Medicare is the federal health insurance program available to Americans at age 65, covering a range of medical services from hospital stays to doctor visits, preventive care, and prescription drugs. For most people, it becomes the foundation of their healthcare coverage in retirement, but navigating the program can be very complex. With multiple parts, enrollment deadlines, income-based surcharges, and coverage gaps that can reach into the tens of thousands of dollars annually, the decisions you make around Medicare can have a lasting impact on your financial plan. Getting it right requires more than just signing up on time.

Medicare coverage is not a one-time checkbox; it's an ongoing part of your financial plan that needs to be assessed on a regular basis. If you're approaching 65 or have already enrolled, we encourage you to review your coverage and costs with your wealth consultant and tax advisor to make sure Medicare is working for you within your broader financial plan.

1. Understand Your Enrollment Window

Most individuals become eligible for Medicare at age 65 and have a 7-month initial enrollment window: the three months before your birthday month, your birthday month itself, and the three months that follow.1

If you're already receiving Social Security benefits, you'll be enrolled in Medicare Parts A and B automatically. If not, you'll need to sign up proactively.

Still working at 65? If you're covered by a health plan through your employer (or your spouse's employer), you can delay Medicare enrollment without penalty. You'll have a Special Enrollment Period to sign up once that employer coverage ends. Importantly, once you retire and lose that coverage, you have eight months to enroll in Medicare before penalties kick in.

Missing that window is costly. Late enrollment penalties are not one-time fees — they follow you indefinitely:

2. Know What Medicare Covers (and What It Doesn't)

Original Medicare consists of two parts:

What it does not cover is equally important to understand: most long-term care, routine dental, vision, hearing, and - in most cases - healthcare received outside the United States.

You have two paths to fill those gaps:

Original Medicare + Supplement: A Medigap (supplemental) policy layers on top of Parts A and B to cover cost-sharing like deductibles and coinsurance. You would add a separate Part D plan for prescription drugs. Many Medigap policies also include foreign travel emergency coverage, which is worth noting for clients who travel internationally.

Medicare Advantage (Part C): An all-in-one alternative that often bundles drug coverage and may include dental, vision, and hearing benefits. The trade-off is that you're typically limited to a network of providers — something to evaluate carefully if you have long-standing relationships with doctors and specialists.

3. Avoid the HSA Trap

This is one of the most commonly overlooked pitfalls for individuals who continue working past 65.

Once you enroll in Medicare, you can no longer contribute to a Health Savings Account (HSA) paired with a high-deductible health plan. The IRS treats any contributions made after Medicare enrollment as excess contributions, subject to a 6% excise tax annually until the excess amounts (plus earnings) are withdrawn.

The timing here is subtle: if you sign up for Social Security at or after age 65, Medicare Part A enrollment is often retroactive by up to six months. That retroactive coverage can inadvertently create excess HSA contributions for months you thought were fine.

The rule of thumb: Stop HSA contributions at least six months before you plan to enroll in Social Security or Medicare. Your advisor and tax professional should coordinate this before any enrollment decision is made.

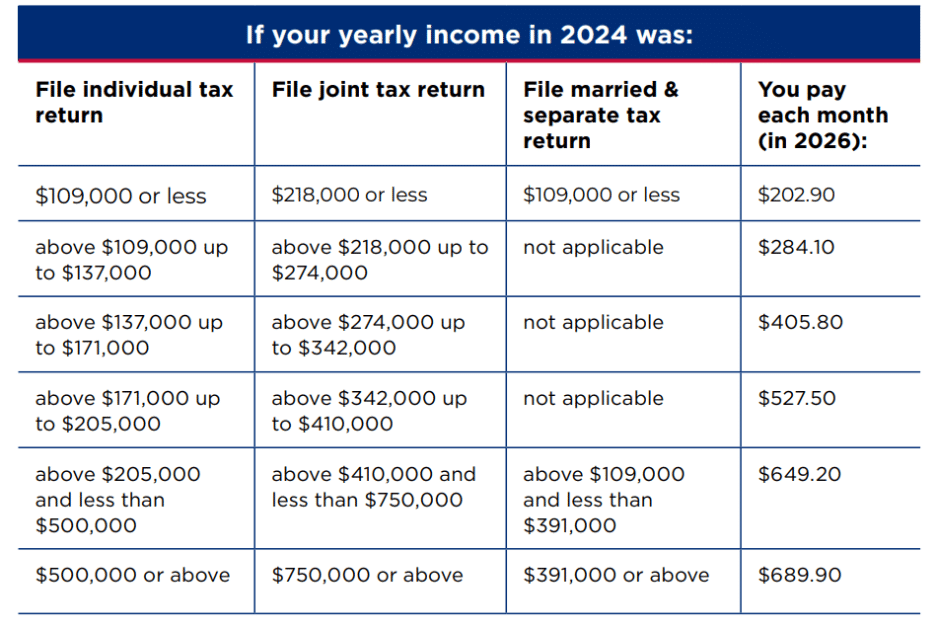

4. Plan for IRMAA — Especially Around Large Income Events

If you are in a higher income bracket, you'll pay more for Medicare. The Income-Related Monthly Adjustment Amount (IRMAA) is a surcharge added to your Part B (and Part D) premiums based on your income from two years prior.

In 2026, the standard Part B premium is $202.90 per month. That surcharge begins once income exceeds $109,000 for single filers or $218,000 for joint filers — and can reach as high as $689.90 per month at the top tier.

This two-year lookback creates planning opportunities — and traps:

Roth conversions and capital gains realizations can push you into a higher IRMAA bracket. Because you cannot request a new determination based on these types of income events, the surcharge sticks. Ideally, large taxable events like these should be timed at least three years before Medicare begins, and coordinated with your tax advisor to stay under the applicable thresholds.

Life-changing events — the death of a spouse, divorce, stopping work, loss of a pension, or loss of income-producing property — do allow you to request a new IRMAA determination from the Social Security Administration. If any of these apply, don't assume the surcharge is fixed; consider filling out form SSA-44.

Strategies to manage IRMAA over time:

5. Don't Set It and Forget It

Enrolling in Medicare is not a one-time decision. Plans change every year — benefits, formularies, provider networks, and premiums all shift. Open enrollment runs from October 15 through December 7 each year, and any changes take effect on January 1.

Each fall, review the Annual Notice of Change from your current plan. Then take time to compare your options:

You can compare plans at Medicare.gov/plan-compare, call 1-800-MEDICARE (1-800-633-4227), or work with a licensed Medicare broker who can walk through your specific situation. Given the complexity, a coordinated review with your financial advisor, tax professional, and a Medicare specialist is worth the time each year.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.The information provided is general in nature and should not be considered legal or tax advice. Consult an attorney, tax professional, or other advisor regarding your specific legal or tax situation. The items included in this publication are our opinion as of the date of this piece, not all encompassing, and are subject to change without notice. This material has been prepared or is distributed solely for informational purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any tax or legal advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.