"The stock market has turned out to be this casino in which people buy shares because they think they can sell them to somebody at a higher price. That’s speculation."

-JACK BOGLE, Founder and CEO of the Vanguard Group (pictured above)

"At some point in the next nine months a historic milestone will be passed. More than half of managed equity assets in the US will be run on a passive basis…At the current rate, we forecast that this will happen sometime in January 2018."

-INIGO FRASER JENKINS, Sanford Bernstein

Much has been written in this publication’s pages about “ETF*-mania” and the rise of passive investing. In fact, devoted readers need not look farther than last week’s Pull It Together (Part II) EVA to read a quick synopsis of Evergreen’s belief that the passive fad is sure to end poorly.

The question perplexing many market “experts” is when the fad will fade. The trend has certainly not been kind to active managers since the global financial crisis, as many have seen their assets under management (AUM) decline while investors have left in droves for passive pastures. Even famed investor David Einhorn of Greenlight Capital experienced the pain recently, as his hedge fund lost more than $400 million to redemptions last quarter.

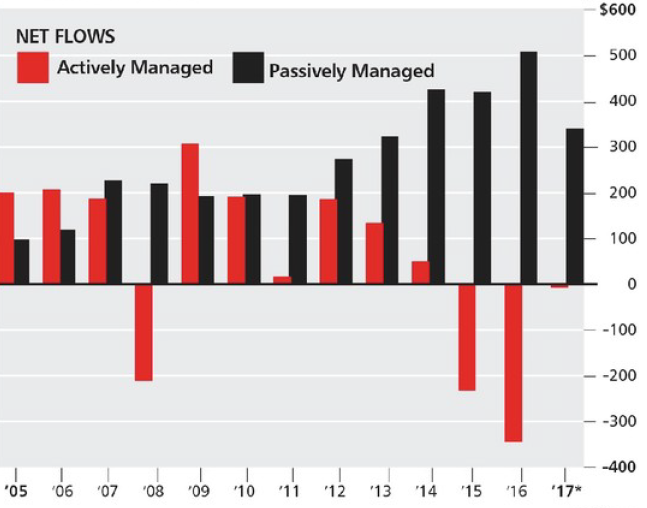

So, just how drastic is the drift? As the chart below shows, net flows into passive funds have severely bested their active counterparts since 2011 – just a couple short years into the market’s most recent run.

ACTIVE VS. PASSIVE NET FLOWS (BILLIONS)

Source: Morningstar, Barron’s (through 5/31)

Source: Morningstar, Barron’s (through 5/31)

With over $800 billion in net inflows forecasted to move into passively managed strategies in 2017, it’s fair to say that what was an evenly-matched contest in terms of comparative flows has turned into a rout.

While we believe the current craze for passive strategies is overly-hyped in its ability to outperform active in the long-term, we concede that the original idea for index funds and ETFs was truly brilliant. In fact, Evergreen was an early adopter of ETFs.**

But, as discussed in prior EVAs, when a benchmark becomes an investment, problems can occur. The distortions Grant Williams (this week’s EVA author) describes due to the flood of trillions into index vehicles is a great example. Stocks get pushed up to extreme levels without regard to valuation.

Further, as indexing takes over the investment world, it also has negative consequences for the economy as capital is allocated less efficiently. Perhaps this is one reason why this expansion has been so lackluster.

As noted above, this week’s Guest EVA comes from Grant Williams, a long-time friend of Evergreen Gavekal and author of the popular publication Things That Make You Go Hmm… He is also the co-founder of Real Vision TV, a rapidly growing online financial channel. (By the way, RVTV’s popularity has survived our Chief Investment Officer being featured on several occasions.)

In the following pages, Grant provides context for the shift towards passive investing and the rise of ETFs, before outlining the inherent risks of both trends.

One thing is certain: the Ice Age for passive investing is upon us; but, those able to survive the temporary freeze will likely experience an active investing golden age when the ice finally cracks.

*Exchange Traded Funds, which are often index-type securities

**Although, unlike many investors, we have always utilized them in a contrarian way. A good example was our overweighting of Large Cap Growth – LCG – ETFs back in 2004 when we first started our Right Cycle Investing portfolios. In the wake of the tech bubble blow-up, LCG was very out-of-favor and it has materially out-performed the S&P 500 and, especially, its Large Cap Value peer since that time.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

Regression: noun, re·gres·sion ri-‘gre-shen

1. The act or an instance of regressing

2. A trend or shift toward a lower or less perfect state

3. Retrograde motion

-Merriam-Webster

PASSIVE REGRESSION

By Grant Williams

(Note: Grant’s article was too long to present in full-form. As such, we have compiled excerpts from Passive Regression below. Breaks in writing are noted with ellipses throughout this article.)

Today will be the precursor to a more in-depth look at two phenomena I have been talking about for some time but which seem to increase in importance with each passing week; the shift to passive investing and the rise of ETFs and the danger inherent in both. A little background, if you will.

So, as this is a precursor, let’s go back to the beginning, shall we? That seems to make sense to me.

On August 31, 1976, after an Initial Public Offering, First Index Investment Trust was launched by John C. Bogle’s Vanguard Group (an entity which, at that time, had itself only been in existence for 16 months).

Even back in the 1970s, the media liked to hang catchy names on anything they could and First Index Investment Trust was no exception. A skeptical press dubbed the vehicle ‘Bogle’s Folly’ and, it has to be said, with fairly good reason.

The initial target for the Trust was $150 million and, with the four largest Wall Street retail brokerages constituting the underwriting group, Bogle’s hopes were high that his new idea would be a roaring success.

Sometimes, however, things don’t turn out as anticipated.

At the close of the underwriting period, the First Index Investment Trust had raised the princely sum of...wait for it... $11.3 million—a 93% shortfall from the stated goal and, in true Wall Street fashion, the underwriters approached Bogle and suggested the deal be canceled as the IPO had been an ‘abject failure’ (those are Bogle’s words, not mine).

In fact, here’s Mr. Bogle himself reminiscing first about the reasoning behind the First Index Investment Trust and then the troubled launch of what was the world’s first passive investment vehicle:

Back in 1976, my associates at Vanguard shared my confidence that indexing would ultimately come to reshape the mutual fund industry. After all, an index fund, with its minuscule costs, would guarantee that our investors would earn their fair share of stock market returns.

But managed equity funds as a group, because of their high costs—advisory fees, operating expenses, sales loads, portfolio transaction costs, excess taxes—virtually guaranteed the reverse, a substantial shortfall...

...Nobel laureate economist Paul Samuelson played a major role in precipitating the index fund’s creation. While I’d hinted at the idea of an index fund in my senior thesis at Princeton University in 1951 (mutual funds “may make no claim to superiority over the market averages”), Samuelson was much more forceful, strengthening my backbone for the hard task that lay ahead: taking on the industry establishment.

His article “Challenge to Judgment” caught me at the perfect moment. Published in the inaugural edition of the Journal of Portfolio Management in the autumn of 1974, it pleaded “that some large foundation set up an in-house portfolio that tracks the S&P 500 Index—if only for the purpose of setting up a naïve model against which their in-house gunslingers can measure their prowess.”

Presented with that challenge, I couldn’t resist. While all of our peers had the opportunity to create the first index fund, Vanguard alone had the motivation. The newly formed Vanguard Group (owned not by outsiders but by its own shareholders), I reasoned, ought to be “in the vanguard” of this new concept. Our goal was to offer well-diversified funds at minimal costs, focused on the long term. (Wall Street Journal)

OK, so when I said I’d go back to the beginning, I didn’t actually mean 1951 when passive indexation was nothing more than a firing synapse or two in the brain of a young Princeton undergrad, but still, it’s fascinating to see just how long this idea was percolating in Mr. Bogle’s mind.

Fast forward to August 1976, however, and, as we’ve already seen, the first foray into indexation was less than satisfactory:

“We were confident that the IPO would be a roaring success. Not only was the math that assured the index fund’s superiority unarguable, but the principal underwriters included the four biggest retail brokers on Wall Street. Their target was $150 million. But when the books were closed, the underwriting of First Index Investment Trust produced just $11.3 million, a 93% shortfall from the goal. When the underwriters brought me the news of the abject failure, they suggested we cancel the deal, for the tiny proceeds were insufficient to own all 500 stocks in the S&P 500 Index. I remember saying: “Oh no we won’t! Don’t you realize that we now have the world’s first index fund?” (Wall Street Journal)

See? I told you ‘abject’ and ‘failure’ were Mr. Bogle’s words and not mine.

Of course, it’s no surprise to see Wall Street’s biggest retail brokerages trying to cancel a $150 million deal they’d underwritten when it went so poorly, but Jack Bogle’s doggedness is to be admired.

Had Mr. Bogle buckled to pressure from Wall Street brokerages desperate not to write a large and unexpected check as opposed to cashing a large, expected one, the investing landscape may be a very different place today, but stand strong he did and the results of his determination have been transformative.

By 1999, that initial $11millon invested in Vanguard’s passive strategy had reached $100 billion.

Since the launch of Bogle’s Folly, indexation has positively blossomed. Thirty-five years after Jack Bogle faced down those shell-shocked retail brokerages, Bogle’s Folly was just one of roughly 300 distinct stock and bond mutual funds in the United States, which between them were home to hundreds of billions of dollars but, alongside those indexation products of which the First Index Investment Trust was very definitely in the vanguard (sorry, but that was just too easy) there were another 1000-odd U.S.-based passive exchange-traded funds.

Between the stock and bond index mutual funds and ETFs, there was roughly $2.3 trillion in passive assets invested in the U.S. markets back in 2011—roughly a third of the then-$7.3 trillion squirreled away in actively-managed funds.

Since then... well let’s just say things have changed.

Now, let’s just park all that for the time being because I just introduced ETFs into this conversation and that is another history lesson we really need to explore before we can move on and get into the nitty gritty of passive investing as it pertains to today’s market.

The first attempt at creating an ETF-type product is widely accepted to have been the launch of Index Participation Shares on the S&P 500 all the way back in 1989. Hard to believe, I know, but that’s how far back we are going here.

...

But it wasn’t until January of 1993 that the American Stock Exchange launched the S&P500 Depository Receipt and the party got started in earnest.

S&P Depository Receipts...SPDRs.

That’s right—your friendly, neighborhood Spiders, man.

And, as the SPDRs grew, so did the ETF complex.

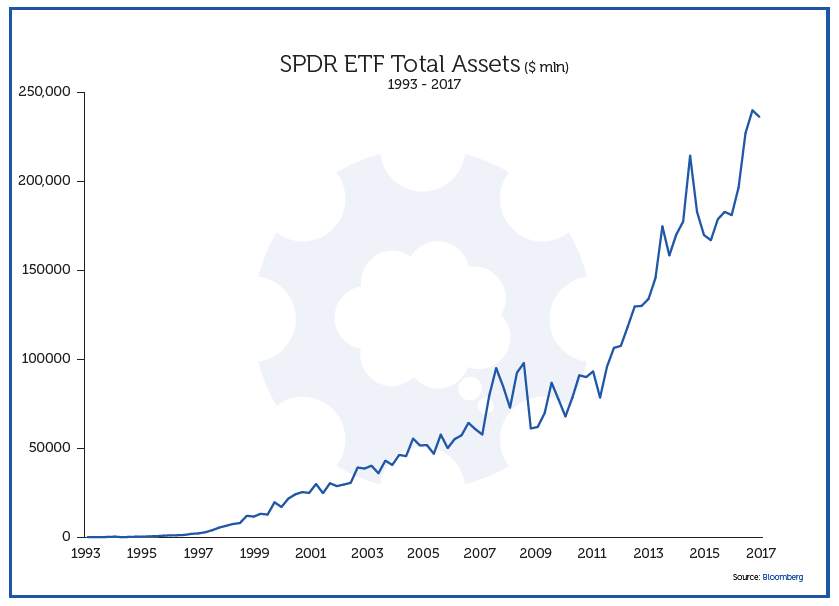

Total assets of the SPDR ETF grew from $133 million at launch to its current level of $236 billion and, along the way, the proliferation of exchange-traded products has been extraordinary.

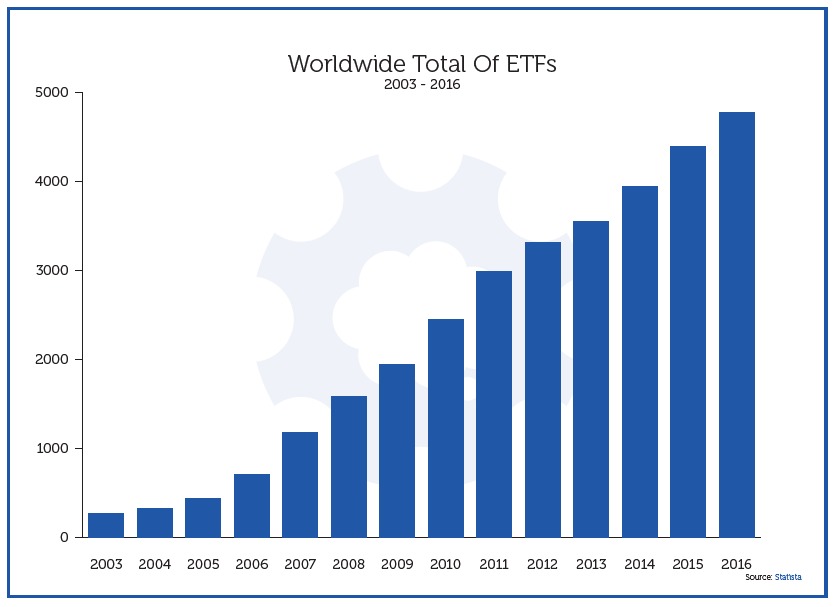

That one ETF in 1993 grew to over 100 by 2002 and almost 1,000 by the time 2009 was in the books.

By the end of 2011 there would be over $1 trillion of AUM parked in U.S. listed ETFs alone.

Meanwhile, the craze for low-cost, exchange-traded products had truly swept the globe with an astounding 3,000 products listed globally at that time—a number which has subsequently ballooned to 4800.

Along the way, some interesting correlations began to develop.

2003 marked the first year that ETF inflows exceeded those of mutual funds and, on a performance basis, it had become clearly measurable that, when market returns were poor, ETFs saw superior inflows but when market returns were positive, mutual funds gained the upper hand.

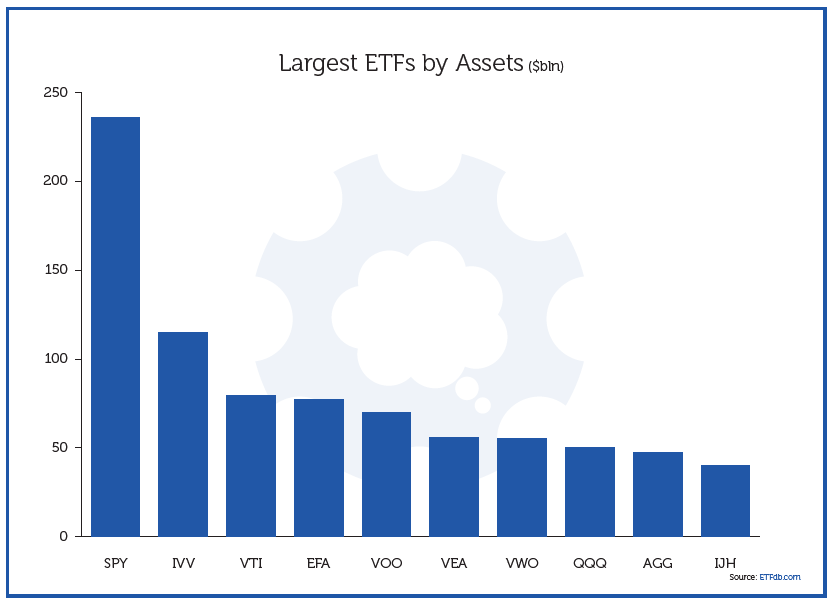

Currently, the top-10 ETFs alone boast total assets between them of $826 billion.

Since the Credit Crisis, the move to passive investing has picked up steam to a degree which, while perfectly understandable, has confounded many market observers.

Simply explained, as interest rates have plunged to essentially zero (and been artificially pegged there by the geniuses at the helm of global monetary policy), removing as much frictional cost as possible has been uppermost in most investors’ minds.

In addition, having been scarred by the events of 2008, investors have decided to embrace their inner Bogle and just get long indexes.

Why be cute?

This has resulted in a monumental shift away from active management and, in perhaps the greatest example of reflexivity to be found anywhere in markets replete with such things, has exacerbated the negative performance of active managers—most of whom refuse to chase index-leading darlings such as the ubiquitous FAANG stocks but who meanwhile see themselves underperform to a degree with which they are completely unfamiliar—which inevitably quickens the outflows from active to passive yet further.

…

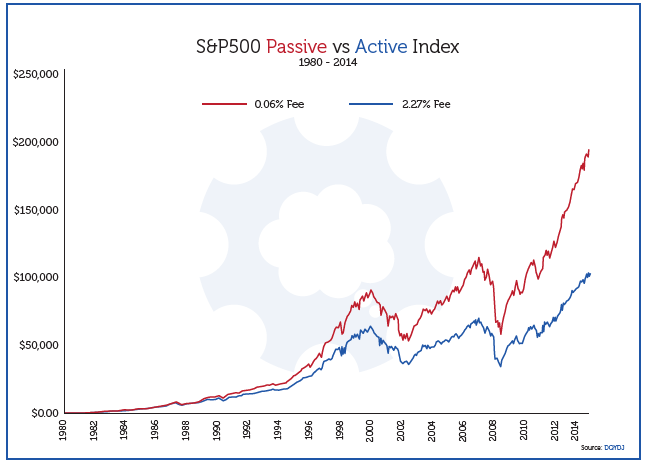

In case there are any remaining questions about why money keeps on piling into passive strategies, Exhibit A can be found in the chart below.

Fortunately, we don’t need an Exhibit B to allow our case to rest— this is easier to understand than the rules of hopscotch.

…

Simply put, products which allow investors access to instant liquidity around the clock have proliferated in an era when liquidity has not only never been more abundant, but has also been wholly necessary to both create the rising markets which have been the genesis of these products, and simultaneously avert another 2008-style crisis.

Of course they have.

Of course they have.

This deluge of nearly 5,000 ‘access products’—all of which purport to offer instant liquidity—have not only encouraged speculation (the antithesis of the rationale behind the original Index Funds) but they have never been tested in the white-hot cauldron of markets allowed to trade freely in both directions.

That could will be a huge problem.

But don’t take my word for it. Ask Jack Bogle:

“ETFs have become a marketing and promotional game. Those kinds of things are great for marketers but bad for investors,” says Bogle, in an August telephone interview, on vacation in the Adirondack Mountains. “The ETF has become a heavily traded vehicle used for speculation, often on indexes without much claim to fame except that they have new ideas some marketers want to test on unsuspecting investors. The proliferation of “fringe element ETFs” has resulted in “a quagmire of choices—everybody’s trying to be more creative than the next guy. So there are ETFs of dubious credit quality, leveraged ETFs, people creating their own investment ideas, their own indexes. All that has led to speculation.” (Think Advisor)

…

How crazy have things gotten? Well anybody who listens to the Adventures in Finance podcast will have heard this a few weeks ago but for those of you who haven’t subscribed (yet!!), here’s what I think may be the clanging bell chiming at the turning point for ETFs:

The Securities and Exchange Commission on Wednesday gave the green light to quadruple leveraged exchange traded funds, in a sign that previous concerns about this type of investment will not carry through to a new team at the regulator.

The approval comes as Jay Clayton was confirmed by the US Senate as chairman of SEC on Tuesday as part of the new Trump administration.

The regulator approved the ForceShares Daily 4X US Market Futures Long Fund, which will use the ticker UP, and ForceShares Daily 4X US Market Futures Short Fund, which will use the ticker DOWN. The former is designed to produce four times the daily performance of the S&P 500 index futures and the latter four times the inverse of the daily performance of index futures. (Financial Times)

The ability to offer people an easy way to get exposure to instruments they have no business trading (retail investors and inverse VIX ETFs spring immediately to mind) is bad enough, but to then offer them ways to lever that exposure via products which simply don’t offer them the clean 2x or 3x performance they expect is borderline disgraceful—but when the crowd is baying, you give ‘em what they want.

It will not only end, but end badly.

…

The point I have been making for some time now bears repeating: in a rising market, there is always an offer. 24 hours a day. 7 days a week.

Now, you may not like the offer (it may be 10%, 50% or even 100% higher, than the last traded price) but someone, somewhere will make you an offer in that asset in the belief that, should you avail yourself of their generosity, they will be able to turn a handsome profit by arbitraging the difference between your lack of patience or surfeit of necessity and their own time horizon or heightened level of risk tolerance.

In a falling market, none of that last paragraph applies. All bets are off.

In a falling market, the bid is sometimes often zero.

Every Flash Crash we have seen in recent years, as the number of ETFs has surged and the volume of high frequency & algorithmic trading has soared, has been nothing more than a dress rehearsal for the day when this market finally turns. These aren’t ‘fat fingers’ and, what’s more, I’m delighted to say that Jack Bogle agrees with me:

“ETFs probably have a turnover rate of 700% per year. That is staggeringly high by any measure. The mutual fund industry, in general, has a turnover rate among shareholders of 30% to 35%, a three-year average holding—which I myself think is amazingly short. Sixty percent to 70% of securities that were suspended were ETFs. Of course it can happen again! With high frequency trading, we have a system that seems out of control. We’ve created a kind of Frankenstein’s monster.” (Think Advisor)

A Frankenstein’s monster is exactly what we have created and in the coming weeks I will expand upon this idea and take a deeper look at some of the ways ETFs are setting investors up for a nasty surprise when the market finally turns—and turn it inevitably will.

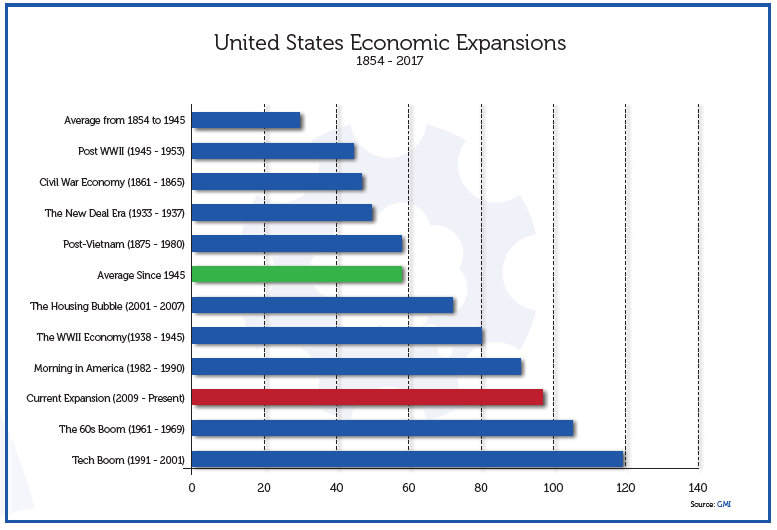

As the now 2nd-longest expansion in U.S. history moves closer to its eventual end, the stakes are being raised with each passing week and the chorus of those warning about the possible damage that the next U.S. recession will cause grows louder at every turn.

…

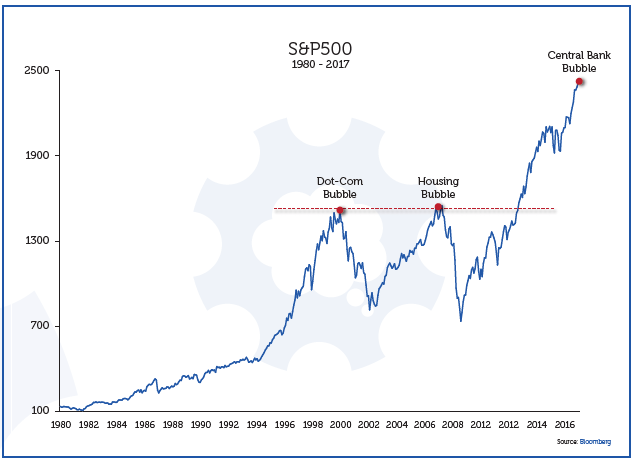

While anyone who either stayed on the sidelines for the last phase of the bull market or has been steadily raising cash (both of which would apply to your humble scribe) has watched the S&P 500 go sideways for two years before leaping higher by 20% in the last 12 months, the air is getting more and more rarefied up here as a simple step backwards demonstrates all too clearly.

Pop Quiz: Does that chart look either:

a) sustainable or;

b) something which will correct ‘quietly’

Yeah. I don’t think so either.

The problem is not so much that the market is due for a correction but the potential magnitude of that correction and, specifically, the amplifying effect that the massive expansion of the ETF market may have on the eventual outcome.

…

Until then, pay attention to the small print of any ETFs you may own in your portfolios.

All is decidedly not as it seems.

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.