"This environment is one that naturally encourages investors to use borrowed money to increase their exposure to risk…they will ‘ride the market’ until there is an unambiguous signal of a ‘turn’.’"

- Mohamed El-Erian, Pimco’s former CEO

Come on, Dave—pull it together! There’s not much quibbling that Evergreen puts out considerable quantities of information to its clients and even its non-clients. However, it’s probably a legitimate criticism that we don’t always create a coherent mosaic out of all the charts and data, perhaps frequently falling victim to the triumph of information over knowledge.

Accordingly, I do periodically attempt to produce an essay that serves as a synthesis of many of the key ideas and themes we’ve highlighted in recent months. While it’s probably safe to say that few EVA readers doubt our discomfort with current US equity valuations, I’m not sure the rest of our Google Earth-type views of the financial and economic landscapes have been concisely conveyed. In fact, even regarding stocks, we probably haven’t been specific enough.

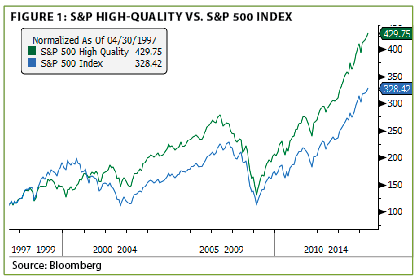

So let’s start with everyone’s favorite topic, especially when it is rising: the US stock market. Some have criticized us for using the "B" word (hint: rhymes with trouble) with regard to current price levels. They correctly point out that there are many reasonably priced issues, particularly, and ironically, among America’s finest companies. At a presentation we did last week, one alert attendee asked me to define what I meant by "high-quality stocks," and it occurred to me that many EVA readers might be wondering the same thing. There are many ways to determine blue chip status, but S&P makes it easier by ranking stocks on a quality basis, with A- to A+ being considered elite status.

As we have repeatedly expressed in past EVAs, the best quality companies have outperformed in the very long run, as you can see below. Moreover, they have done so with less volatility, creating that nearly mythical condition of higher return with less risk. (See Figure 1)

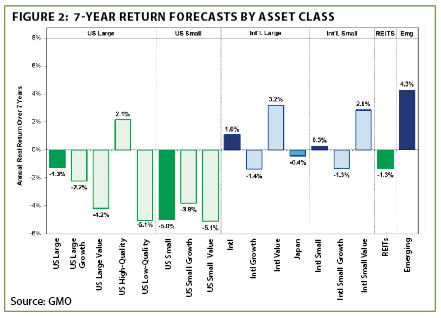

As I remarked at last week’s presentation, this is one of the rare free lunches the financial markets offer (a tip of the hat to Jeremy Grantham on that one). Yet, this is really only the case when high-quality shares are reasonably priced versus the overall market. Fortunately, at least for future relative performance, US high-quality shares are comparatively inexpensive. The reason for the double italics is that blue chip stocks aren’t cheap in absolute terms. This is reflected in the fact that Jeremy Grantham’s firm, GMO, famous for their accurate long-term forecasts, is showing modestly positive, but still below average, multi-year returns for US high-quality shares (note that the returns shown are net of inflation). (See Figure 2)

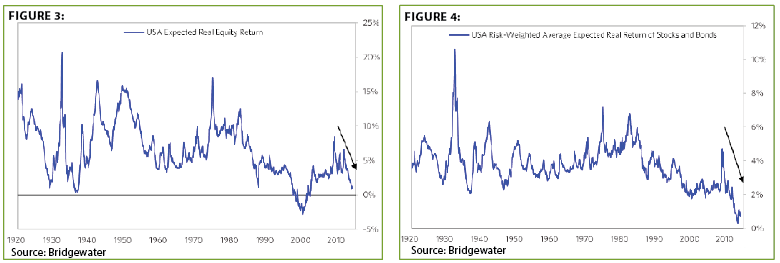

In case you think GMO is too bearish, I recently came across two charts from Bridgewater, Ray Dalio’s uber-successful firm, one of the unusual hedge funds that truly earns their high fees. As you can see below, it’s readily apparent GMO is not flying solo in their low-expectation future outlook. In the Bridgewater view, there has been just one time (the peak of the late ‘90s bubble blow-off) when prospective real returns for stocks were lower based on their methodology. Note that when considering both stocks and bonds, forward-looking real (or after-inflation) returns have never been this low. Now, how often do you hear or see this from your typical rah-rah Wall Street firm? (See Figures 3 and 4)

The reality is almost never—perhaps because they are too busy creating new weapons of mass financial destruction…

Is the new roach motel spelled ETF? You may recall the term "shadow banking system." This amorphous structure became infamous during the financial crisis, and it continues to flourish. Lest you think that the shadow banking system (SBS) is some rarified place where only big institutions transact with each other, please realize that investments as mundane as money market and bond funds are technically part of the SBS. It also includes other seemingly innocuous investment vehicles like ETFs (exchange traded funds).

Until he departed for the safety of academia last month, Jeremy Stein was one of the Fed’s clearest-thinking and most candid senior officials. He noted that a reality of the shadow banking system is that it provides a "liquid claim on illiquid assets." That struck me as one of those simple but incredibly profound assessments of not just the SBS but of the entire edifice of alleged prosperity the Fed has fabricated in recent years.

Similar to Mr. Stein’s views, I believe the "ETFization" of the financial system poses serious systemic risks by providing an illusion of liquidity involving inherently illiquid securities. And, in my view, the poster child for the excesses of this latest Fed-blown bubble is an ETF that goes by the symbol BKLN.

In days gone by, bank loans were strictly an institutional playground. But, as with so many areas of the investment world, ETFs have democratized this area. That sounds like a good thing but is it?

As Jeff Gundlach, the Planet Earth’s second most famous bond investor, has observed, many bank loans don’t settle (i.e. close) for a month. Yet, thanks to the Bank Loan ETF, BKLN, retail investors can access this esoteric niche of the credit markets with just a few keystrokes on the Schwab or TD Ameritrade trading platforms. (In full disclosure, Evergreen has utilized this type of ETF before their popularity soared and underlying loan quality plummeted.)

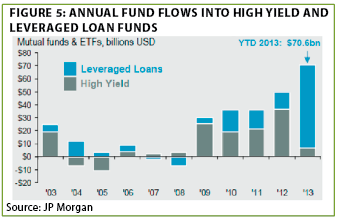

And, as the chart below makes Crater Lake clear, investors have been charging into both low-quality bonds and bank loans with wild abandon. The problem, of course, is what happens when they decide to do the other definition of "abandon," as in head for the hills. (See Figure 5)

If an ETF provides instant liquidity but the underlying security is illiquid, there is, obviously, an inherent contradiction. On the way up, as new money keeps coming in, this creates a pleasant cause/effect condition. In-flows into an illiquid market tend to drive prices up more than if the underlying security was readily available. However, when steady deposits turn into frantic withdrawals, the process plays out in reverse—prices fall much more and much faster than they would normally. This is especially true because, as the old saying goes, market values rise on an escalator and come down on an elevator. Having retail investors heavily involved in a thinly-traded and risky asset class ensures that it will be a high-speed elevator ride down to ground level (and likely far below).

This is a potentiality (in my view, more like a certainty) that goes well beyond bank loans. The entire bond complex is at risk of a panicked-flight scenario. You may have read that the Fed is considering instituting exit fees on bonds funds, presumably including ETFs, due to their angst over this possibility. But the junkiest realms of the credit markets are where the real disaster almost certainly lurks. It has been these most speculative issues that have generated the best performance in recent years, leading to, predictably, the heaviest in-flows from retail investors.

The aforementioned mad-dash into any security with a high yield by definition causes credit spreads, or the yield difference between government bonds and junk debt, to narrow. In the past, I’ve repeatedly highlighted that the Fed’s various QEs failed to lower longer-term government bond yields and the mortgage rates tied to those. Thus, it did whiff on one of its main goals of "large scale asset purchases," which was supposed to aid the housing market and, in turn, the real economy. However, QEs worked wonderfully at crushing credit spreads.

Undoubtedly, this has had some beneficial impact on the actual economy, but collapsing credit spreads have poured rocket fuel into the tanks of the financial markets. This is even the case in Europe, where once-reviled debt issuers like Spain and Italy are able to float 10-year debt at well under 3% (Spanish yields are now the lowest since 1789!). In almost every corner of our world, yield has truly gone missing as investors have bid up bond prices to previously inconceivable levels.

The fly in the ointment, once again, is what happens when credit spreads normalize (if you think these levels are normal, you must also believe in the Easter Bunny, Santa Claus, and that Joan Rivers hates plastic surgery). Jeremy Stein has vocally worried about this, citing his study that a 0.5% widening in credit spreads over a few months clips the real economy by 2% over the next four quarters. You may have noticed that we don’t have an extra 2% of GDP to spare these days.

However, with corporate defaults low and cheap money still omnipresent, it’s reasonable to wonder what might cause spreads to widen. On that score, there’s an old nemesis potentially coming out of a long hibernation.

Going stag? Toward the end of pretty much every economic cycle since the early 1980s, concerns have flared up about "stagflation." In the past, whenever this word has dominated the financial media, I have persistently dissented, most recently in 2007 and 2008. It has been my contention that rising prices, usually in commodities as overutilization of resources occurs late in an up-cycle, was really a case of "lagflation." Once the commodity bubble popped, inflation quickly receded.

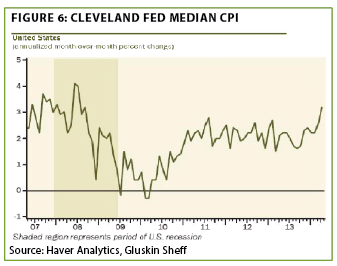

Lately, though, our inflation antenna has been picking up some stronger signals. Many economists believe the Cleveland Fed’s Median CPI, the mid-point between the highest and lowest inflation readings, is more accurate than the Fed’s official measure. Per the chart below, the Cleveland Median CPI has been trading in a fairly tight range for years but has recently broken out on the upside. (See Figure 6)

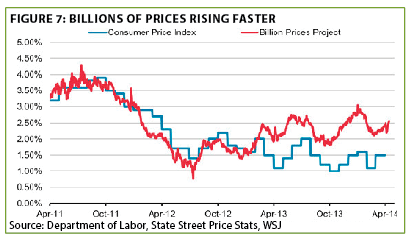

This corresponds with the chart we ran a few weeks ago based on the tracking of on-line transactions by two MIT professors. Since it is so relevant to this topic, I thought I would relay another graphic based on their methodology. (See Figure 7)

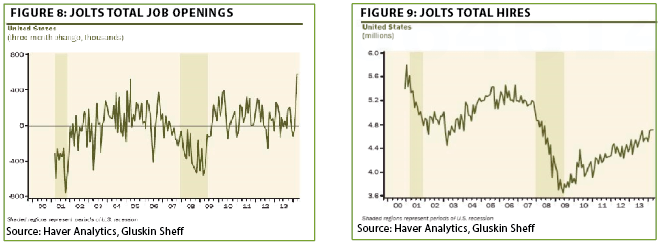

We’ve previously highlighted various charts showing the recent acceleration in bank lending. While we’re not sure whether this has been due to, pardon the pun, weather (the Polar Vortex), as our colleague Will Denyer noted in last week’s EVA, we are becoming convinced the Fed is wrong to believe there is tremendous slack in the labor market.

To our eyes, unemployment conditions are an additional "Tale of Two Markets" phenomenon. Unlike Janet Yellen, Evergreen believes there is a distinct difference between the demand for the long-term unemployed, who tend to be skills-challenged, and those out of work on a short-term basis, the latter generally being the most desirable to employers. This seems to us the only plausible explanation for why there is such a disconnect between the number of job openings, essentially back up to the prior peak, and the still subdued level of new hirings. (See Figures 8 and 9)

This is vitally important because, with Ms. Yellen at the helm, the good ship USS Fed is convinced that they need to try to force the overall unemployment rate down to normal levels using the only tool it has: the printing press. If it is misjudging labor market conditions, then the Fed is running the risk of further encouraging inflating asset bubbles and possibly even creating serious inflation. Wage rates are already rising noticeably for skilled workers.

The Fed needs to come to terms with the reality that a large chunk of the US population is not returning to the work force, whether it is due to demographics (i.e., age) or a growing preference for being on a government support program. (However, it is inaccurate to contend, as many have, that the US has fully recovered the jobs lost during the Great Recession. Due to population growth, the pool of available labor has increased by 15 million, causing the share of the working age populace that is unemployed to soar to a 36-year high, reflecting the aforementioned factors.)

Consequently, should inflation begin to accelerate in earnest, the Fed might have to play from behind and be forced, very much against its habitually stimulative will, to actually start raising rates. And this, in turn, would likely rattle the bond markets, causing credit spreads to widen. After all, few market segments have been more juiced by the Fed’s $3 trillion printing spree than the credit markets, especially those of the dodgier variety.

All right—it’s time to try to create some "closure"…

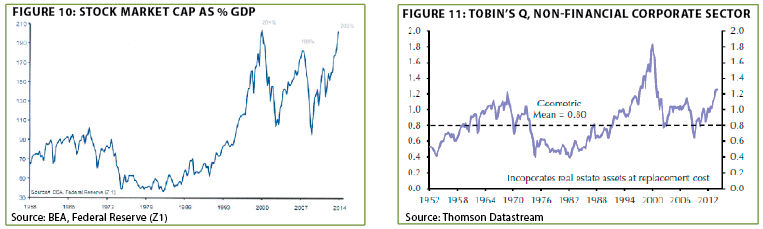

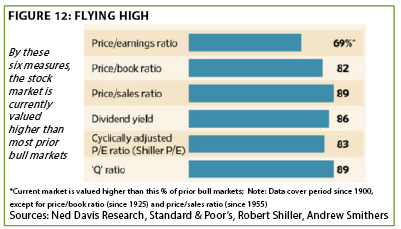

It’s a wrap. Let me conclude this EVA with some quick disabusing of a few stock market-related myths at a 2-minute-drill pace and then I’ll try to tie things together. First, on two of the most reliable long-term measures, market-value-to-GDP and Tobin’s Q Ratio, the stock market is not reasonably priced, as is so often stated in the media. The first is Warren Buffett’s preferred valuation method and the second, comparing the overall market valuation of Corporate America to its replacement value, has had the most accurate forecasting record (tied with our cherished price-to-sales ratio), according to the Wall Street Journal’s Mark Hulbert. As you can see, it takes a very brave, or, perhaps, very biased bull to argue against these facts. (See Figures 10-11 below, and Figure 12)

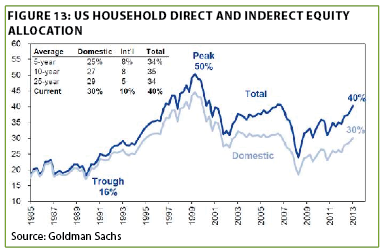

Another outright myth is that American households are low on stocks. While it’s certainly true that stock ownership levels are down from their bubble peaks, they are quite elevated other than when compared to that earlier episode of mass insanity. Further, the graying of America would argue for less stock exposure, at least until the echo baby boomers hit their prime investing years. (See Figure 13)

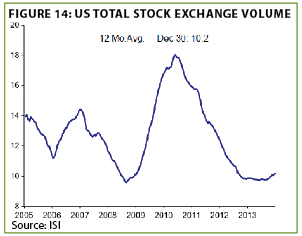

A third blatant myth is that the US equity market is highly liquid. The reality is that, even as this bull has been romping over the last two plus years, volume has plunged. Meanwhile, the share of trading that occurs on traditional exchanges has plummeted from 70% to 40%, with the "shadow trading systems" share surging from under 30% to nearly 60%. This seems like another accident waiting to happen once investors shift into a serious risk-off state of mind, as is certain to happen at some point (perhaps sooner than later). (See Figure 14)

A final stock market myth I’d like to shatter is that low interest rates mean stocks automatically trade at loftier P/E ratios. As one of EVA’s most cerebral readers, Morgan Stanley’s Dan Winckler, points out, this is really only true when real interest rates compress

from high levels. When they fall from a low starting point, as they have lately, it is more reflective of economic stagnation. In reality, ultra-low real rates have been associated with depressed P/Es over time. With inflation rising to around 2% (or 2.5% if you believe the Billion Transaction survey and 3% if you favor the Cleveland Fed’s CPI), and the 10 year-T note yield around 2.6%, the current after-inflation rate is extremely low. (See Figure 15)

So, where does all this leave us? First, we believe the ultimate flash-point for the next bout of turbulence is likely to emanate from the credit markets. We’d suggest watching spreads very closely for a clue as to when this current bout of irrational euphoria begins to morph into just as irrational despair.

Second, though US blue chip stocks are not helium-infused currently, it would be most surprising if they don’t suffer at least some pain when the bubbles in various asset classes pop. But, for those who feel compelled to stay fully invested, or who believe there is a blow-off top coming, they are the place to be in our market.

Third, there’s a good chance inflation may be stirring from its long hibernation. At this point, we suspect it will be a brief awakening. In our view, once the markets break—either due to the Fed surprising with an earlier and more aggressive tightening, or to fears of unchecked inflation, a geopolitical disaster, or some unknownable unknown—worries about deflation will emerge once again. But even a fleeting inflation spike could be the pinprick for the bond market bubble in low-grade credits, rather than rising defaults.

Fourth, this is a pricey stock market, one that seems totally at odds with a world that has mounting risks on multiple fronts (several of the military variety). The power vacuum created by the US becoming more inwardly focused means geopolitical threats need to be factored into the investment process.

The positive news is that pockets of undervaluation are still out there in places where the crowd hasn’t been charging in (gold, Canadian and Hong-Kong issued bonds, as well as emerging market debt). They may not generate eye-popping future gains, but we believe they are comparatively safe harbors.

We are constantly asked how we plan to make livable returns for our clients in the years ahead. As you saw from the Bridgewater chart, it’s not going to happen through a buy-and-hold approach with either stocks or bonds. It’s a hard truth, but the upside just isn’t there. That’s why we aren’t fully invested in either. The only way, in our opinion, to achieve mid- to upper-single digit future returns is to hold a larger than normal amount of cash and also some hedges on the market sectors most vulnerable to a mass exodus. Having these puts us in a position to buy into whatever asset class drops to a point where future returns are at least respectable, as happened with most yield instruments during last year’s "taper tantrum."

Another inescapable reality is that lofty prices by definition lead to lower future returns. There’s a venerable adage in economics that has been proven out time and time again: The cure for high prices is high prices. The same is true in the financial markets.

![]()

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.