“The past decade of government and Fed profligacy is not his fault, but that still isn’t an argument for recklessness. If this ends in tears, Mr. Trump will get the blame.”

-GEORGE MELLOAN, Former deputy editor of the Wall Street Journal, from today’s edition of that paper.

By David Hay / CIO, Evergreen Gavekal

The Opinion Exchange. One of our primary goals with this newsletter is to provide our readers with a wide range of viewpoints. As noted previously, the risk with this is that we don’t convey a clear idea of our actual views. Yet, we’ve always felt that’s a chance worth taking, particularly since we try to subsequently clear up any ambiguities.

This month’s installment of our Guest EVA gives us the perfect chance for clarification. In last week’s Gavekal issue, we showcased the thoughts of its co-founder and senior partner, Anatole Kaletsky. It’s no exaggeration to say that Anatole is one of the most influential individuals in Europe, where he has served as a top adviser at the highest level for both businesses and governments. However, as I wrote last week, Anatole’s political views and mine are often extremely divergent.

The combination of my introduction and Anatole’s short essay did strike a nerve with a few readers, including a gentleman who writes a daily newsletter I almost always read, Tom Bentley. His response was so passionate that it caused me to ask him to write a rebuttal to last week’s issue. He generously offered to do just that, the product of which you will read shortly.

However, I also wanted to make this a point and counterpoint piece, giving me the chance to expand a bit on what I was trying to express. The most important aspect, at least in my mind, was the huge disconnect between how financial markets are behaving and how well—or not—capitalism is functioning for the typical American. Yet, first, let me quickly agree with Tom that I feel capitalism has been getting a bum rap for years because it’s been a very long time since it was allowed to operate without the “helping hand” of government. This is a topic near and dear to my heart, as regular EVA readers who saw my “war on the private sector” issue from last October may recall. Even last week, I pointed out the leading role government policies played in producing the housing crisis, the biggest financial fiasco since the stock market crash in 1929.

In Tom’s case, as you will read, he’s referring to that phenomenon as BUG: Big Unaccountable Government. And I need to admit right up front that Tom is smarter than I am. After all, he retired at 54 while I’m still putting in time-and-a-half on the downhill side of 61. Also, I love his suggestion of long conversations over martinis, preferably tall ones, and ideally in his present place of residence, Sun Valley, Idaho. Moreover, I don’t recall ever being accused of conventional wisdom but I kind of like it for a change. As wrong as I’ve been about the apparent immortality of this bull market in stocks, I’ll take being associated with any kind of wisdom, conventional or otherwise.

Naturally, I’ve got some disagreements with a few of his views. One of my counterpoints is that I believe bad policies have been very much of a bipartisan undertaking over the last 15 years or more. And while I’m not going to defend Anatole’s politics or beliefs, I do think he made some good points about the acute need for much better vocational training in the US (we could use a lot more newly minted welders and a lot fewer graduates in French Art History). It also makes sense, in my opinion, for our country’s unions to emulate Germany’s, which are far less adversarial than those in the US, as Anatole was suggesting. Maybe I’m just naïve—a potential trait that is tough to reconcile with my market skepticism—but I still believe there is such a thing as good government policies. However, it’s certainly been a very long time since we’ve seen much evidence of such.

It struck me as fascinating that Tom muses about the idea of taxing the super-rich at higher rates than those making $500,000 or so a year. That’s an idea that I believe Anatole would like very much. Personally, I believe the key to effective tax reform is to make the code immensely simpler, with lower rates—though still progressive—and very limited deductions. The main problem with our present tax system, in my mind, is its fiendish complexity.

As a further point of clarification, I didn’t use the term “white privilege” in an email response to him, but I did bring up the notion of luck, something I see almost nothing about in economic commentary. So, at the risk of losing my conventional-wisdom billing, I want to touch on that briefly.

First, there is what Buffett calls “the lucky sperm club”, those born into immense wealth. Then there are people like Tom and me, who just were in the right place at the right time. We worked hard for sure (as noted, some of us still are) but a lot of other people did, too, and they don’t have what we have to show for it—not even close. Maybe that’s because we’re smart (lots of EVA readers would question that supposition in my case) but isn’t that just another example of fortunate DNA?

Or perhaps you got hired by the right start-up and ended up with tens of millions in stock options. You hit the IPO jackpot but how many others deserved it just as much and didn’t get to ring the bell? One of Australia’s richest men once said words to the effect that any highly successful person who didn’t believe that luck played a big part in his or her success was an “arse”. I couldn’t agree more.

Therefore, I believe the best capitalist systems take luck into account through programs meant to offer opportunities to those stuck in tough circumstances through no fault of their own. The most successful societies are the ones where rising from the bottom rungs to the upper echelons can happen with the fewest impediments. It’s the constant rising up of the aspiring and hard-working—combined with the “shirtsleeves to shirtsleeves in three generations” phenomenon which often brings down the idle rich—that truly drives a nation’s prosperity. America did that exceptionally well for generations but somehow we’ve lost our way over the last decade or so (notwithstanding the overnight tech billionaire scenario which happens to a precious few).

Additionally, it’s only humane to provide the basic necessities of life for anyone unable to care for themselves. Yet, I love Tom’s line that the safety net has become a hammock. Both parties have taken turns destroying our national balance sheet with voting-buying programs. Even Anatole pointed this out last week in his section where he lamented the proliferation of lavish retirement programs, mostly benefiting older workers. It is, unquestionably, vital to have an incentive-based system which is why capitalism, if not subverted, works infinitely better than socialism. Or, said differently, socialism always and everywhere fails—it’s just a question of when.

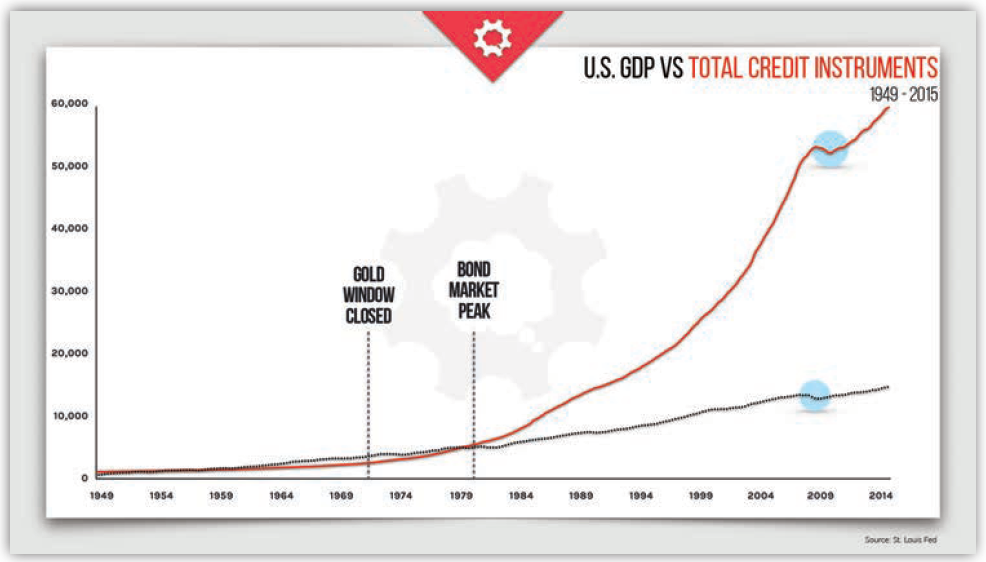

But this is meant to be primarily an investment newsletter; thus, it’s the impact on financial markets that we try to focus on most and that leads me to another major point I make repeatedly: the dangers of debt. Tom addresses this as well and blames it on BUG, as I alluded to in the previous paragraph. As you can see in the first chart below, it was about thirty years ago—during the Reagan and Clinton booms—that credit outstanding began to go viral.

OVER 30 YEARS OF DEBT GROWING MUCH FASTER THAN GDP

Source: Things That Make You Go Hmmm

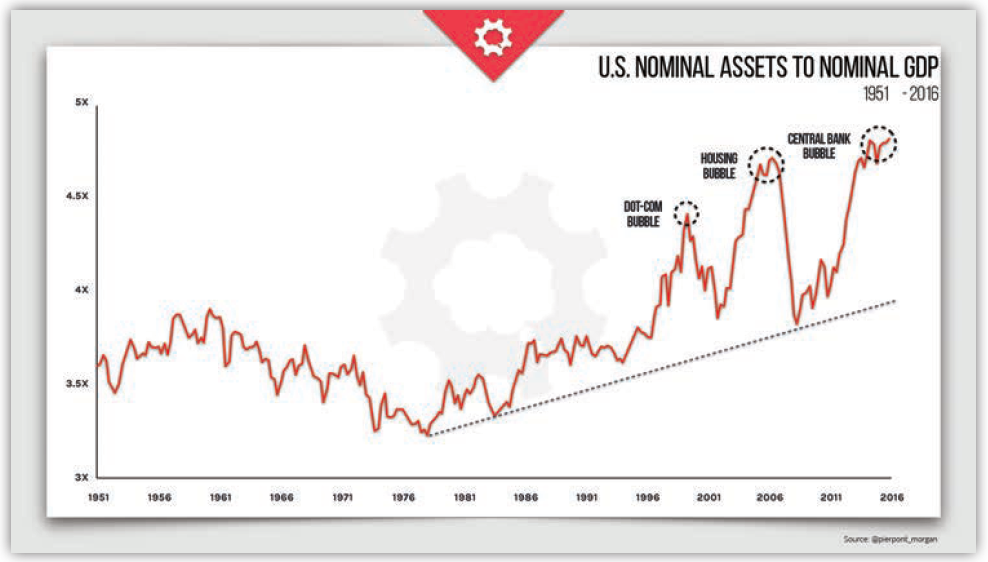

ASSET PRICES VS. GDP AT PAST BUBBLE HIGHS

Source: Things That Make You Go Hmmm

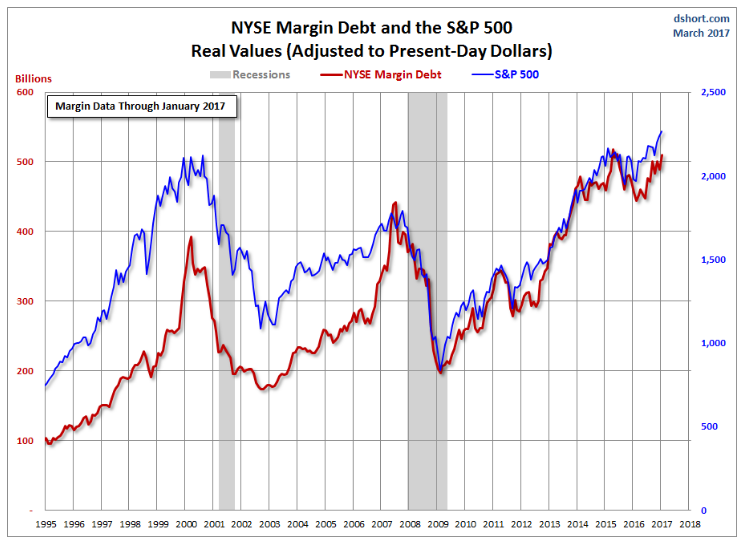

Source: Advisor Perspectives

History shows that capitalism has always been plagued by debt binges. The railroad booms and busts in the 1800s were a classic example of that, as was, much more cataclysmically, the 1920s stock market bubble.

But since debt began to do a moon shot in the 1980s, whenever there was a bust—like the crash of 1987, which should have purged the system of a lot of bad debt—the Fed intervened to prevent that natural reset from happening. This was a direct consequence of the now infamous “Fed put”. It’s also why we are currently at a dangerously extended level of asset prices relative to size of the economy as well as why margin debt is at a record high, even adjusted for inflation, as is so clearly illustrated in the chart above. In the latter case, the second longest bull market ever—heavily juiced by the Fed’s trillions of monetary steroids—has led investors to believe it’s safe to pile on the leverage, at ever higher prices. This has ended horribly twice in the last 17 years and I don’t see how this time will be any different.

It’s nearly irrefutable that this massive debt accumulation is a big reason asset prices are as inflated as they are. Also almost inarguably, this has made the rich much richer, at least on paper, a point Tom concedes. Meanwhile, an increasing percentage of Americans don’t own stock. As mentioned in last week’s issue, this is particularly true among millennials. That’s not good news for the long run health of capitalism.

Further, I believe the aforementioned massive debt build-up has facilitated the emergence of an ultra-rich class on a scale the world has never seen. This leads to an inequity of wealth, especially at the tail-end of a bull market in stocks and real estate. The late 1920s brought tremendous wealth disparities as well—and you know how that turned out.

Tom is a fan of John Mauldin, a familiar name to many EVA recipients. In John’s March 1st Thoughts From the Frontline, he had a section titled: “Angst in America”. It reads much like my introduction to our issue from last week. He observed that 10 million American males between the prime working ages of 24 to 64 have “literally dropped out of the workforce”. Of those, some 57% collect disability benefits! As I’ve relayed several times in the past, there is a disability epidemic going on in this country, even after eight years of economic growth. This is another clear marker something is seriously amiss.

(For a really deep dive into all that ails our country right now, I’d suggest you click on this link to a fact-based, non-partisan article I just read, “Our Miserable 21st Century”, courtesy of a thoughtful client who sent it my way.)

My goal with this isn’t to depress you but rather to shake all the investors reading this out of their complacency and excessive bullishness. This is the only mega-bull market (as opposed to cyclical rallies, such as we saw in the 1970s) I’ve ever seen in my nearly 40-year career that has coincided with such widespread societal fracturing and discontent. In fact, I don’t think there has ever been one like this in the history of our country. As you can tell, I’m standing by my contention made last week that tens of millions of Americans are scared—and I don’t care how high the S&P 500 is right now.

Frankly, my recurring nightmare is that Trumponomics disappoints at the same time the Fed is on a mission to “normalize” interest rates, leading to a stock market crash and another wicked recession. If so, the whipping boy will once again be capitalism and the stage will be set for a big leap leftward in 2020. The Democratic party is already being pulled hard to the port side by the likes of Bernie Sanders and Elizabeth Warren. I shudder to think what they will be telling America’s already disaffected young people at that time but I know for sure they won’t be extolling the wonders of our free enterprise, incentive-based system.

Hopefully, my nightmare is just that—a bad dream. Perhaps Mr. Trump and Congress can somehow avoid an explosive detonation of the asset bubbles that have built up over the last eight years. There are definitely some encouraging things happening, including a valiant attempt to reform the Affordable Care Act, certainly one of our nation’s biggest challenges. I wish them God’s speed but keep your seat belts fastened—it’s likely to be a wild ride.

QUIT APOLOGIZING FOR CAPITALISM!!!

By Tom Bentley

Your missive of March 3 was full of the conventional wisdom from Anatole and you, David, and as is often the case, the conventional wisdom is either partly or totally wrong. I’m not going to rebut all the points, just hit what I think were some of the more salient ones. I’ll begin with your comment, David: “Yet, it (Capitalism) has always struggled with equitably distributing the fruits of its awesome output.” Unequal distribution is a feature of Capitalism, not a bug. How do we create incentives without it? Don’t we all believe in meritocracy? Or, heaven forbid, do we think everybody gets not just a trophy, but the same trophy? In fact, our current income distribution (after transfers) is TOO equitable; we have removed the incentive to work for many people (as seen in declining labor force participation), and to pay for it we have increased penalties for working via higher taxes (high taxes in California are part of the reason I retired at 54). Capitalism worked better before our safety net became a hammock, and when we had lower taxes on investment (both on corporate profits and investment itself).

I will concede however, David, that you were partly right with your comment: the past 30 years has seen an explosion of income for the mega-rich. This is occurring not just in business but in almost every field—look at sports and entertainment—do you think Sam Snead could have foreseen that a golfer several generations later would make over one billion dollars, and he would be an African American? We can have long conversations over martinis about why this has happened, and whether it’s a good thing or bad thing, but for sure, it has happened. Moreover, not only have incomes at the very top gone way up, asset price inflation has also made the rich richer. The interesting part here is that it’s monetary profligacy combined with some well-intentioned (?) regulations that have boosted asset price inflation—and those are Democrat policies. Still, whatever one’s view of the good or bad of this phenomenon, I do wonder why our tax code maxes out at income under $500K, which is still far away from mega-rich; in fact, it barely pays for a middle-class lifestyle for families in Manhattan and SF. Why don’t we have higher brackets at $5M, $10M, $25M, etc.? Again, it’s the mega-rich who are skewing the data on income inequality. Why do we keep wanting to punish the merely well-off for that?

Next up, Anatole misses the mark: “By deregulating finance and trade, intensifying competition, and weakening unions, governments created the theoretical conditions that demanded redistribution from winners to losers.” Finance has been getting steadily more regulated, not less, for three decades now. Liberals have been bemoaning the decline of competition (Jason Zweig wrote about this in the Wall Street Journal last week) for years now….so which is it: too much Capitalism or too little? Governments didn’t weaken unions, the unions killed themselves, by wrecking competitiveness in the industries where they dominated. Federal government has always tried to strengthen unions, but they can’t reverse fundamental economics. If unions require businesses to pay workers more than their marginal productivity, those businesses will ultimately fail. Germany has unions that have shown themselves capable of working cooperatively with management towards the success of the enterprise, but not here—our unions only want more pay, more benefits, and more inefficient work rules.

Anatole contends, “Market fundamentalism conceals a profound contradiction. Free trade, technological progress, and other forces that promote economic ‘efficiency’ are presented as beneficial to society, even if they harm individual workers or businesses…” Ever since the industrial revolution began and humans clawed their way out of a subsistence existence that was “nasty, brutish, and short,” we have had economic dislocations. Let’s remember that some 80% of workers were once employed in agriculture, and now it’s 2%. The biggest change recently has been that Western governments and Japan have implemented broad safety nets to cushion the impacts of economic evolution, and indeed those programs have led to income disparity changing little in recent decades (as measured by consumption, not the false analyses we typically see of income disparity before all the redistribution we already do). But that safety net has its own unintended and adverse consequences—it reduces incentives for people affected by change to adapt to those changes by retraining or relocating, and it inevitably increases demand for even more redistribution (which has become the unifying force of the Democrat party).

The real enemy of the people and of prosperity is not Capitalism, it’s BUG (Big Unaccountable Government). One can draw a straight line between the increasing size and scope of government, and the economic malaise (secular stagnation) that has affected Western countries and Japan. BUG and BUG policies have led to an explosion of debt at all levels, and we all know that, inevitably, there is a limit to how much debt public and private sectors can absorb. The only question is, does the explosion of BUG and of the debt mountain end with a bang or a whimper? I prefer the explanation that the protagonist in “The Sun Also Rises” gave for how he went bankrupt, “Slowly at first, then quickly.” We are in the slow stage now, but we can see the bang on the horizon if we keep heading this way. Our only hope is to start NOW to scale back BUG and the debt explosion, yet politicians everywhere are offering the opposite.

David, in a subsequent message to me you expanded on the theme of Capitalism creating income inequality by pointing to debates we have had in recent times about what I’ll call “white privilege.” Indeed, in virtually every country you can name, there is a dominant culture and the members of that culture succeed at a higher rate than members of other cultures present in the country. This is a universal problem, yet Capitalism is the strongest tool we have to fight against white privilege, because it mandates inclusiveness. All you have to do is look at the largest and most successful experiment with “winner-take-all” Capitalism that the world has ever seen, which is the Silicon Valley, to see how inclusiveness has been a critical part of that success. American corporations dominate on the world stage; half of the largest companies are domiciled here (and many of the rest are state-owned monopolies), and inclusiveness has been a major reason for that. So I will concede that white privilege is a huge problem here, and it has brothers and sisters in every country, but Capitalism is the cure, not the cause.

Overall, Capitalism is every bit as great as it ever was, and maybe even greater in its current iteration, especially the way we practice it in the US. However, BUG has been getting BUGgier since Reagan left office, and in the time of Clinton we covered it up by having demographics (baby boomers) and the tech revolution as tailwinds. Those tailwinds have now become headwinds, so we can’t get away with “soft Socialism” and piling on debt any more, we have to get back to the fundamental principles that have always succeeded and always will—free markets under rule of law, and an open society that creates opportunities for the animal spirits that dwell in all of us. We need to quit apologizing for Capitalism, and start pointing the finger where it needs to be pointed, at BUG and the mountain of private and public debt BUG has created.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.