITs)

- Long-term investment grade corporate bonds

- Long-term municipal bonds

- Short euro ETF

- Long-term Treasury bonds

- Investment-grade floating rate corporate bonds

- Select European banks

- Small-cap growth

- Preferred stocks

DISLIKE

- Small-cap value (start covering shorts)

- Mid-cap value

- Lower-rated junk bonds

- Floating-rate bank debt (junk)

- US industrial machinery stocks (such as one that runs like a certain forest animal, and another famous for its yellow-colored equipment)

- BB-rated corporate bonds (i.e., high-quality, high yield; in addition to rising rates, credit spreads look to be widening) * **

- Short yen ETF (i.e., we believe the yen is poised to rally)

- Dim sum bond ETF; individual issues, such as blue-chip multi-nationals, are attractive if your broker/custodian is able to buy them

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

** Due to recent weakness, certain BB issues look attractive.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.