“It’ll be gone by June.”

- Variety magazine referring to rock ‘n roll, in 1955

“We don’t like their sound, and guitar music is on the way out.”

- A Decca Records executive on declining to sign the Beatles in 1962

“Reagan doesn’t have the presidential look.”

- A United Artists executive, rejecting Ronald Reagan for the lead role in the 1964 political drama, The Best Man

Don’t sleep on the underdogs. If there’s one dominant message that comes through from this newsletter, it’s my sincere hope it’s the danger of investing alongside the Wall Street consensus. A prime example of the risks of falling for the “wisdom” of the Street was its nearly universal recommendation to overweight emerging stock markets five years ago. This was based on expectations of much faster growth vis a vis the lethargic “rich” countries. Yet, as you can see in the below headline, from yesterday’s front page of the Financial Times, the tables have definitely turned.

![]()

Ironically, as previously observed in past EVAs, emerging nations actually have, until recently, experienced more robust economic results than their lumbering developed country counterparts (think: US, Japan and Europe). Despite this, emerging market shares have been chronic laggards compared to the sloth-like mature economies.

FIGURE 1: FROM STELLAR TO CELLAR--EMERGING STOCK MARKETS VS THE US, JAPAN & EUROPE

Source: Evergreen Gavekal, Bloomberg

In this month’s Guest EVA, I’m turning to one of America’s most storied money management firms, GMO, and its erudite asset allocation chief, Ben Inker, to shed some light on this apparent paradox. While Ben’s essay was written early this year, his essential points are timeless. He hits on one of our core beliefs: Markets (or asset classes) that have been champs over a-three-year period frequently turn into chumps during the next three. On the flip side, the former duds morph into studs. (Similarly, Ben and his team also found that the fasting growing economies over the prior three years tend to lag over the next three, although the tendencies aren’t as powerful as they are with stock prices.)

As he points out, when investors are bullish on the prospects for a country’s—or a region’s—stock market, valuations are generally high. This premium makes it very difficult to continue producing superior returns. Much more likely is a reversion to the mean, or, in English, poor performance that wipes out the previous excess returns.

Ben has found that above-average economic growth often doesn’t translate into faster than normal earnings per share increases, with the latter being a much more important driver of stock prices. (The difference being primarily due to the share issuance/dilution that is often necessary to finance rapid economic development.)

He further discovered that often the catalyst for bull markets is surprising economic growth spurts. In other words, if a country is not expected to do much and it suddenly comes alive, this typically leads to superior stock market gains. Usually, those countries with subdued growth expectations typically have undervalued share prices, a nice launch pad for future outperformance.

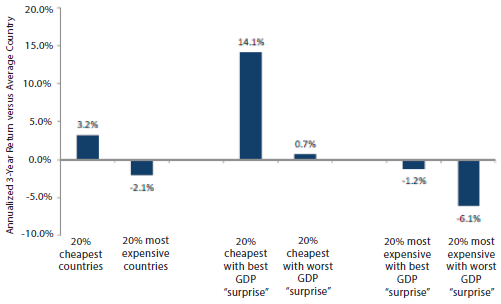

In that regard, here is a key excerpt: “If you can find cheap countries that are going to have a big positive surprise over the next three years, you’ll outperform by a whopping 14.1% for the next three years…if you are unlucky enough to buy the cheap countries with the worst GDP surprise, the outperformance is only 0.7%.” Note, however, that even in the “unlucky” scenario, you still achieve better than average results. The trick is, of course, in predicting positive surprises, which, by definition, are unlikely. But the point is, if a country is predicted to be a tortoise and it turns out to be more like a hare, you can make a lot of money. If you’re wrong, investors still do okay.

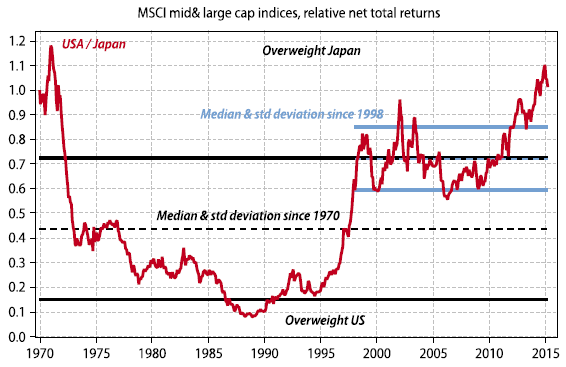

FIGURE 2: RELATIVE PERFORMANCE OF THE US VERSUS JAPAN, IN USD

Source: Gavekal Data/Macrobond

A case in point today is Japan, where the economy is only projected to grow at ½% ad infinitum. This may turn out to be the case but, if so, investors might still make decent money owning Japanese shares due to their massive underperformance versus the US market over the last quarter century. (There’s little doubt that this extraordinary lag was a function of the great expectations for both its economy and its stocks at the end of the 1980s, when the Japanese model was the envy of the world.)

As noted in earlier EVAs, many blue chip Japanese companies are currently trading at 0.2 to 0.3 times sales per share versus an average of 1.7 times for the priced-for-perfection US market. So if you’re interested in following Ben’s advice, the land of the rising sun might just be a diamond in the rough.

For the non-professional investors among you, here’s a little “cheat-sheet” for some of the terms Ben uses:

“Cyclically-adjusted P/E”: Essentially, the Shiller P/E, or the ten year average of inflation-adjusted earnings on a market like the S&P 500.

“Correlations”: A linkage between two or more different securities, asset classes, or markets. A perfect correlation is 1.0.

“Value”: When he refers to value on page 5, he’s referring to value, or contrarian, investing; i.e., buying the lowest priced securities (based on P/E and other metrics).

“Change the sign”: At the bottom of page 5 he uses this to mean that countries with expensive stock markets, based on various valuation measures, underperform even when they produce faster-than-expected economic growth.

DITCH THE GOOD, BUY THE BAD AND THE UGLY

Ben Inker

There has seldom seemed to be a much starker choice facing equity investors than there is today. On the one hand you have U.S. stocks, where profits* have compounded at 11% for the past four years, real GDP has grown at 2.2%, accelerating to an annualized 4.8% over the past six months, and neither inflation nor deflation seems a credible threat. Or you can invest in the eurozone, where profits have compounded at -6% over the last four years in U.S. dollars, real GDP has grown at an annualized 0.3%, “accelerating” to 0.4% over the past six months, and consumer prices have been falling since April–months before oil prices began to fall. Or Japan, where profits have compounded at 6% over the past four years in U.S. dollars, the economy has grown at 0.3% over the same period, falling at a 4.3% annualized rate over the past six months, and a recent burst of inflation associated with a consumption tax hike has brought the level of consumer prices all the way back up to where they were in 1999. Or you could pick emerging markets, where earnings have compounded at 1.3% for the past four years, economic growth is decelerating in fast growers like China and economies are shrinking in commodity producers like Russia, and some combination of inflation (Russia, India, Brazil, Turkey) and deflation (Korea, China) threatens many countries.

And the problems for the non-U.S. options don’t stop there. The new Greek government is heading for a showdown with its paymasters, which may put it on a path to exit the eurozone, and far left and right parties are on the rise in much of Europe, which is not a shock given that the German-inspired austerity path to prosperity seems to be failing. Japan is facing some of the worst demographics in the world, has government debt of over 250% of GDP, and the only obvious cure for its wretched return on capital–investing less–would only worsen its economic plight in the medium term. The problems for the emerging world are truly legion, from an epic credit bubble in China, to an economic crisis in Russia, to the plundering of state-owned enterprises from Argentina to Venezuela. (I wanted to throw in Zimbabwe for a true A to Z listing, but at this point, Zimbabwe would have to crane its neck pretty far to even see its way to being a frontier market, let alone an emerging one.)

Given the backdrop, it is no wonder that the U.S. stock market has been the envy of the world, and with P/Es far from the nosebleed territory of the 2000 bubble, it seems awfully tempting to just follow the advice of the venerable Jack Bogle and avoid non-U.S. stocks entirely.** And yet, as the New Year begins, we in Asset Allocation find ourselves slowly selling down even our beloved U.S. quality stocks in favor of the various problem children of the investing world. We are riding away from the Good and into the arms of the Bad and the Ugly. You might chalk it up to sadomasochist tendencies on our part. However, there is a method to our madness.

The short explanation is that markets don’t work quite the way people assume they do. A slightly longer answer is that things that “everybody knows” are generally priced into markets, despite the fact that most of the time what “everybody knows” turns out to be pretty wrong. If you could accurately forecast the surprises, it would be quite helpful, but in the absence of that ability, buying the cheap countries has generally been the right strategy. And the U.S. is about as far from cheap as any country in the world right now. To use one of the better single valuation measures out there, the cyclically adjusted P/E for the U.S. stock market is 26, versus just under 16 for the U.K. and Europe and a little under 14 for emerging. It will take a lot of good economic news to justify that kind of valuation premium in the medium term.

If You’re Going To Be a Jerk, at Least Be a Contrarian Jerk

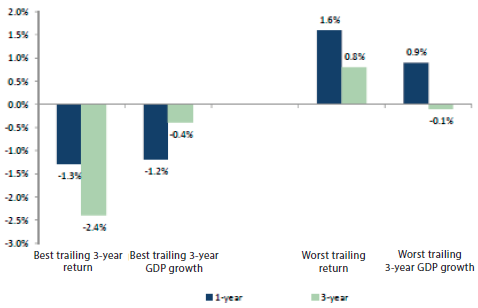

Investors are probably ill-advised to be a knee-jerk anything. It may pain me to say it, but things are always at least a little different this time. We have never seen an economic environment quite like the one the eurozone is facing, with demographic headwinds, a seriously flawed monetary union, high debt loads, and falling household incomes. Certainly Japan is in uncharted territory as well, and if you can find a really good historical comparison for China, Russia, India, or any of the other major emerging markets, you probably are not paying enough attention. On the other hand, history tells us that if you are going to be a knee-jerk anything, at least be a knee-jerk contrarian. The 20% of developed stock markets that outperformed most over a three-year period underperformed on average by 1.3% in the following year and by 2.4% annualized over the next three years. The worst 20% of prior performers outperform by 1.6% and 0.8% annualized.*** The pattern is similar, if weaker, with regard to GDP growth. The fastest GDP growers over the prior three years underperform over the next one and three years by 1.2% and 0.4%, while the worst growers outperform by 0.9% over the next year and marginally underperform by 0.1% over the next three. The performance is summarized in Figure 1.

FIGURE 1: TRAILING GDP GROWTH AND EQUITY RETURNS TO PREDICT FUTURE EQUITY RETURNS (1984-2014)

Source: GMO, MSCI, S&P 500, Datastream

Source: GMO, MSCI, S&P 500, Datastream

But GDP Growth Doesn’t Matter, Right?

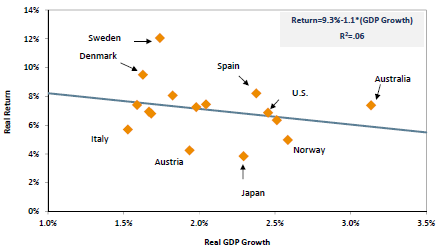

Investing in the best performers over the past few years is clearly a pretty bad idea, as is investing in the fastest GDP growers. This is not because GDP growth doesn’t matter for stock market investors. GDP growth really doesn’t seem to matter for equity investors in the long run, and while that is a topic I covered in “The Death of Equities Has Been Greatly Exaggerated,” it’s worth covering the point again. Investing in a country because you expect it to have strong GDP growth in the long term is a bad idea, and this is true even if your prediction is an accurate one. Figure 2 shows the findings for the developed markets.

FIGURE 2: STOCK MARKET RETURNS AND GDP GROWTH FOR DEVELOPED MARKETS (1980-2010)

Source: MSCI, S&P 500, Datastream

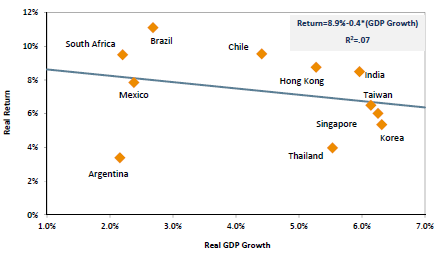

In the 30 years from 1980-2010, the countries that actually had the fastest GDP growth had a slight tendency to underperform those that had the slowest growth. The same pattern held true in the emerging world, as we see in Figure 3.

FIGURE 3: STOCK MARKET RETURNS AND GDP GROWTH FOR EMERGING MARKETS (1980-2010)

Source: MSCI, S&P 500, Datastream

The biggest reason for this non-intuitive result is that the relationship between GDP growth and earnings per share (EPS) growth that most people assume must be there does not exist in the long run. The two developed countries with the strongest EPS growth between 1980 and 2010 were Sweden and Switzerland, which each had lower than average GDP growth. Canada and Australia, which saw the strongest GDP growth, showed very little aggregate EPS growth. Why? A big reason is dilution. Canada and Australia saw strong growth from their commodity producing sectors, but that growth came from massive investment, which was funded by diluting shareholders. Switzerland and Sweden did not invest as much and did not dilute their shareholders, leaving shareholders better off despite lower economic growth.

Where GDP Matters

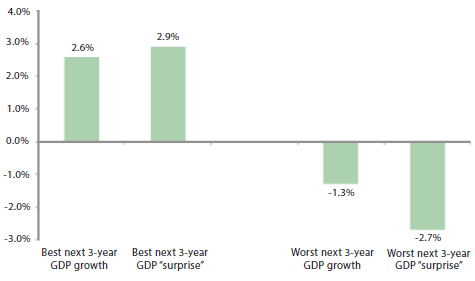

Where all of this gets confusing is that the relationship between earnings per share growth and GDP growth is quite different in the shorter term. If you could accurately predict the next three years of GDP growth, this would be decently helpful for investment purposes as the fastest 20% of growers in the developed world outperform by 2.6% annualized over that three-year period, while the slowest growers underperform by 1.3%. Why does it work in the short term, but not the long term? In the shorter term, GDP growth and earnings are positively correlated. It’s not as strong a relationship as you might think, at 0.32 on average across the developed countries, but it is at least the right sign. In the shorter term, strong GDP growth is associated with cyclical widening of profit margins, whereas long-term growth does not have a similar impact. Where all this gets a bit more confusing is that it almost certainly isn’t GDP growth per se that is most correlated with EPS growth, but GDP growth surprises. Profit margins tend to expand when sales grow faster than what is built into corporate output plans, and they fall when sales growth disappoints relative to plan. Unfortunately we don’t have good history on three-year GDP forecasts across countries, but we can come up with at least a simple proxy of expected GDP growth based on trailing GDP growth and look at the difference between that and actual subsequent growth. The correlation with earnings growth rises from 0.32 to 0.44. The relationship with performance improves as well, with the best 20% of GDP surprise outperforming by 2.9% over the period and the worst 20% underperforming by 2.7%. The data is summarized in Figure 4.

FIGURE 4: FUTURE GDP GROWTH AND GDP "SURPRISE" TO EXPLAIN EQUITY RETURNS (1984-2014)

Source: GMO, MSCI, S&P 500, Datastream

Value Will Out

So investors aren’t crazy to believe that GDP growth in the medium term is related to stock market performance. The problem is that the GDP growth that really matters is almost certainly not the growth that “everybody knows” is going to happen, but the growth that is going to come as a surprise. And predicting surprises is a notoriously tricky problem. Value, on the other hand, only takes information that is freely available to all market participants. It doesn’t take away from the power of being able to predict surprises, but it is clearly the more important factor, as we can see in Figure 5.

FIGURE 5: VALUE AND GDP "SURPRISE" TO PREDICT FUTURE EQUITY RETURNS (1984-2014)

Source: GMO, MSCI, S&P 500, Datastream

Note: "Cheap" and "Expensive" determined by GMO Multi-Factor Valuation Model

If you can find cheap countries that are going to have a big positive GDP surprise over the next three years, you’ll outperform by a whopping 14.1% per year for the next three years, whereas if you are unlucky enough to buy the cheap countries that will have the worst GDP surprise, the outperformance is only 0.7%. Expensive countries with the best GDP surprise only underperform by 1.2%, whereas the expensive countries with the worst GDP surprise lose by 6.1% annualized. GDP surprise certainly matters, but our strongest takeaway at GMO is that even the cheap countries with the worst GDP surprise still outperform, and even the expensive countries with the best GDP surprise still lose. The macroeconomic performance matters, but given how hard it is to predict who is going to do better than expected and the fact that it doesn’t change the sign for either the cheap or expensive countries, we’re sticking with value.

Conclusion

One endlessly confusing fact about stock markets is that even sensible ex-post explanations of outperformance do not imply that forecasting the factors that led to the outperformance is a good idea. It is probably a pretty accurate statement to say that the outperformance of the U.S. stock market over the last few years has been due to the superior economic growth in the U.S. over the period. Forecasters are projecting that superior economic growth to continue into 2015 and beyond. History strongly suggests that investing in the U.S. due to that forecast is a bad idea. Not only are economic forecasts notoriously inaccurate, but the driver of profits and equity returns is really about the macroeconomic surprises, which are almost by definition difficult to forecast. Investing where the valuations are lower has been a far better strategy historically, and, despite all of the worrying features of the economic environment outside of the U.S. today, we believe that investing in the various bad and ugly places in the world is going to wind up far more rewarding than the admittedly good-looking U.S.

* Earnings per share growth: S&P 500 in the case of the U.S., the relevant MSCI index for non-U.S. equities.

** Interview with Bloomberg, “Jack Bogle: I Wouldn’t Risk Investing Outside the U.S.,” December 9, 2014.

*** This and subsequent results are based on the countries that have been in the MSCI World universe continuously from 1984-2014. Returns are for MSCI country

indices in U.S. dollars apart from the U.S., which uses the S&P 500 index.

_______________________________________________________________________________________________________

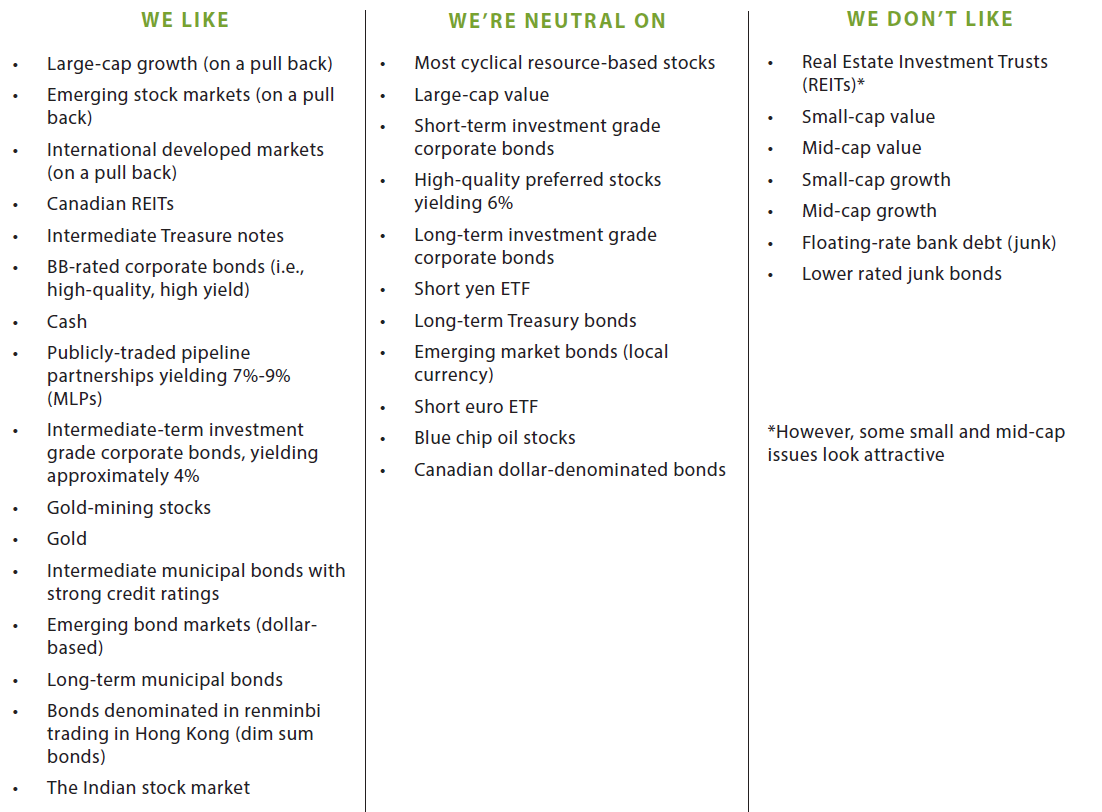

OUR CURRENT LIKES AND DISLIKES

There were no changes this week.

_______________________________________________________________________________________________________

DISCLOSURE: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.