“Just because a reversal of something unsustainable hasn’t happened yet doesn’t mean it won’t.”

-Seth Klarman, one of the most successful investors of the last 30 years.

“There is too little economic risk-taking and too much financial risk-taking.”

-Christine Lagarde, head of the International Monetary Fund (IMF)

One of my regrets from the ill-fated summer of ’07 is when I edited out a quote that was destined to become infamous in the fullness of time. It was uttered by Citigroup’s then CEO, Chuck Prince, and it basically said as long as the music was still playing (meaning the liquidity spigots were still wide open), Citi would keep dancing. A little over a year later, the global financial system was on life-support and Citigroup stock was break-dancing its way to $1 per share from over $50.

At the time, my gut told me that Mr. Prince’s quip would come back to haunt him. It also occurred to me that it was one of the most succinct examples of the devil-may-care attitude prevailing back then among most of the leaders of the financial community, not to mention regulators and the Fed. But, alas, for some long-forgotten reason, I left it out. In this week’s EVA, Gavekal’s Joyce Poon resurrects Mr. Prince’s exceedingly ill-advised sound-bite and discusses the similarities with today.

Nobody likes a kill-joy, though, and Evergreen is certainly enjoying riding the market wave right now. This is especially the case since some of the most battered asset classes from last year—which we were consistent buyers of—are in the vanguard of the current market rally. However, it’s only realistic to realize that the central banks are at the controls of the wave-making apparatus. In other words, it’s not the usual bull market drivers—such as strong earnings, rising productivity, an improving regulatory environment, swelling societal confidence, et al—that are at work these days. In fact, all of the above have been heading in the wrong direction over the past couple of years.

In addition to Joyce, another one of Gavekal’s most astute young analysts is Tan Kai Xian. While he’s skeptical this central bank-contrived nirvana will persist, he notes that the gap between corporate America’s cost of capital and its returns thereon remains quite wide. This is similar to Evergreen’s focus on credit spreads* which also continue to be very well-behaved, implying a recession is not imminent. However, the sharp downtrend, particularly in return on invested capital (ROIC) is concerning, and deserves close monitoring.

Next up is Gavekal’s Tokyo-based analyst Neil Newman. He examines the continuing disappearance of the Japanese government bond (JGB) market. The Bank of Japan (BoJ), its equivalent of the Fed, is buying such a large quantity of new issuance that in three years there may not be a traded market in these securities. Besides driving Japanese bond yields below zero (out as far as 10 years), it is also encouraging Japanese investors to seek the higher returns available in the US debt market. This is another supportive factor for US-based income securities, including corporate bonds.

Then, Joyce and Udith Sikand make the case that certain emerging market bond markets look attractive. It is a view with which Gavekal’s US-based money management operation (aka, Evergreen Gavekal) concurs, especially when it comes to Mexico.

Finally, the last two pages give readers a handy overview of Gavekal’s views on various markets and key themes by its very deep analytical team. For institutional or high net worth investors who are interested in subscribing to Gavekal’s regular research stream, please contact Steve Miller at smiller@gavekal.com.

View the Gavekal Chartbook here.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

*The yield gap between government and corporate bonds.

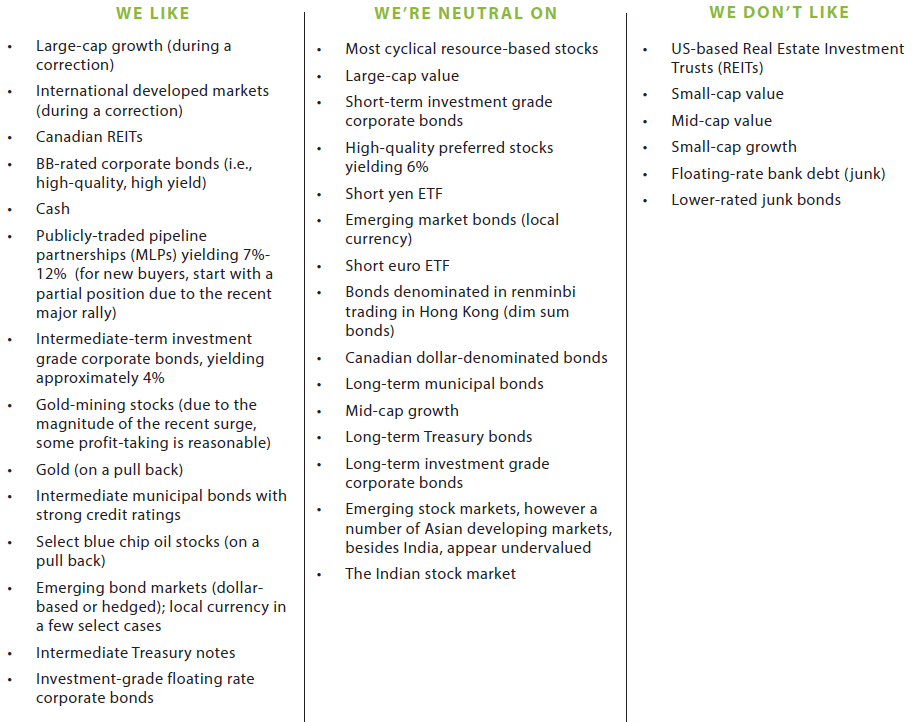

OUR CURRENT LIKES AND DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.