“History repeats itself, but in such cunning disguise that we never detect the resemblance until the damage is done.”

–SYDNEY J. HARRIS, journalist and author

If someone were to dive deep into the Evergreen Virtual Advisor (EVA) archives, they would stumble upon a publication from two years ago titled, “America is Great, Home Country Bias Ain’t.” The bulk of the article was written by GMO’s Rick Friedman and its main premise is that investors skew their equity exposure towards their home country. Americans who have invested in line with this idea over the past decade have unquestionably been beneficiaries as benchmark indexes including the S&P 500, Nasdaq and Dow Jones have all been on epic bull runs.

However, as last week’s “Instant Classic” newsletter outlines, legendary investor Ray Dalio believes there is a paradigm shift on the horizon and suggests investors rotate into assets that post good returns when money is devalued – such as gold. This week, Evergreen’s partner Louis-Vincent Gave makes a parallel argument, outlining his belief that investments following the prevailing groupthink of today will underperform other areas - such as emerging markets and commodities - over the next decade.

Louis’ investment thesis for the 2020s is bold and likely at odds with anyone who has been lulled into the idea that cycles are antiquated. Those still inclined to believe that history does in fact repeat itself will find ample evidence in the article below that actual results often differ from popular beliefs when it comes to the long-term game of investing.

AN INVESTMENT THESIS FOR THE 2020s

By Louis-Vincent Gave

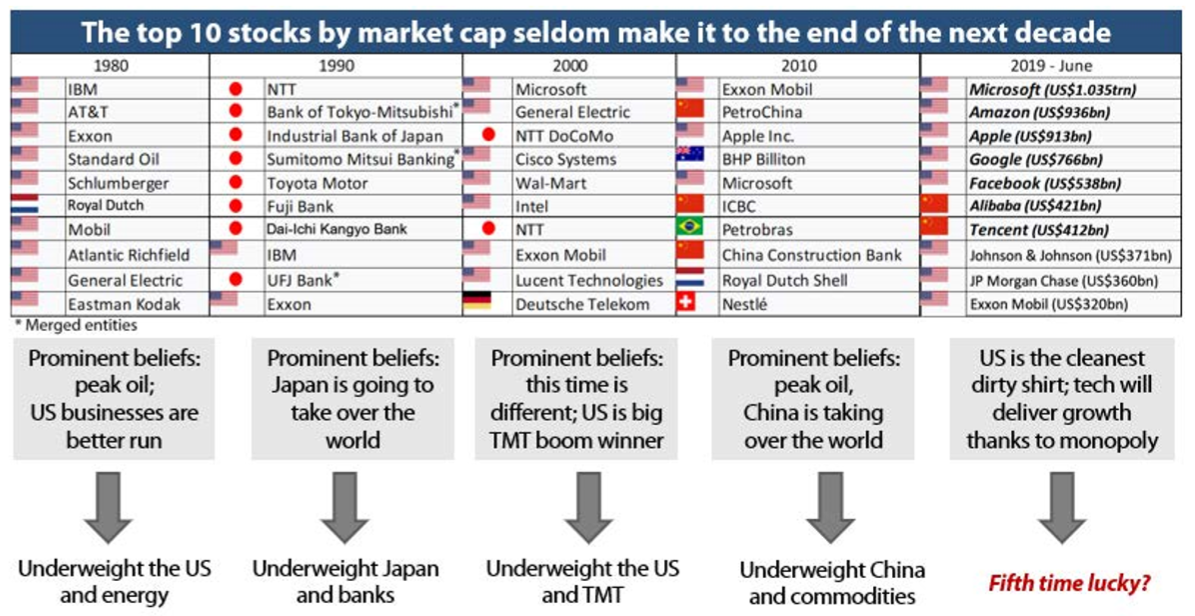

Is long term success in investing more easily achieved by picking winners, or by avoiding losers? Arguably, the second path takes a lot less work. The table below illustrates the point nicely; it lists the world’s 10 biggest companies by market capitalization at the beginning of each decade since 1980.

In 1980, the broad consensus was that “democracy inherently promotes inflation.” According to the prevailing belief of the day, politicians would always try to buy votes with unsustainable public spending, while central bankers would be unable to withstand pressure from governments twisting their arms to fund the ever-growing budget deficits. As a result, the only stocks worth holding were of companies with real assets, and especially commodity producers. At the time, energy names made up almost a third of the MSCI World index, and six of the world’s top 10 companies.

So much for the consensus. In 1980 any investor brave enough to own zero energy in his or her portfolio could have packed up and gone to the beach for the next 10 years, and at the end of the following decade would have outperformed handsomely.

Remember when Japan was the future?

After his decade-long beach holiday, our outperforming investor would have returned to the office in 1990 only to be told that if he did not learn Japanese, then there would be no job for him in the coming years. Japan’s superior management techniques and bank-led financing model would ensure that Japanese corporates would take over the world. Given this consensus, it was no surprise that in 1990, eight of the top 10 companies in the world were Japanese, and six of those eight were banks. How could you lose money owning Japanese banks when Japan was set to take over the world?

Still, if our investor had decided to underweight Japan (which by January 1990, made up 45% of the MSCI World index), then once again he could have afforded to head for the beach for the entire following decade.

Coming back in 2000, our investor would have found a market segmented between attractively-valued “old economy” stocks, and “new economy” stocks valued on previously unheard of measures such as “price to eyeballs”. These new economy stocks, in media, telecoms and technology, made up more than a third of the MSCI World. Yet again, if our courageous investor chose to ignore the hype, he could have gone on holiday for another 10 years.

Returning in 2010, he would have found that the prevalent belief was that it was actually China that was going to take over the world. And China’s insatiable thirst for commodities meant that the world not only faced “peak oil”, but peak copper, peak nickel, and perhaps even peak coal. By that point, five of the world’s top 10 companies by market capitalization were involved in digging stuff out of the ground while, for the first time, three of the world’s top 10—PetroChina, ICBC and CCB—were not only state-owned companies, but state-owned companies of a nominally communist government which a generation earlier had been gunning down its own students on the streets of its capital. Freshly returned from the beach, our investor might have found this odd, and might reasonably have decided to deploy his capital elsewhere.

Back from the beach once again

All of which brings us to today and the approaching end of the current decade. Once again, our fantasy investor will be coming back from the beach to review the beliefs underpinning today’s bull market. And he will find that:

As these beliefs have taken hold of investors’ psyches, asset prices, interest rates and exchange rates have adjusted in consequence—to the point where eight of the top 10 companies in the world are now American (I exclude Berkshire Hathaway, as it is more an investment conglomerate than a typical company) and seven out of the 10 are technology stocks. Beyond the top 10, the US is now 56% of the MSCI World, the market cap of the entire European banking sector is less than the market cap of JP Morgan, and the daily trading volume of Amazon often surpasses the daily volume on the Hong Kong stock market.

All this might make sense, and perhaps in 10 years, our beach-loving investor will come back to a world in which all the top 10 stocks are US tech companies, and where the US accounts for 65% of the MSCI World. But I doubt it, for the following reasons:

This brings me back to the table on the first page, and the acknowledgment that for a bull market to evolve into a bubble—and let’s face it, bubbles are where the fun is—there needs to be an over-riding idea to unite investors into a single, common faith. Famously, investors are motivated by two emotions: greed and fear. And in a bubble, greed can have two drivers, but fear only one—giving rise to three different types of bubble.

How big can a Schumpeterian bubble blow?

Investors today are betting on the continuation of the Schumpeterian bubble. As tech companies move into finance, as the fortunes poured into health research reap a new harvest of breakthroughs, as our dependence on fossil fuels for transport and energy disappears, as robots eliminate mindless work, the consensus is that we will genuinely move into a brave new world of ever better modern conveniences. But while this sounds attractive and exciting, we should remember that multi-year investment trends are like very big dogs: they seldom live past their first decade. Instead, the historical precedents would suggest that the top 10 companies of 2030 are more likely to reflect either the growth of capitalism into new territories (India? Latin America? China? South East Asia?) or the fear that there won’t be enough for everybody.

On this point, the Mayans used to believe that history was made up of recurring cycles of 52 years; a notion which fits nicely with the popular belief that people avoid making their parents’ mistakes, only to repeat their grandparents’ errors. So perhaps in 2030 the market will be primed for a return of the belief that democracy can only lead to inflation, as politicians chase votes with barely-dry cash?

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.