“Roughly speaking, losses hurt about twice as much as gains make you feel good.”

–RICHARD H. THALER, author of Misbehaving: The Making of Behavioral Economics

In his popular book, Misbehaving: The Making of Behavioral Economics, Richard Thaler suggests that, “Many people have made money selling magic potions and Ponzi schemes, but few have gotten rich selling the advice, ‘Don’t buy that stuff’.” In fact, it can be downright unpopular to be the adult in the room when easy money seems to be falling from the skies like raindrops in Seattle in January.

Similarly, when investors are in a semi-suicidal communal mood, it is equally infuriating to hear those lonely voices saying: “Do buy that stuff.” A classic case of this was in March of 2009, during the most panic-stricken days of the global financial crisis (GFC), when money management legend Jeremy Grantham did exactly that by publishing a bullish essay called: “Reinvesting When Terrified”. At the time, it was not what most investors, who were tightly curled up into the fetal position, wanted to hear.

Vindicating Mr. Grantham’s courage and foresight, in the wake of what was the most abysmal market thrashing since the 1920s, the phoenix that rose from the ashes in 2009 set historic levels earlier this month, as America’s blue-chip index – the S&P 500 - crossed the 3,000-point level for the first time ever.

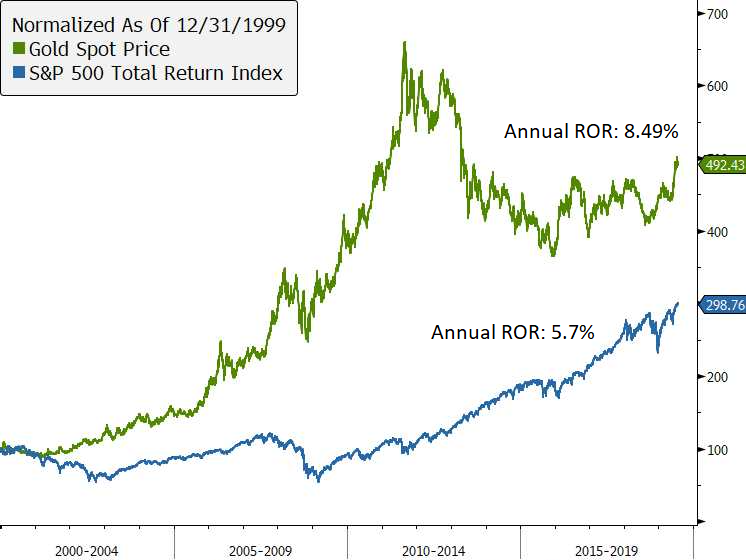

For anyone out there keeping track, prior to the GFC the previous all-time highwater mark for the S&P was just above 1,500. In other words, the S&P 500 has now essentially doubled from its pre-crash peak. From the time when Mr. Grantham penned his now semi-mythic piece, a bit over a decade ago, the main US benchmark has quadrupled. Now, with US stock prices at inflated levels based on a long list of yardsticks, it’s worth asking: what in the world is going to be a winning strategy over the next ten years? Hint: if history is any guide, it’s not what has been the star of the past decade.

This week, we are presenting a guest newsletter from our widely admired friend Mike O’Rourke. For those who don’t know, Mike is JonesTrading’s Chief Investment Strategist and author of The Closing Print, a daily newsletter that sums up noteworthy happenings in the investment world. In this missive, Mike relays the sage advice of another legendary investor, and self-made billionaire, Ray Dalio, who is addressing the urgent question asked above.

As you will read, Mr. Dalio is advocating the avoidance of what is basically rear-view mirror investing, a curse that afflicts even professional investors, particularly after such a long-lasting bull market. Along those contrarian lines, he suggests that given historically elevated asset prices, increasingly high leverage, and monetary policy which is slowly but surely devaluing the greenback, a shimmering precious metal might be a good bet in the years ahead. In case you don’t know it, and we suspect many don’t, the “barbarous relic”, as it is often derisively known, has performed admirably over the last almost 20 years, going back to the first time the S&P 500 first kissed 1500.

Source: Bloomberg, Evergreen Gavekal

Source: Bloomberg, Evergreen Gavekal

Yet, over the last 10 years, it’s been anything but glittering, until very recently, leading millions to ignore—or, even, detest—it. Ironically, that’s precisely the attitude Mr. Dalio is warning investors to guard against.

For those interested, we wrote briefly on the subject in February 2018, in a newsletter titled “Going for Gold.”

THE INSTANT CLASSIC

By Mike O'Rourke

In his 19th century book “Fifty Years in Wall Street,” Henry Clews imparted remarkable wisdom. According to Clews, “Few gain sufficient experience in Wall Street to command success until they reach that period of life in which they have one foot in the grave.” The statement speaks to the long cycles that occur within markets and economies. Thus, it is not often in one’s career that you come across a timely note that marks a seminal moment in markets. Until today, the only note we would place in that category is Jeremy Grantham’s “Reinvesting When Terrified.” It was the type of note that spoke with clarity of mission and purpose, urging investors to avoid psychological pitfalls when an inflection point was lurking but still impossible to pinpoint. Grantham was remarkable in observing that “Every decline will enhance the beauty of cash until, as some of us experienced in 1974, ‘terminal paralysis’ sets in. Those who were over-invested will be catatonic and just sit and pray. Those few who look brilliant, oozing cash, will not want to easily give up their brilliance. So almost everyone is watching and waiting with their inertia beginning to set like concrete. Typically, those with a lot of cash will miss a very large chunk of the market recovery.” That note was published in March of 2009, and history was made.

The key to such a note is that the arguments are extremely lucid. If one can abandon their biases and the emotional noise of the market, the argument being made is undeniable. Ray Dalio’s note titled “Paradigm Shifts” also fits into this category. Dalio was certain to include the historical background along with the facts in his 13-page missive. The note is littered with investment wisdom only gleaned through decades of experience as Henry Clews explained. Other bits of wisdom directly relate to the current environment. As he introduces his view, Dalio notes “...most people adapt to and eventually extrapolate so they become overdone, which leads to shifts to new paradigms in which the markets operate more opposite than similar to how they operated during the prior paradigm.” That view of market activity is very much aligned with George Soros’ “Theory of Reflexivity.” Dalio’s sage advice does not end there. Dalio continued, "… I can say with confidence that throughout the times I have studied the same big things happen over and over again for essentially the same reasons. I’m not saying they’re exactly the same or that important changes haven’t occurred, because they certainly have (e.g., how central banks have come and gone and changed). What I am saying is that big paradigm shifts have always happened and they happened for roughly the same reasons.” That prompted thoughts of legendary Merrill Lynch Strategist Bob Farrell’s line “History does not repeat itself exactly, but behavior does.”

Although it is hard to do justice to “Paradigm Shifts” in such a short format, we will try. Dalio notes that over the last century, paradigm shifts have largely come with the changing of the decade and each paradigm had its own personality, but there were multiyear counter-trend moves within each paradigm. He noted that in those phases, “The worst thing would have been to go with the moves (sell after price declines and buy after price increases).” The paradigm then continues. “They go on long enough for people to believe that they will never end even though they obviously must end.” The extrapolating influences positioning. “I have found that the consensus view is typically more heavily influenced by what has happened relatively recently (i.e., over the past few years) than it is by what is most likely.” Then the shift occurs. “In paradigm shifts, most people get caught overextended doing something overly popular and get really hurt.” Dalio reminds readers never to be complacent and think you are safe. “That is because any single approach to investing—e.g., investing in any asset class, investing via any investment style (such as value, growth, distressed), investing in anything—will experience a time when it performs so terribly that it can ruin you.” Furthermore, “Every major asset class had great and terrible decades, so much so that any investor who had most of their wealth concentrated in any one investment would have lost almost all of it at one time or another.”

Dalio then explains the current environment. “Now, asset prices are relatively high, growth is priced to remain moderately strong, and inflation is priced to remain low.” He further adds “Central banks have been lowering interest rates and doing quantitative easing (i.e., printing money and buying financial assets) in ways that are unsustainable… That bolstered asset prices both directly (from the actual buying of the assets) and indirectly (because the lowering of interest rates both raised P/Es and led to debt-financed stock buybacks and acquisitions, and levered up the buying of private equity and real estate) … That form of easing is approaching its limits because interest rates can’t be lowered much more and quantitative easing is having diminishing effects on the economy and the markets as the money that is being pumped in is increasingly being stuck in the hands of investors who buy other investments with it, which drives up asset prices and drives down their future nominal and real returns and their returns relative to cash (i.e., their risk premiums).”

In explaining the coming paradigm shift, Dalio offers the caveat that he is unsure on timing, but highlights what to watch for. First, “central banks will run out of stimulant to boost the markets and the economy when the economy is weak.” Second, “there will be an enormous amount of debt and non-debt liabilities (e.g., pension and healthcare) that will increasingly be coming due and won’t be able to be funded with assets.” In game planning the anticipated policy response to such an environment, Dalio states “By looking at who has what assets and liabilities, asking yourself who the central bank needs to help most, and figuring out what they are most likely to do given the tools they have at their disposal, you can get at the most likely monetary policy shifts, which are the main drivers of paradigm shifts.” In the situation that is unfolding, he notes it is the debtors relative to the creditors. He believes the tools that will be left will be “monetizations of debt and currency depreciations.” Therefore, he warns against the conventional wisdom of today and recommends increasing exposure to assets that post good returns when money is devalued, like gold. Dalio specifically explains, “Most people now believe the best “risky investments” will continue to be equity and equity-like investments, such as leveraged private equity, leveraged real estate, and venture capital, and this is especially true when central banks are reflating. As a result, the world is leveraged long, holding assets that have low real and nominal expected returns that are also providing historically low returns relative to cash returns. I think these are unlikely to be good real returning investments and that those that will most likely do best will be those that do well when the value of money is being depreciated and domestic and international conflicts are significant, such as gold.”

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.