“The mind is like a parachute. It doesn’t work unless it’s open.”

- Frank Zappa

_____________________________________________________________________________________________________

As is the case with Evergreen, our partner firm Gavekal encourages an environment of “opinion exchanges”. In the latter case, much of that stems from the inherent philosophical divergences regarding economics and politics between its three co-founders.

Louis and Charles Gave definitely lean more toward the Austrian school of economics. This holds as sacrosanct such factors as sound money policies, moderate regulations, controlled government spending and deficits, and the desirability of allowing markets to freely set prices. To Americans, this would be akin to the supply-side economics paradigm that largely dominated during the 1980s and 1990s but has been in a long eclipse since then.

On the other hand, Anatole Kaletsky, the kal in Gavekal, is a self-avowed Keynesian. While Louis and Charles have been largely appalled by the various extreme monetary measures Western central banks have resorted to over the last dozen years, Anatole has maintained a consistently sunny view of these efforts. And he’s been consistently right—at least as far as financial market performance in the US has been concerned. In other markets, and also in America’s real economy (i.e. Main Street vs Wall Street), the positive consequences of radical monetary policies have been far less discernable.

With many, including this author, believing that the 2020s might turn out similar to the 1970s, in this week’s Gavekal EVA Anatole is making a case that it’s more likely to be a replay of the 1950s. In other words, a decade of low inflation, strong growth and shared prosperity, with Keynesian economic theory once more being the saving grace. (Ironically, it was the 1970s stagflation that was the downfall of the unquestioned supremacy of Keynesianism and, today, as you’ve no doubt read and heard, stagflation fears have become widespread.)

Interestingly, Anatole doesn’t address the fact (at least it’s a fact in my mind) that the US and most other “rich” economies, have moved beyond Lord Keynes’ model of running deficits during recessions, but generating surpluses in good times, and into the brave new world of Modern Monetary Theory (MMT). MMT allows for a level of deficit spending, largely funded by central bank fabricated “money”, that would undoubtedly shock and dismay Lord Keynes himself were he still on this side of the grass. In my view, MMT is to Keynesianism what communism is to socialism--the former being much more radical and dangerous versions of a kindred paradigm.

The US was effectively already employing MMT under Donald Trump, even before the virus crisis. Since the pandemic struck, we’ve gone all-in with MMT as the US government has spent $1.2 billion every hour and $19.3 trillion in total from the end of 2019 until now. This resulted in roughly $6 trillion in federal red ink which the Federal Reserve has largely bought with money it has simply created from its magical computers. That is a radically different scenario than what we saw in the mostly Eisenhower governed years of the 1950s. It’s also even more inflationary than anything the Fed did in the 1970s when it fell woefully behind the inflation curve (though not as dramatically as it has since Covid went viral).

Regardless of this omission, it’s always worthwhile to consider optimistic outlooks. This is particularly reasonable when the consensus has moved from inflation/stagflation complacency, at the start of this year, into a state of high-anxiety over these often joined-at-the-hip economic scourges. In other words, perhaps the belief in an inflation breakout has become a too-popular narrative and, consequently, Anatole’s sanguine viewpoint is poised to shift back to mainstream, as it was just a few months ago. That’s certainly possible in my view, but, if so, I’d expect it to be, using one of Jay Powell’s favorite words, transitory.

In the early 1950s, Mad magazine adopted the motto “What—me worry?” as its catchphrase, next to the grinning face of its idiot mascot Alfred E. Neuman, and then promoted Neuman as a write-in candidate for US president in 1956. Since I believe that the world economy now faces conditions more akin to the 1950s than any other decade (and since I am just old enough to recall Mad’s heyday in the early 1960s), let me apply Neuman’s slogan to the worries that have suddenly gripped many investors and market economists, which seem to me way overdone.

These worries were neatly summarized by Bloomberg News last Friday, just before the shakeout in equities on Monday this week: “The global economy is entering the final quarter of 2021 with a mounting number of headwinds threatening to slow the recovery from the pandemic recession and prove policymakers’ benign views on inflation wrong.” Bloomberg then usefully enumerated 10 worries:

Faced with this catalogue of woes, the stock market setbacks since early September are hardly surprising. The real surprise is surely that the closing lows of the S&P 500 and the MSCI World Index on Monday were both just -5% below their September all-time highs. The standard interpretation of these very modest corrections is that the worst is still to come because investors are still complacently ignoring all the risks that are staring them in the face. This is quite possible, and nobody can rule out some further steep declines in the days ahead. But another view is at least equally plausible. It may be that the worries listed above are either a) already discounted, b) exaggerated, c) transient or d) irrelevant to equity prices. I believe that seven of the 10 problems listed by Bloomberg can be dismissed under one of these four headings:

Discounted

Worry #1. The delta variant of the virus has already weakened economic activity, especially in the US, but also in China and other countries trying to enforce zero-Covid policies. Growth expectations have been reduced so drastically since they overshot so much on the upside in the first quarter that they now are overshooting on the downside.

Worry #4. China Evergrande Group will doubtless default on some of its debts and its equity will probably be wiped out altogether, but the Chinese authorities have made clear that they will protect their banking sector and will limit contagion to other property developers. Further shocks are therefore unlikely. Instead, dismantling Evergrande would probably trigger a relief rally.

Exaggerated

Worry #2. A US debt default would certainly be disastrous, but this is not a serious risk despite all the posturing in Washington. The Democrats are willing to use reconciliation and take full responsibility for raising the debt limit if all other options are exhausted. And a reconciliation vote could also resolve the budget impasse by combining the debt limit increase with an agreement on roughly US$2trn of “human infrastructure” spending, splitting the difference between the US$3.5trn demanded by “progressives” and the US$1.5trn wanted by the “moderates”. Once this vote happens, probably in mid-October, a powerful relief rally is very likely.

Transient

Worry #6, fuel and food inflation, #7, supply-chain bottlenecks and #8, labor shortages are mainly symptoms of the same underlying problem: the unprecedented tug-of-war between the biggest demand surge since World War II, caused by post-Covid reopening, and the biggest supply collapse the world has ever seen, caused by Covid lockdowns. Both these events have been far outside the range of previous experience, and therefore impossible to capture in economic models providing inflation forecasts, or in financial models supposedly linking inflation with asset prices. All of these models are based on historic correlations and statistical regressions—and all these calculations are invalid when dealing with events far beyond the limits of historical data sets. Logically, there is no convincing reason to believe that goods, services, commodities and factors of production, that were persistently in excess supply until 2019, suddenly and permanently disappeared from the world economy in 2020-21.

Nobody can predict with confidence when supply and demand will come back into balance, but historical experience and economic theory, going back to Adam Smith, show that market mechanisms are remarkably effective in bringing supply and demand for most products into balance and that overshooting prices caused by shortages are followed fairly quickly by undershooting prices amid excess supply. The exceptions to this general rule are labor and energy, and they are the only plausible sources of generalized inflation, as opposed to relative price swings—of which more below.

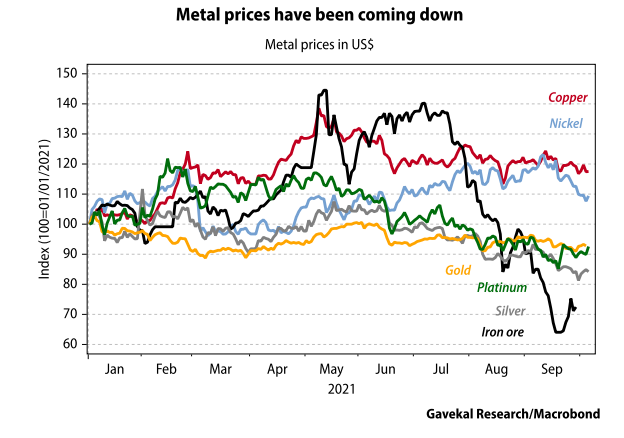

Apart from these two key markets, which are influenced by macroeconomics and geopolitics rather than the laws of supply and demand, most other products are likely to come into balance in the coming months, although the timing is bound to vary between different products, ranging from cotton and pork bellies to semiconductors and cars. The recent price declines in many commodities, including iron ore, copper, nickel, silver, platinum, palladium and gold, suggest that market mechanisms have not been permanently paralyzed by Covid. If anything, market forces in industrial commodities seem to be acting faster than many analysts realize.

Irrelevant

Worry #10. Central bank tightening fears have probably been the strongest bearish influence on investor sentiment since stock markets peaked in early September. But the Federal Reserve’s tapering plans are almost irrelevant to equity prices. What matters for equity valuations is the level of policy rates and the shape of the yield curve. If the Fed sticks to its plan to keep policy rates near zero until 2023—or even if it hikes the Fed funds rate by 25bp before then—the yield curve is unlikely to steepen sufficiently to push 10- year bonds rates above 2%, for reasons that I have discussed repeatedly throughout this year. And if bond yields remain below 2% (or, better still, stay in the range of 1.25-1.75% established this year), equity prices will remain quite reasonable, even for US Big Tech stocks, while valuations in many non-US markets will be screaming “buys”.

Genuine worries

The process of elimination above leaves three genuine worries for investors in risk assets: #3, Chinese regulation; #5, energy shortages; and #9, the long[1]term stagflation threat. Others at Gavekal have debated China and energy at length, and I have only one observation to add: the upsurge in global energy prices is also mainly a consequence of US and European political blunders, not of energy economics or under-investment. If president Joe Biden carried out his promise to lift sanctions on Iran, eased his confrontation with Russia and abandoned the US policy of turning Venezuela into another Cuba, the global oil shortage would quickly reverse. Even more importantly, the Opec monopoly recreated by Russia’s alliance with Saudi Arabia would break down, as it did from 2009 to 2019. Meanwhile in Europe, if the German government and the European Commission agreed immediately to let Russia open the Nord Stream 2 pipeline, the gas shortages in Europe would quickly disappear.

Thus, western politicians have a simple choice with regard to energy prices and fuel shortages: do they give priority to economic growth and price stability in their own countries, or to energy sanctions and other futile gestures which have almost always proved ineffective in achieving geopolitical objectives or changing the behavior of hostile regimes? That is the most important question that energy analysts should be asking. The present panic over gas prices in Europe may create conditions for European Union politicians, at least, to make the rational choice.

I also believe that Chinese internet regulation is mainly a response to US technology sanctions that are forcing China to redirect its investment and engineering talent from software to hardware, as eloquently explained by Dan Wang. This redirection of Chinese resources will erode, and ultimately eliminate, America’s main technological advantage over China. In other words, US gesture politics is heading for another self-inflicted defeat. When it comes to politics, therefore, the US has plenty to worry about, as it did in the 1950s, when Mad coined its slogan to satirize the complacency of Dwight D. Eisenhower’s Cold War. It is just that the real worries were not about economics, but about geopolitical blunders and conflict with communist Russia. This seems to me another interesting analogy between the 1950s and the decade ahead.

Finally, what about the threat of 1970s-style stagflation? This is a definite possibility, although I have been arguing since last summer that economic theory and history both suggest that a period of Keynesian policy success more analogous to the 1950s and early 1960s is most likely. This is not the place to rehearse all these arguments, so let me just repeat two less speculative points that I made last month.

First, that labor markets will mainly determine whether the decade ahead is marked by stagflation, meaning much higher inflation and weaker growth than in the monetarist period since 1980, or by Keynesian success, meaning slightly higher inflation and significantly stronger growth. Second, that nobody will know the answer to this conundrum until the second half of his decade. Until then, investors will have to make guesses about the long[1]term future, and they will tend to do this on the basis of what happens in the present and the recent past.

Therefore, if inflation in the next six to 12 months proves to be somewhat tamer than expected while growth remains well above pre-Covid trends, the Keynesian success story will gain credibility and fears of stagflation will subside. This is the short-term outlook that seems most plausible in the US and almost certain in Europe and Japan, with Britain the only advanced economy facing a serious short-term danger of stagflation, for reasons Nick Andrews outlined last week. I therefore believe that the 1950s Keynesian scenario will gain favor in the markets. But what about the many economists and former policymakers who, like Mervyn King and Larry Summers, will keep warning about disastrously repeating 1970s-style stagflation? My reply, in the spirit of the 1950s, will be “What— me worry?”. And I suspect that the markets will agree.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.