"Knowledge is power only if man knows what facts not to bother about."

-Robert Lynd, sociologist

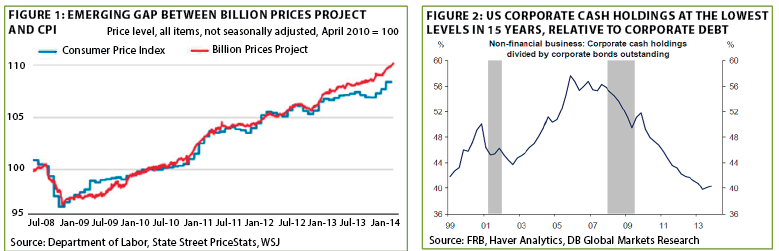

1. For many years, this newsletter has urged its readers to ignore inflation worries. Lately, though, we have begun to see some indications that consumer prices may be heating up. One of the more intriguing is the growing divergence between the official CPI and the “Price Stats Index,” developed by Alberto Carvallo and Roberto Rigobon at MIT, which tracks real-time online transaction data. It is not running 1% higher than the official measure and began to widen over a year ago. (See Figure 1 below, left)

2. Five years ago, when bearishness was pervasive, numerous EVAs referenced Corporate America’s fortress balance sheet as a key reason to be a buyer of blue chip stocks, as well as ultra-depressed yield securities, such as bonds and preferred shares. These days, though, the corporate sector is no longer very fortress-like, with cash relative to bonds outstanding at the lowest level in fifteen years. (See Figure 2 above, right)

3. Current economic trends are presently extremely conflicted, and inflation is no exception. Unit labor costs are the primary driver of consumer prices, and in the last year they have increased by a mere 0.9%, implying there isn’t a major inflation spurt on the immediate horizon.

4. Best-selling author Michael Lewis' new book, Flash Boys, warned about the destabilizing impact of high-frequency trading. There is another development that could also create extreme volatility: The proliferation of Exchange Traded Funds (ETFs). ETFs warrant scrutiny in this regard as they now represent $1.7 trillion of market value versus just $531 billion in 2008. The risk is the ease with which ETFs can be sold, forcing down the prices of the underlying securities, often much less liquid, triggering a pernicious chain reaction effect.

5. Echoing a long-standing EVA theme, the US economy’s lethargic expansion is leading to increased longevity, as recently noted in a Wall Street Journal article titled “Sluggish Recovery Proves Resilient.” Moreover, there are signs economic activity is improving, though the data continues to be mixed enough to support either a positive or negative view, with attitudes shifting on almost a weekly basis.

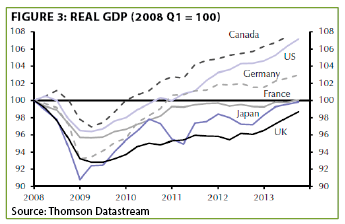

6. Regardless of the confusion caused by the irregular nature of America’s current economic up-cycle, there is no question that it has bested nearly all other heavily-indebted developed countries, most of which have also resorted to profligate fiscal and monetary policies. However, the US has trailed Canada, one of the few rich countries that has avoided the ultra-Keynesian "solutions," perhaps a crucial factor in why its economy has been the star performer. (See Figure 3)

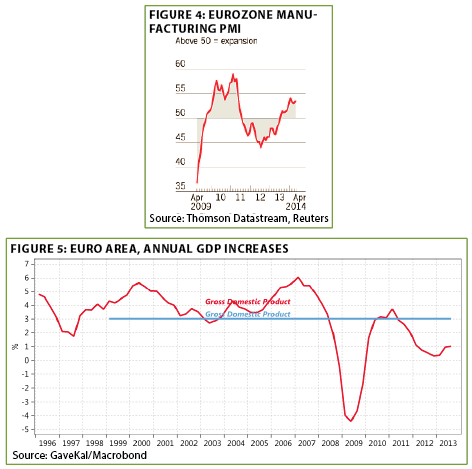

7. Although inflation looks to be troughing and possibly hooking up in the US, the situation in Europe is radically different. Eight eurozone countries are now experiencing deflation, with Sweden coming under withering criticism from hard-core Keynesians, such as The New York Times’ Paul Krugman. Swedish prices fell by 0.4% in March, or nearly 5% annualized.

8. Mere weeks ago, it appeared as though Europe was unquestionably on the mend as its key Purchasing Managers Index (PMI) moved decisively into expansion territory. Suddenly, however, the Continent is once again being bombarded by a plethora of weak economic releases. Given that the eurozone’s nominal GDP (i.e., including inflation) has averaged just 3% since 2000, and is running at just 1% now, this is most unwelcome news. (See Figures 4 and 5)

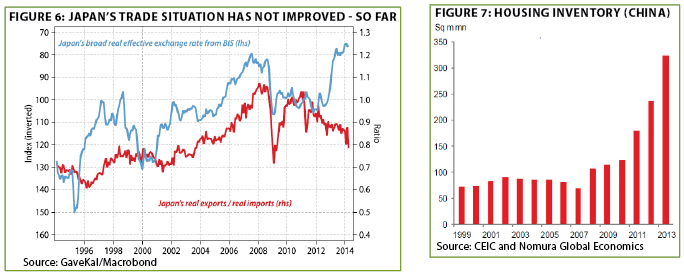

9. It was expected that the yen’s cliff-dive, as intentionally engineered by the Bank of Japan, would jump-start Japanese exports. Thus far, this is not happening. (See Figure 6 below, left)

10. Despite supposedly limitless demand, China’s housing market finally appears to be cracking. Inventories are up 300% in recent years, and prices are now beginning to fall. This is likely to have far reaching consequences, including globally, considering how reliant its economy has been on booming property markets and how much of the world’s growth was made in China. (See Figure 7 above, right)

THE EVERGREEN EXCHANGE

By David Hay, Jeff Eulberg, and Tyler Hay

The most pressing question? Due to the fact that there has been an influx of new EVA recipients recently, I thought it would be helpful to explain a couple of things which are likely familiar to veteran readers. First, this is the time of the year when my team and I converge on the sunny San Diego area to listen to viewpoints from a collection of some of the most acclaimed investors on the planet Earth at the Mauldin/Altegris Strategic Investment Conference (SIC).

This is an event that I have attended for nearly a decade, and it has consistently provided a view of the world often at odds with the outlook of Wall Street firms and most mainstream economists. It’s not being harsh to observe that neither of these more traditional sources of investment "guidance" have distinguished themselves in their ability to anticipate the various calamaties that have hit the economy and financial markets since the new century (and millennium) began.

Yet, that is definitely not the case when it comes to those who have spoken through the years at the SIC. Many of the same luminaries, who predicted the housing and lending bubble of seven years ago, are still featured speakers. It is fascinating to me how their views are now diverging as they consider what the future holds after another period of ultra-low interest rates and the return of "anything goes" lending.

This is also the EVA edition, which we do twice monthly, when we include the analysis of Jeff Eulberg and Tyler Hay, both of whom also attended last week’s SIC. Their assistance in absorbing and processing the tsunami of insights that rolled over us last week was invaluable.

In my case, I went into this year’s SIC in search of "intel" on a topic that I’ve written extensively about in past EVAs, one that I believe may be the most significant for what lies ahead for the financial markets: the velocity of money. Fortunately, there was considerable commentary on this vital issue but, in my opinion, the most definitive was from the intellectually—and verbally—formidable Dr. Lacy Hunt of Hoisington Investment Management. Before I summarize his views on velocity, and those of some of the other presenters, let me provide a brief refresher on what it is and why it is so meaningful.

Velocity, in the monetary sense, refers to how rapidly money circulates in our financial system. (For those technically inclined, it is specifically the total size of the economy, i.e., GDP, divided by the amount of money in circulation.)

The reason that the rate at which money turns over is such a huge issue relates back to the Fed’s hyperkinetic creation of banking reserves in the last five years, the infamous "QEs," now amounting to over $3 trillion. Typically, banks multiply their reserves by almost 10 to 1, using them to generate mortgages, auto financing, business loans, etc. Doing some simple math, this means that there is the potential for close to $30 trillion of new credit extensions thanks to the Fed’s "binge printing."

A full utilization of this staggering sum would almost certainly precipitate an immense surge in demand for goods and services. Of course, it would also mean a veritable explosion in consumer prices, otherwise known as inflation and, nearly instantaneously, interest rates, at least those beyond the Fed’s control. Should velocity start returning to anything close to normal, the Fed would have to do a complete 180 if they want to avoid a return to the inflation-plagued 1970s, or even worse. In other words, they would have to quickly become as aggressively tight as they have been exceptionally easy.

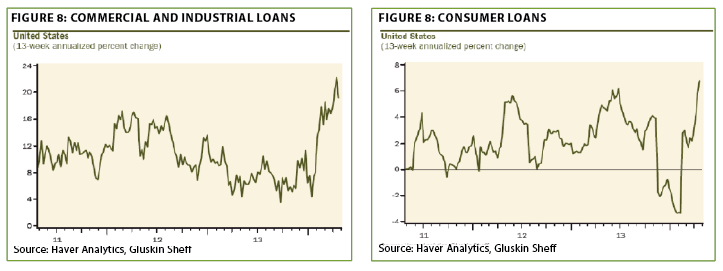

With Evergreen’s considerable exposure to yield-oriented investments, this issue is naturally of paramount concern to us, but we think all investors should be riveted on it as well. Going into the SIC, my team and I were, as conveyed in recent EVAs, on high alert about indications that velocity was coming out of its long bear market. The charts below give you some sense of why our nerves have become increasingly frayed. (See Figures 8 and 9)

David Rosenberg was one of the first speakers at the Mauldin event, and he sits firmly in the acceleration camp, as he displayed various graphics similar to those above. (I should further mention that my partner, Anatole Kaletsky, who also spoke, is largely in agreement with "Rosie.") Considering that for nearly 20 years, David was a bull on bonds, and a pooh-pooher of any inflation revival, his dramatic about-face is definitely noteworthy. But on day two, Lacy Hunt—the epitome of dapper in a white shirt, bow tie, and crisp seersucker suit—launched into one of the most powerful and persuasive counter-arguments I’ve ever witnessed.

First, as conveyed in numerous bygone EVAs, Hunt asserted that QEs 2 and 3 actually raised longer rates. If you’re skeptical, consider that since the "taper" was activated in December, long-dated Treasury yields have been falling, flummoxing almost the entire investment community (but rewarding our numerous against-the-grain purchases of beaten-down yield issues in the second half of last year).

Second, Hunt affirmed my view that the notion of the Great Deleveraging (there are a lot of "Greats" floating around these days) is much more myth than reality. While the US has experienced a minor amount of debt pay-down since 2009, debt levels are now 435% of global GDP versus 403% pre-crisis. Some deleveraging!

Next, he pointed out that once economies hit the 275% debt-to-GDP level (both private and public), growth begins to flatten out. This happened in the US in 1997 and, consequently, our economy’s normal 3% expansion clip has melted to 2% (actually 1.8% since 2000). Japan and Europe hit the 275% threshold much earlier, and have continued piling on IOUs, but they also hit the growth wall much earlier than America did. Ergo, at a certain point, when debt is roughly three times as large as a given economy, growth becomes very difficult. This is despite Al Gore’s invention of the Internet in the 1990s, which arguably rivals the printing press (I don’t think even Al would claim to have created that!) as the ultimate breakthrough technology.

Ok, I’m running out of time and space, so here is a paraphrased CliffNotes version from Hunt on why this happens: Artificially suppressed interest rates hurt savings; with inhibited savings, investment falls; without adequate and intelligent long-term investing, productivity contracts; unjustifiably low interest rates invariably incite borrowings that are used to make bad investments (like buying back stock at inflated prices), causing velocity to fall as these inevitably blow up (think housing bubble and, lately, buying debt from countries and companies that can’t pay it back). Consequently, Hunt believes velocity will continue falling at 3% per year.

So, here’s our bottom line takeaway from SIC: We think the odds favor the deflationary shock view versus those looking for an inflationary boom, at least over the next year or two. We are far from convinced on this, however, and will continue to monitor developments extremely closely. As you will read in Tyler’s section, there are some very bright people who strongly disagree with the Lacy Hunt view.

As they say, that’s what makes a market—and our job interesting in the extreme!

Changing the world, one phone at a time. As a member of the Evergreen investment team, one of the aspects I appreciate most about the Mauldin SIC is the variety of viewpoints expressed. Listening to these, and deeply reflecting on them, helps us avoid the trap of groupthink. At Evergreen, we try to avoid this pitfall by going to this and other similar events, as well as encouraging an open dialogue and imploring the entire team to challenge every opinion.

Just like every other year, I returned from this year’s conference with piles of notes and presentations to comb through. Some of my opinions were reinforced by the powerful presentations, while I’ll need to spend time reviewing others to solidify my viewpoint. The most common theme throughout the presentations, though, probably won’t surprise you. Not because the idea was novel, but because it refers to something currently in your bag or pocket: smartphones and tablets, and more generally, the mobile space.

Mauldin, oft-labeled a perma-bear, shocked the crowd with a rather bullish presentation discussing impressive technological innovations that are on the cusp of changing our lives. Former Speaker of the House, Newt Gingrich, believes we’re just witnessing the start of what these devices are capable of. Neil Howe, a historian, economist, and demographer, believes futures generations will require everything to be connected and will benefit immensely from these devices.

In Mauldin’s presentation, he put up a Radio Shack ad from the early 90s (below, right) in an effort to point out that every one of the devices in it are now in your pocket. The smartphone hasn’t just replaced traditional landline phones. It’s consolidated music players, video and voice recorders, notepads, cameras, and many other gadgets from yesteryear into one mega-device. Beyond being cost- effective, smartphones have changed the way we access news, check the weather, share photos with friends, and even how we consume content.

Newt Gingrich told a story about how smartphones help marriages as well. Recently, Newt was on vacation in France with his wife when they got off course and couldn’t figure out where they were headed. In the past, this would have required driving around lost, arguing with his wife, until finally stopping for directions. Today, all he needed was Google Maps. The hotel address was entered—in relation to their current location—directions were produced, and the problem was solved in a matter of minutes.

The phone in your pocket has the capability to control everything in your living room. At the push of a button, or more likely with a voice command, your phone can set your house alarm, turn on music, turn off the television, take inventory of your refrigerator, and even lock or open your home. Eventually, the phone will replace everything that is in your wallet and will eliminate any need for cash or credit cards. At some point, the phone will become your personal assistant. The software will seamlessly organize your life into one convenient location.

These devices have made us extremely efficient, but can they be more? Mauldin and Gingrich both mentioned the impressive potential from a health perspective. Gingrich believes we are close to a time when heart patients can be constantly monitored via their phone. And, the devices will have the capability to alert the patient’s doctor if vitals drop to harmful levels. In a similar vein, Mauldin thinks we could be close to having infants monitored and parental warnings issued should anything concerning happen late at night. Health care researchers love data, and the smarthphone appears to be the Holy Grail they’ve been waiting for to assist in tackling many of their industry’s greatest challenges.

Immense knowledge is now in the palm of our hands. We can use these devices to quickly settle debates or research new topics of interest. This pocket-size knowledge portal is also helping brilliant minds develop in the emerging world, which wouldn’t have been possible pre-smartphone. Who knows, the next Steve Jobs may currently be roaming the streets of Mumbai looking for a way to satisfy his hunger for knowledge. As of 2013, India has 67 million smart phones subscribers, currently only 6% of the overall India phone market. However, subscriptions are growing by a staggering rate of more than 50% per year. Before we know it, everyone will have the same access to information.

Through the Khan Academy application, or other learning resources, students can now access immediate lessons in subjects in which they’re struggling. Teachers are available to people 24 hours a day. Students no longer have to go to their parents for help with their geometry homework. Thanks to this revolutionary technology, they can now get help from someone who actually knows what they’re talking about (sorry, mom and dad).

Mobile wireless devices will be the platform on which many businesses of the future will be created. The development of the Internet allowed for the birth of Google and many other Fortune 500 companies. Mobile wireless will help create the next Google, and has the potential to create so much more. It’s my bet that the first trillion-dollar company (as determined by market capitalization) will come from the mobile wireless industry. I believe it will be Apple, but I wouldn’t be shocked if Google, Microsoft, or another competitor emerges.

Silicon Valley is still the breeding ground for innovation. The world’s greatest entrepreneurs flock to Northern California to work with like-minded and talented individuals. We need to encourage US companies to invest in research and development to cultivate the game-changing technology of tomorrow. And, we must stop pushing these firms to buy back shares of stock with excess cash when the value of life-enhancing technology is so immense. The applications that we will use in the future will grow to much more than a photo sharing app or an instant messaging service. If in just a few years of developing apps we’ve come this far, imagine where we’ll be in twenty years. These devices will continue to make us more efficient, more secure, smarter, and they’ll even help us live longer lives. The Internet was a quantum leap towards the Jetsons-like lifestyle, and mobile wireless will take us where no man—or woman--has gone before.

Minority (not majority) rules. Let me admit right up front, even if Dave and Jeff won’t, one of my primary reasons for going to San Diego isn’t just for the brilliance of the speakers—it’s also for the illumination that comes from that object we so rarely see in Seattle called the sun. So, during short breaks in the SIC action, when my mind begins to ache from information-overload, I often hustle outside for some "Vitamin D."

In 2011, the conference was held in La Jolla—an affluent suburb of San Diego. One day I went outside for sunshine and fresh air between speakers. I was looking forward to hearing the next speaker, the legendary Paul McCulley, former managing director of Pimco. He’s considered a gifted financial mind and unmatched orator. As I sat soaking in some sun, a homeless man (not a common occurrence in La Jolla) came slowly headed in my direction. He had a long, shaggy beard and hair that hadn’t been cut since the pre-Internet days. His clothes were a mismatched assembly of tattered pants and a bizarre checkered suit coat. He was smoking the stub end of a Marlboro Red cigarette and mumbling to himself. If I hadn’t known The Dude from The Big Lebowski to be a fictional movie character, I would have thought it was he in the flesh. Careful not to make eye contact with the disoriented man, I strategically maneuvered out of his path and returned inside. When I got back to my seat, something strange happened: The homeless man appeared on stage. Even more bizarre, he started talking to the audience and was opining (more like yelling) about financial matters. The homeless man was Paul McCulley! (I promise this story has relevance to investing!)

At this year’s conference, McCulley was there again. In fact, he’s been there every year for the last ten years. This time, his appearance was different. He looked like he had been the lucky recipient of one of Oprah’s transforming makeovers. His noticeably shorter silver hair was sleekly combed back, and his beard was gone. He wore scholarly looking glasses and was in a black suit. His speech was brilliantly communicated. His combination of inflection, southern drawl, and sharp financial acumen was like Doc Holliday meets modern economics. It reflected the same tenets he’s been defending and promoting as long as I’ve been listening. McCulley is an unwavering, uncompromising, unapologetic Keynesian. He’s made no secret of his desires to join the Fed, and his public support of past policies have likely made him a very viable candidate.

McCulley has called Ben Bernanke courageous in his actions during and since the crisis. He rejects the notion that a ballooning debt burden can lead to a disastrous outcome when the debt is owed domestically. This is a fancy way of saying that the US can simply print more money to meet our debt obligations because lenders were stupid kind enough to extend us credit in dollars—a currency we could produce at will. If General Electric issues more bonds than it can payback, they default. If America issues too much debt, the Fed can simply print money. While McCulley acknowledges this can eventually lead to a diluted currency (aka, inflation), he insists the associated impacts are not on the scale with the crisis we saw in 2008. Lastly, he thinks it’s time for the top 1% of earners to pay their fair share. (Don’t shoot the messenger!)

Interestingly, out of the twenty-two presenters who spoke at the conference, McCulley and his fellow Keynesians were in the minority. During a four-person panel, Lacy Hunt, Dylan Grice, and Newt Ginrich pounded on McCulley. The erudite Lacy Hunt was quoting Adam Smith’s timeless study of economics to McCulley. Grice was tactfully conveying the need for sound central bank policy-making. Newt Gingrich was recounting past civilizations’ failed experiments with currency debasement. The degrees of validity contained in their arguments were irrelevant. The soundness of their logic or the historical precedents they put forward went ignored. For those of you who feel like McCulley is minimizing the economic consequences, I do not have the most comforting news: McCulley and people who share his monetary policies are in power. They are in control at the Federal Reserve Bank and their way of thinking is prevalent throughout Washington D.C. If you think this is a Democrat versus Republican issue, it is most certainly not. When Gingrich was asked if the fears held by those (like Hunt) who oppose active monetary policies (like QE) were being discussed in Washington circles, he delivered some frightening news. The former Speaker of the House said that anyone, Republican or Democrat, who would be so bold as to bring up controlling, limiting, or abolishing the Fed, would be viewed as "cuckoo." This means we are stuck with the policies of McCulley, Yellen, Krugman, et al, for better or for worse, until the next crisis. Basically, get use to playing by their rules.

As I said earlier, there is a widely-accepted belief that the Fed’s policies have worked. Our economy is healing after the most serious crisis we’ve had in eighty years. Unemployment has crept lower, and the stock market has come roaring back. Say what you want, given the hand it was dealt, the average American finds the Fed’s work at least respectable. Why shouldn’t they? So far, all those who warn of the consequences associated with "QE Infinity" still haven’t been proven right (sorry, Dave). Inflation is a no-show and now the Fed is in the process of a measured taper, which will theoretically allow the economy to continue its recovery.

Despite their "successes," there is one thing the Fed and others in Washington are not happy about: The widening wealth gap. When talking on this topic, McCulley said, "We will rejigger the distribution of our income so that everyone in this room will assume a great deal of responsibility…." Now, it’s possible that he thinks this alone, and the others at the Fed do not share these views, but I doubt that very much. Janet Yellen has never had a private sector job and doesn’t measure success in profits. She is an academic. Her legacy and the economy’s performance under her direction are what drive her above all else. So far, it’s not a secret that those who’ve owned assets (stocks, real estate, bonds, etc.) have recovered much better than those who didn’t. Incomes have not improved much for the poor or middle class, which is why legislative efforts like raising the minimum wage are gaining steam in Washington D.C. and numerous other states.

McCulley, Yellen, Krugman, and others believe our society is, in the former’s words, "Ripe for a conversation about social justice." Investors should brace themselves for what’s ahead. To me, what comes next is rather straight forward. Emboldened by their recent navigation post 2008-2009, we are going to follow an activist Fed policy until something goes wrong. I do not believe that, should the stock market go down 20%, it would be destabilizing enough to alter the Fed’s current policies. It takes a crisis. In many ways I believe the Fed sees the stock market’s out-of-sync recovery compared to Main Street’s (i.e, far stronger) as an aberration it would like to correct.

Let me conclude with an analogy that I wish I had thought up on my own. Jeffrey Gundlach, the incomprehensibly smart and unofficial new "King of bonds," rejects the notion we are taking our economy in the right direction. He thinks what we’re doing is like someone who jumps out of an eighty-story building, and after passing the fortieth floor says, "So far so good." While he may be right that a fatal ending lies ahead, there is no end in sight for current Fed policies. In many ways, it was the financial crisis of 2008-2009, that reshuffled economic leadership, and it will likely take another crisis before those ideologies soften or get diluted. I’ve

never been a strong believer in buy-and-hold investing. The markets, after all, have these imperfect, irrational participants called humans, who are "regulated" by human officials. If you think we as humans are always rational, I applaud your belief in people (and can simultaneously confirm that you’ve never been married). People do, however, persevere and we’ve always done our best for clients and their portfolios during times of crisis. We don’t expect either of these things to change in the future.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.