“We can’t solve problems by using the same kind of thinking we used when we created them.”

-ALBERT EINSTEIN

In this month’s edition of our Gavekal-authored EVA, we are giving readers a sample of three different views from our partner firm. It’s fair to say that Gavekal’s deep team of analysts provides some of the most comprehensive insights on global economic, financial, and political trends. It’s also not an exaggeration to say that their global footprint is extraordinary.

In today’s first section, Tan Kai Xain and Simon Pritchard discuss the growing likelihood of some type of fiscal splurge in the US—probably heavily focused on infrastructure build-outs and upgrades—as well as the road-blocks such a program would need to overcome. As EVA readers may recall, Evergreen has long believed a well-designed “domestic Marshall Plan” would almost assuredly produce a significant boost to the US economy. The key, of course, is “well-designed”, which, given our current cast of political actors, may well prove extremely challenging.

In the second part of this Gavekal EVA, Rosealea Yao takes us half way around the world to China, arguably the planet’s other most critically important economy. No doubt most EVA recipients have been following reports out of that nation on its remarkable housing bubble, at least in major cities. But relevant to the point of her brief essay, the fundamentals of the Chinese commercial property market are even more ominous. This appears to be particulary true in retail development where, as in the US, e-commerce is putting severe pressure on bricks and mortar stores.

Thus far, China has been able to avoid a day of reckoning for its massive bubbles in residential and commercial real estate. Perhaps the modern-day mandarins over there will be able to continue delaying any kind of Thelma and Louise (i.e., off the cliff) moment. Yet, there are clearly some points of serious stress accumulating in the Middle Kingdom that might defy its command and control model. It’s just another one of those “fingers of instability”, as my friend John Mauldin calls them, that have the potential to destabilize exceedingly complacent financial markets, particularly in the US.

Speaking of the United States, Charles Gave, one of my most important intellectual influences, confesses his confusion on the current status of the US economy in this EVA’s final short installment. In doing so, he makes an admission that most of you have often have read from yours truly, such as when I’ve referenced Edward R. Murrow’s famous quote: “Anyone who isn’t confused clearly doesn’t understand the situation.” As even Fed vice-chairman Stan Fischer conceded recently in Jackson Hole, there is enough conflicting information on the US economy that one can come to nearly any conclusion about its present condition.

Yet, both Charles and I are becoming increasingly alarmed about the erosion in a wide array of “real economy” datapoints. In his piece, he gives a concise overview of these even while conceding the dramatic improvement seen since early February in almost all financially-driven indicators, especially our favorite stress measure—credit spreads. But as Louis Gave and I discussed over Labor Day weekend, up at Louis’ beautiful home in Whistler, B.C., it’s possible that with the European Central Bank buying so much US corporate debt, spreads aren’t as meaningful a heads-up factor as they once were. But that’s a topic for an upcoming Random Thoughts edition of this newsletter. For now, it’s Gavekal time.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

*The difference between government and corporate bond interest rates.

By Tan Kai Xian & Simon Pritchard

More than three years after the world fretted about the US economy falling off a “fiscal cliff”, there is suddenly much talk of government spending being used to gin up growth. Whatever their many differences, both Hillary Clinton and Donald Trump favor a fiscal expansion, with a focus on upgrading the US’s aging infrastructure stock. At the same time Federal Reserve officials, led by Janet Yellen and John Williams, are arguing for more fiscal support in a call which effectively admits that monetary policy has run out of road as a stimulus tool.

These calls reflect a potentially powerful intersect of intellectual opinion among policymakers and the rawer political expediency that drives US election campaigns. The American public experiences badly maintained roads, bridges and airports on a regular basis and the first chart shows their rapid aging. Moreover, the link between “crumbling infrastructure” and the broader issue of US prosperity has been made by lobby groups such as the American Society of Civil Engineers, which recently claimed that US GDP could take a US$4trn knock between 2016 and 2025 due to lost sales and rising costs associated with bad infrastructure (see report). What grabs us as especially interesting is to hear the likes of Fed Vice Chair, Stanley Fischer pitching into the debate by arguing that spending more on public infrastructure could improve productivity growth, which sits at the heart of concerns about “decline” and “secular stagnation”.

The problem with this argument is that the purse strings of the US government are controlled not by the president or the Federal Reserve, but by the people’s representatives in Congress. And whether it is Clinton or Trump who takes the presidential oath on January 20, they will face the constraint of the Budget Control Act of 2011 which established a hard cap on discretionary spending lasting until 2021. That spending is expected to rise by just US$25.4bn in 2017 and contract by -US$2bn in 2018 according to forecasts released last week by the Congressional Budget Office.

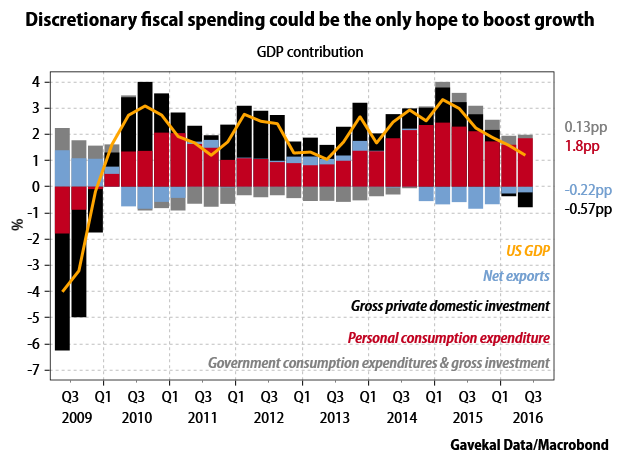

One possibility is that come November a changed configuration in both the House of Representatives and Senate allows for an amendment to the Budget Control Act. That puts us in the realm of political tea leaf gazing, which is not Gavekal’s game, but it is worth considering the economic context in which such discussions may be taking place. Consumption has been the key driver of the US economy in the last two quarters (see chart to the right), yet the latest reading of the Conference Board’s consumer confidence expectation index, which leads actual consumer spending by about two months, points to flat consumption. Capital spending (ex-residential) is unlikely to ride to the rescue as it is closely tied to corporate sales, which remain weak. Residential investment is similarly likely to stay sluggish, due to the tightness in bank lending standards.

Taken together, it is entirely possible that by early next year growth will be on a clear weakening track, while inflation is edging higher, forcing the Fed toward a tightening bias. With monetary policy unable to act as an effective counter-cyclical tool, the policy discussion would likely quickly turn toward fiscal policy. And the fact that intellectual opinion, as well as a broad spectrum of political opinion, seems to be focused on fixing the country’s infrastructure, it seems fairly clear what could well be the next big government initiative to support the economy.

By Rosealea Yao

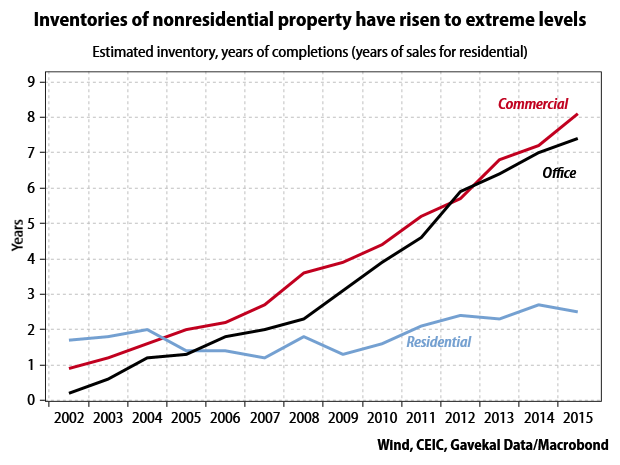

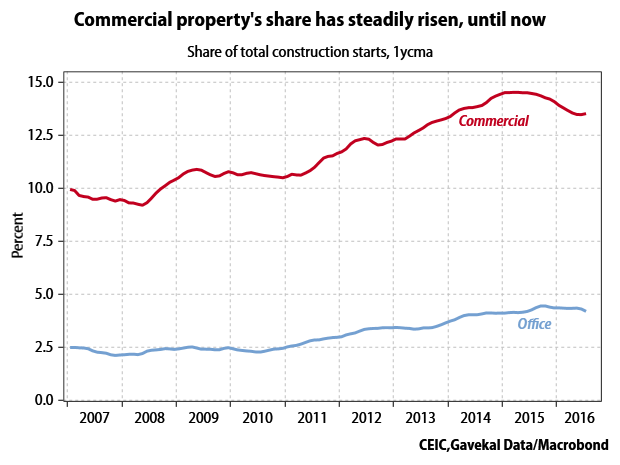

China’s inventories of unsold housing are a national problem, so officials are allowing a huge expansion of mortgage lending in hopes of soaking up the excess supply. They should spare a moment to look at the even more enormous overhang in the non-residential property market. While housing inventories are now under two years of sales, on my estimate the pipeline of unsold commercial and office property will take at least eight years to digest. The irrational exuberance that has underpinned commercial property construction for years is now, finally, showing signs of deflating. But this sector of the property market will be a drag on overall construction growth for the foreseeable future.

Regular readers should be familiar with my simple method for estimating the inventory of residential property: the difference between cumulative starts and cumulative sales. I use a similar method to estimate inventories of commercial and office buildings, but with cumulative completions rather than cumulative sales. This is to account for the fact that developers often rent rather than sell commercial property. Such a procedure shows that started but uncompleted commercial properties were equivalent to 8.2 years of completions in June, and 7.8 years of completions for office properties. In absolute terms, commercial inventories were 1bn sq m and office inventories 270mn sq m—frighteningly high compared to 2.4bn sq m of residential inventories, given that non-residential construction accounts for only about 20% of construction starts. If anything, the actual level of nonresidential inventories should be even higher, as the simple assumption underlying the estimate—that completed buildings are never inventory, i.e. that they are always immediately occupied—is overly strong.

It is not hard to find signs of excess supply. The most common type of commercial space is the first couple of floors in residential high-rises, which are usually allocated to shops to serve the residents. When the residential units are not full, there is little incentive for shops to open. On a recent visit to Xianghe, a county in Hebei bordering Beijing, I saw rats running in broad daylight through the empty storefronts in one project, which looked to have about 40% occupancy. The new business district of Xiangluowan in Tianjin, sometimes called the Chinese version of Manhattan Island, will also take any visitor’s breath away—not just because of its size but because its office towers are mostly empty. In Ningbo, nearly 60 shopping malls around the city are desperately competing to attract enough stores; according to a recent report, some mall managers are not even taking rent but are paying retailers as much as RMB4,000 per sq m. In Shenyang, which the China Index Academy rates as having the largest excess supply of commercial real estate, the local government plans to start remodeling unwanted commercial projects into residential ones.

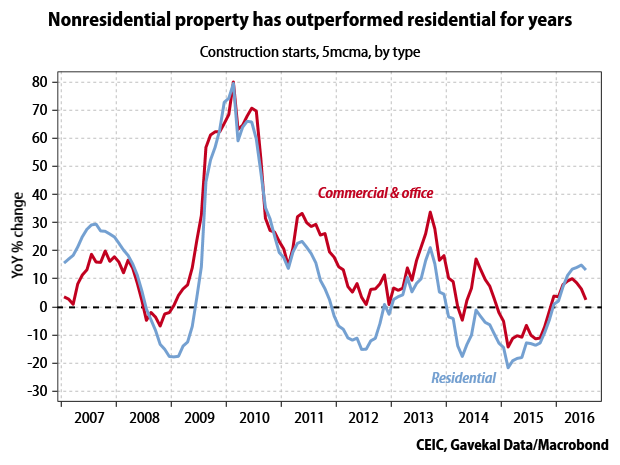

The unvarying trend in these commercial and office inventories is quite striking: nonresidential inventories have been steadily rising for more than a decade, though the increase became more rapid after 2009. Even official measures of commercial and office inventory—which are based on a very narrow definition of completed but unsold buildings—have roughly tripled since 2010. Housing inventories show relatively clear cycles, and marked regional differences; commercial property inventories display neither. All this suggests that the buildup of nonresidential inventories is a nationwide phenomenon quite distinct from housing inventories.

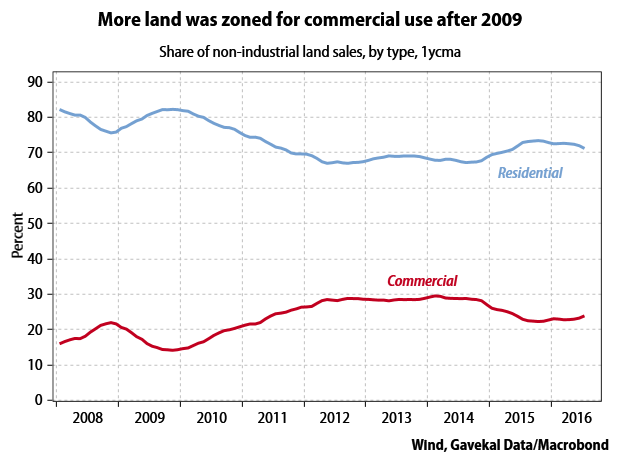

The data show that nonresidential construction rarely outperformed residential construction before 2008 but did so consistently afterward: nonresidential starts almost always grew faster than residential starts, whether in an upcycle or a downcycle. In other words, the share of commercial and office space in total construction starts has risen consistently in recent years. The best explanation is probably a systematic planning bias caused by the local governments that guide development through land use. The widespread notion that China was becoming a “consumption driven” economy may have led localities to encourage more commercial property, seeing retail space as the most obvious way to profit.

The recent popularity of large mixed-use property developments is one example of how this trend has played out. In contrast with the older model of dedicating one or two floors of a residential building to shops, these are more ambitious combinations of high-end apartments with malls, cinemas, hotels and office spaces in a single complex. Some developers, such as Wanda, have indeed been very successful with these projects, and other developers are now eagerly replicating them across the country. Local governments also favor these projects as they are visually impressive and a sign of local prosperity. A report by Knight Frank in 2014 estimated that the total stock of such developments was rising more than 20% annually, and will exceed 1,000 projects (or 430mn sq m) in 49 cities by 2016.

The problem of course is that this new wave of investment into space for retailing has coincided with a massive structural shift of consumer spending online, away from physical retail channels. At the same time the changing structure of the economy has resulted in slower rather than faster growth in consumer spending, with much of the growth coming in services other than traditional retail. While it has taken some time for the reality of steadily-rising inventories to change developers’ minds, the blind optimism on commercial property finally seems to be fading: the share of commercial and office space in construction starts has started to decline for the first time in years.

Yet it is unlikely that even the epic scale of today’s nonresidential property inventories will lead to a complete collapse in this type of construction. This is simply because much nonresidential property is built more or less automatically as a consequence of residential construction (all those ground-floor stores in new high-rise buildings). Local governments will still need to ensure that new housing developments have the shops they need; while the share of land use going to retail space will decline, it will not go to zero. Historically the construction cycles for residential and nonresidential property have been basically identical: nonresidential property does not follow an independent driver. So what is more likely to happen is that nonresidential property goes from being a boost to the residential cycle (making upturns higher and downturns shallower) to a drag (making upturns lower and downturns deeper). This is yet another reason, along with the long-term peak in housing demand, to be very cautious about the future growth of construction in China.

By Charles Gave

Friday saw the release of US jobs market data for August which had investors convinced of a continued “not too hot, not too cold” outlook for the world’s largest economy. This is at odds with the view that I have held for a while; namely, that the US has been on the brink of recession or may have even entered one. This prognosis was based on a hopefully not insubstantial analytical foundation, which may be worth reviewing.

Let’s start with economic activity:

1) Private sector GDP: The 12-month rate of change stands at 1.3% YoY, a level which since 1968 has always coincided with a recession.

2) Industrial production: The six-month moving average of the 12-month rate of change has been negative for a good while, which since the 1930s has never occurred outside of recession conditions.

3) Non-financial profits (national accounts): Since the 1950s these have not been lower than three years ago without a recession (save 1986-87).

4) Capital spending: The two-year rate of change is negative and (save for 1987) this situation has always coincided with a recession.

5) New home building permits: The 12-month rate of change has swung negative, which has often been a recession signal.

6) Exports: The six-month moving average of the 12-month rate of change has gone negative, which has almost always coincided with a recession (there have been recessions with export growth).

7) Industrial sales: The Year-over-Year (YoY) change is in negative territory, which has usually been associated with a recession.

8) Tax receipts: The six-month moving average of two year variations is negative, which has never happened outside of a recession.

9) Employment: Variations on a 12-month basis remain positive, but are decelerating. This tends to lag economic growth by about a quarter.

10) Consumer spending: Real retail sales are generating about 1% growth, yet consumer spending above 2% YoY (Obamacare impact?).

Also consider the following (non-output related) base data.

1) US real monetary base: The 12-month variation is negative, which has always coincided with a recession (there have also been quite a few recessions when real base money was rising on a YoY basis).

2) Corporate spreads: There has been a massive narrowing since February with Baa and junk bonds yields falling faster than economic activity.

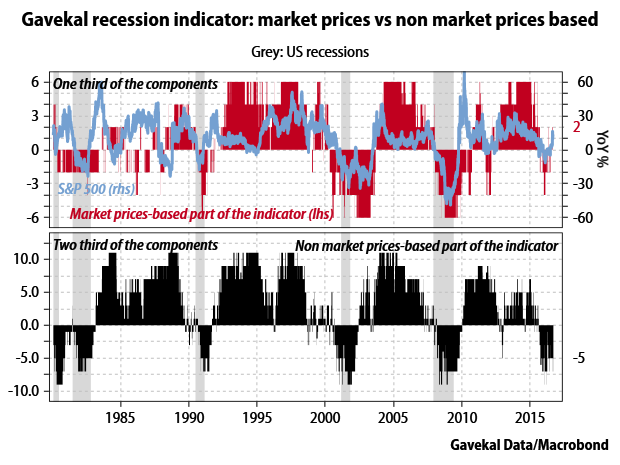

A little more than a year ago, I built a recession indicator for the US economy which included most of the factors mentioned above. The recession frontier of this tool stands at --5 and in the intervening period the reading has varied from 0 to -9. It is now recording -3.

In order to better understand the reasons for this recovery, I have broken the recession indicator into two parts, with the first part being based on the official data, and the second being derived from market-based measures such as corporate spreads, commodity prices and equity indexes. The former “hard” data makes up about two-thirds of the indicator and the latter, “market” or “forward-looking”, part constitutes about one-third. It is in this market part where all the improvement has been registered, with the reading rising from a low of -4 early in the year to +2 (see chart below). By contrast, the hard data piece of the indicator has maintained a steady deterioration, with the subset reading going from –3 to –5. The one similar, although not as pronounced, situation was in 1999.

So how to explain this seeming dissonance? On the one hand, US financial markets have since February been heralding an improvement in the US economy, which six months on, is nowhere to be seen. Or perhaps the markets simply operated on the basis that the Federal Reserve would do whatever it took to avoid a recession in a presidential election year. Or perhaps central banks really did coordinate after the Shanghai meeting of G20* finance ministers in February as part of a concerted global price-keeping operation** (see video interview with Louis where he considers this possibility). Whatever the reasons behind the pick-up, it seems clear that the US economy must now start to recover, or alternatively the market-based components of my indicators could soon roll over.

It seems clear that the non-services part of the US economy is in a recession and has been for a good while. Moreover, I cannot remember a time when the Fed would have considered raising rates while the industrial economy faced such a situation. As such, raising interest rates at this juncture would constitute a significant policy mistake (which is precisely why it is quite likely to happen). To understand why this outcome is likely, it is only necessary to note that not raising rates would constitute an admission that the policy settings of the past five years have failed. Sadly, I cannot find a neat conclusion to this very messy and muddled tale.

*Leading countries

**I.E., propping up financial markets

OUR CURRENT LIKES AND DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.