"The mood in the market is better, but the fundamental problems of the euro zone remain unresolved."

- NOUIEL ROUBINI, NYU Professor of Economics (and one of the few academics to warn in advance of the housing bubble's demise).

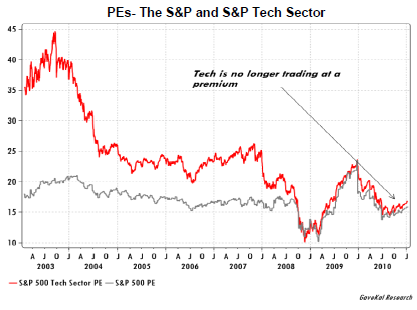

1. The US stock market has witnessed a persistent narrowing of the overall valuation premium by faster growing companies. This phenomenon is evident in the fact that P/E ratios on tech stocks are essentially in line with the general market.

2. Stock market advances that are led by a limited number of issues are usually considered to be vulnerable to a reversal. Last year, 73% of the NASDAQ’s returns and 60% of the S&P’s gains came from just 10% of each index’s constituents.

3. In further confirmation of the tendency of smaller investors to use poor market timing, TrimTabs Research has found that while the S&P 500 has averaged 1171 over the last decade, the average purchase price by those investing in equity mutual funds was 1434.

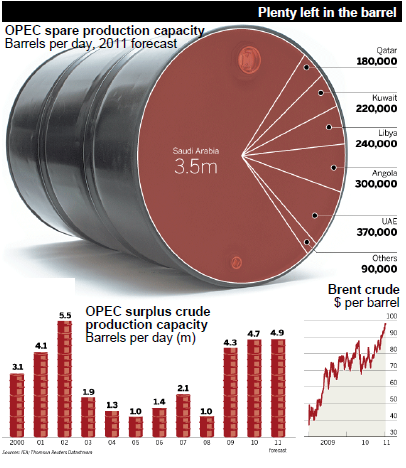

4. Although oil prices are not far from the psychologically crucial $100 level, there is a major difference now versus 2007/2008 when crude first hit, and then vaulted over, the triple-digit mark. Currently, OPEC has nearly five million barrels per day of production capacity.

5. In the 1970s and early 1980s, oil price spikes tended to be inflationary, but since that time they have served to inhibit consumer spending. According to the Wall Street Journal, this may be because wage indexing has largely disappeared. Consequently, when energy costs jump, disposable income is immediately reduced.

6. Recently, there has been a proliferation of new vehicles to invest in oil and gas pipelines, frequently organized as master limited partnerships (MLPs). Given that this group has risen 170% in the last 10 years, versus a down S&P 500, such enthusiasm is understandable. At current elevated prices, though, the optimism may be excessive.

7. Oil is not the only raw material that has gone vertical thanks to the Fed’s government bond-buying binge. The overall commodity index has now exceeded even its speculative top seen in 2008 (just prior to an unprecedented collapse).

8. Chinese authorities continue to be alarmed by rising food prices but asset inflation also remains shockingly high. A square meter of property in China’s leading cities amounts to 164 times per capita income versus a multiple of 33 in Japan.

9. Gold prices have recently weakened, but the long-term uptrend still has some catalysts. Production of the yellow metal peaked a decade ago, while global currency in circulation is up 150%. Additionally, the value of the world’s gold is equal to just 0.6% of the aggregate value of stocks, bonds, and cash versus 3% in 1980.

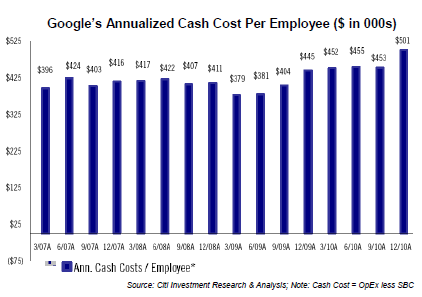

10. Unquestionably, Google has an exceptionally lucrative business model but its prodigious profits may be causing it to lose spending discipline. The internet search giant now incurs a cash cost (i.e., exclusive of stock based compensation) per employee of $500,000.

11. Fears of an escalating European crisis have subsided considerably of late but the Continent continues to face huge challenges such as the need to refinance an unprecedented $750 billion of debt. This massive looming supply, combined with shaky fundamentals, has pushed the yield on Portuguese bonds back up to an unaffordable 7%.

12. Bulls on Japan’s currency were rattled yesterday by news that S&P downgraded its sovereign debt to AA minus from AA citing vertiginous debt levels and the lack of a credible fiscal plan to prevent further deterioration.

13. Inflation anxiety is increasingly evident in the financial press due to the latest vertical move by commodities. While this is a huge problem for many emerging countries, resource costs are a small part of the US CPI, with labor representing around 70%. Given the anemic six-month trend in real wages, it’s hard to envision a domestic inflationary surge.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.